In the realm of personal finance, few expenses are as universally borne yet as widely varied as car insurance. For millions of drivers, the quest to find “cheap car insurance” is an annual or even semi-annual pilgrimage, driven by the desire to protect their assets without breaking the bank. Yet, the answer to “who has cheap car insurance” isn’t a simple name or a single company. It’s a complex interplay of personal factors, market dynamics, and savvy shopping strategies that, when understood and applied, can lead to significant savings. This article delves deep into the financial considerations of car insurance, guiding you through the labyrinth of policies, premiums, and providers to help you identify the most cost-effective coverage for your unique situation. We’ll explore the financial levers you can pull, the pitfalls to avoid, and the strategic approaches that empower you to take control of your car insurance budget, transforming a seemingly unavoidable cost into a manageable and optimized financial commitment.

Understanding the Landscape of Car Insurance Costs

The notion of a single provider universally offering the cheapest car insurance is a pervasive myth. The reality is that insurance premiums are meticulously calculated based on a vast array of individualized factors, making the “cheapest” option a highly personal determination. Understanding these underlying financial mechanics is the first step toward securing more affordable coverage.

Key Factors Influencing Your Premium

Car insurance companies are sophisticated risk assessors. Every piece of information they gather about you, your vehicle, and your driving habits contributes to their calculation of how likely you are to file a claim, and how costly that claim might be. From a financial perspective, these factors directly translate into higher or lower premiums.

Firstly, your driving record is paramount. A history of accidents, traffic violations (especially DUIs or reckless driving), or even minor infractions signals a higher risk, leading to significantly inflated premiums. Conversely, a clean driving record, often for a period of three to five years, is a strong indicator of responsible behavior and can unlock substantial good driver discounts.

Secondly, your vehicle itself plays a crucial role. More expensive cars, sports cars, and those with high theft rates typically command higher premiums because the cost of repair or replacement is greater. Safety features, on the other hand, can sometimes lead to discounts, as they reduce the likelihood or severity of an accident. The age of your car also matters; older vehicles might have lower comprehensive and collision costs due to depreciation, but they might also lack modern safety features.

Thirdly, personal demographics and location are significant. Age is a major factor, with young, inexperienced drivers (especially those under 25) typically facing the highest rates due to statistical risk profiles. As drivers mature and gain experience, rates generally decrease, before potentially rising again in very old age. Your geographic location, down to your specific zip code, can impact rates based on local accident rates, theft statistics, and even weather patterns. Your credit score, in many states, is also a powerful predictor of financial responsibility, and a good score can lead to lower premiums, while a poor one can significantly increase them. This is a critical financial tool many drivers overlook.

Finally, the type and amount of coverage you choose directly affects your premium. Opting for state-mandated minimum liability coverage will always be cheaper upfront than comprehensive coverage with a low deductible, but it leaves you vulnerable to significant out-of-pocket expenses in the event of a major accident. Balancing adequate protection with affordability is a core financial decision.

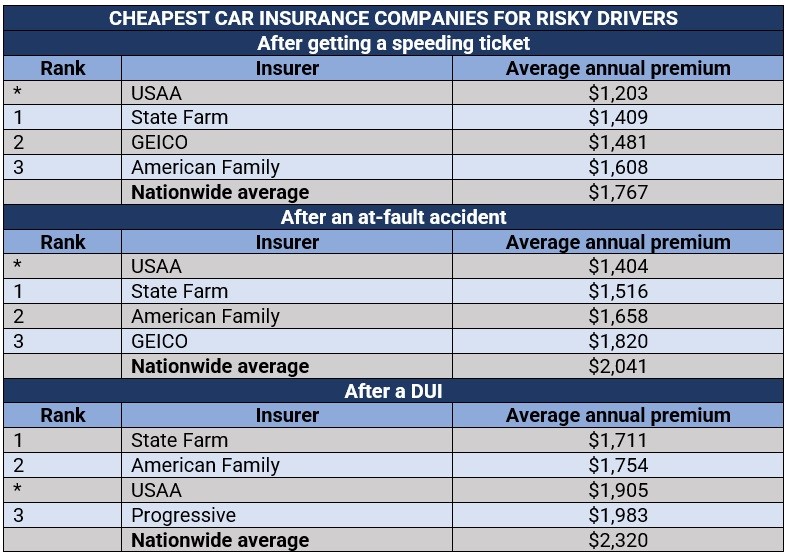

The Myth of a Single “Cheapest” Provider

No single insurance company consistently offers the lowest rates for everyone. Company A might be cheapest for a young driver with a new sports car in an urban area, while Company B might offer the best deal for a mature driver with a perfect record in a rural setting. This divergence stems from each insurer’s unique underwriting algorithms, target customer base, and risk appetite. Some companies specialize in high-risk drivers, others in bundling policies, and still others in specific demographics. Their pricing models are not monolithic; they are tailored to their specific financial goals and market positioning.

Why Your Profile Matters More Than the Company

Given the personalized nature of premium calculations, your individual driver profile is arguably more influential than the specific insurance company you choose. It’s not about finding the company with cheap car insurance, but rather finding the company that offers you the cheapest car insurance based on your specific circumstances. This means that a proactive, informed approach to managing your driver profile and actively seeking out quotes tailored to it is paramount. Thinking of car insurance as a financial product where your personal data points are inputs into a pricing engine helps reframe the search from a passive query to an active financial strategy.

Strategic Approaches to Finding Cheaper Car Insurance

The good news is that while many factors are beyond your immediate control (like your age or past accident history), there are numerous proactive financial strategies you can employ to significantly reduce your car insurance costs.

Leverage Comparison Websites and Independent Agents

The digital age has revolutionized the car insurance shopping experience. Online comparison websites allow you to input your details once and receive multiple quotes from various insurers simultaneously. This can be an invaluable time-saver and a powerful tool for identifying the most competitive rates available to your profile. However, it’s important to note that not all insurers participate in every comparison site, so supplementing this with direct quotes from major carriers is often wise.

Alternatively, an independent insurance agent can be a financial ally. Unlike captive agents who work for a single company, independent agents work with multiple insurers. They can shop around on your behalf, often having access to exclusive rates or companies not found on public comparison sites. Their expertise can be particularly beneficial if you have a complex driving history or unique insurance needs, as they can help navigate the nuances and find tailored financial solutions.

Bundling Policies for Significant Savings

One of the most effective ways to reduce your insurance costs is by bundling multiple policies with the same provider. Insurers often offer substantial multi-policy discounts when you combine car insurance with homeowner’s, renter’s, or umbrella policies. From a financial standpoint, this incentivizes customer loyalty and reduces administrative overhead for the insurer, benefits they often pass on to you in the form of lower premiums across all policies. The savings from bundling can sometimes outweigh minor differences in individual policy pricing, making it a critical strategy for comprehensive financial planning.

Maximizing Discounts: From Good Driver to Low Mileage

Insurance companies offer a plethora of discounts, many of which are often overlooked. Actively inquire about and qualify for every discount you are eligible for. Common discounts include:

- Good Driver Discount: For maintaining a clean driving record over a specified period.

- Multi-Car Discount: For insuring more than one vehicle with the same company.

- Good Student Discount: For young drivers who maintain a high GPA.

- Low Mileage Discount: If you drive fewer miles than the average person annually.

- Anti-Theft Device Discount: For vehicles equipped with approved security systems.

- Safety Feature Discount: For cars with features like airbags, anti-lock brakes, or adaptive cruise control.

- Affiliation Discounts: For members of certain professional organizations, alumni associations, or employers.

- Defensive Driving Course Discount: For completing an approved driver safety course.

Each discount, though seemingly small individually, can collectively shave a significant percentage off your premium, reflecting smart financial management.

The Impact of Your Deductible and Coverage Levels

Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in after a claim. From a financial perspective, choosing a higher deductible (e.g., $1,000 instead of $250 or $500) will almost always result in lower monthly or annual premiums. This is a direct trade-off: you save money upfront but assume greater financial risk in the event of a claim. Assess your emergency fund and financial comfort level to determine if you can realistically afford a higher deductible should an accident occur.

Similarly, your coverage levels directly influence your premium. While it’s tempting to opt for minimum state-mandated liability to save money, this can be a financially catastrophic decision in the event of a serious accident where damages exceed your coverage limits. The excess costs would come directly out of your pocket. Consider dropping comprehensive and collision coverage on older, lower-value vehicles where the annual premium for these coverages might approach or exceed the car’s actual cash value. This is a strategic financial decision to avoid over-insuring an depreciating asset.

Optimizing Your Driving Habits and Vehicle for Lower Rates

Beyond policy adjustments, your everyday choices related to driving and vehicle ownership have a profound financial impact on your insurance premiums. Cultivating good habits and making informed decisions can lead to sustained savings.

Maintaining a Clean Driving Record

This cannot be overstated. A clean driving record is the golden ticket to lower insurance premiums. Every ticket, every accident, and especially every serious violation, will likely trigger an increase in your rates, sometimes for several years. From a financial planning perspective, avoiding incidents is the single most impactful way to control your insurance costs long-term. Investing in defensive driving skills, obeying traffic laws, and avoiding distractions behind the wheel are not just about safety; they are about protecting your financial future from escalating insurance expenses.

Choosing the Right Vehicle: Insurability Matters

When purchasing a new or used vehicle, its “insurability” should be a key financial consideration alongside the sticker price and fuel economy. Certain vehicles are inherently more expensive to insure due to factors like their theft rates, repair costs, horsepower (indicating higher risk for speeding), or the cost of their parts. Before making a significant vehicle purchase, get insurance quotes for several models you’re considering. You might be surprised to find that a seemingly minor difference in model or trim level can lead to substantial annual savings or increased costs in your insurance premium. This is a long-term financial decision that extends beyond the initial purchase price.

Telematics Programs: Trading Data for Discounts

Many insurers now offer telematics programs, also known as usage-based insurance (UBI). These programs involve installing a device in your car or using a smartphone app to monitor your driving habits, such as mileage, speed, braking, acceleration, and time of day you drive. In exchange for sharing this data, safe drivers can earn significant discounts on their premiums. While some may have privacy concerns, for those confident in their responsible driving habits, telematics programs represent a direct financial pathway to lower rates by proving you are a lower risk. This is an innovative financial tool leveraging technology to personalize insurance pricing.

Financial Management and Review for Sustained Savings

Finding cheap car insurance isn’t a one-time event; it’s an ongoing process of financial vigilance and periodic review. Market rates change, your personal circumstances evolve, and new opportunities for savings emerge.

Regular Policy Reviews and Re-shopping

It’s prudent financial practice to review your car insurance policy at least once a year, or whenever major life events occur (e.g., getting married, moving, buying a new car, or adding a new driver). Don’t assume your current insurer still offers you the best rate. Insurers often reserve their best rates for new customers, a phenomenon known as “loyalty penalty.” Re-shopping your policy by getting quotes from multiple providers regularly can ensure you’re always getting the most competitive premium for your current profile. This proactive approach ensures your insurance budget remains optimized.

Improving Your Credit Score (Where Applicable)

In many states, your credit-based insurance score (which is related to, but distinct from, your traditional credit score) is a significant factor in determining your premium. Insurers use these scores as a predictor of how likely you are to file a claim. Statistically, individuals with higher credit scores tend to file fewer claims. Therefore, improving your financial health by maintaining a good credit score—paying bills on time, managing debt responsibly, and avoiding excessive credit inquiries—can indirectly lead to lower car insurance rates. This reinforces the interconnectedness of various aspects of personal finance.

Understanding Payment Plans and Fees

How you pay for your insurance can also impact your overall cost. Many insurers offer a discount for paying your premium in full upfront, rather than in monthly installments. While this requires a larger initial outlay, it can save you money by avoiding installment fees or finance charges. If paying annually isn’t feasible, consider setting up automatic payments, as some companies offer a small discount for auto-pay. Be mindful of any processing fees associated with specific payment methods and factor them into your total cost calculation.

Navigating Special Circumstances and Future Trends

The insurance landscape is dynamic, with specific challenges for certain demographics and evolving trends that will shape future affordability.

Young Drivers and High-Risk Policies

Young drivers, particularly teenagers and those under 25, face disproportionately high insurance rates due to their lack of experience and statistically higher accident rates. Financially, this can be a significant burden. Strategies for young drivers include: remaining on a parent’s policy, taking defensive driving courses, utilizing good student discounts, choosing a modest, safety-rated vehicle, and carefully considering higher deductibles. For drivers classified as “high-risk” due to multiple accidents or serious violations, finding affordable insurance can be even more challenging, often requiring specialized insurers or state-mandated residual market plans, which tend to be more expensive but necessary for legal driving.

The Rise of Usage-Based Insurance

As telematics technology becomes more sophisticated and widely adopted, usage-based insurance (UBI) is set to become an even more prominent feature of the car insurance market. This trend promises a more personalized and potentially fairer pricing model, where premiums are directly tied to actual driving behavior rather than broad demographic assumptions. For careful drivers, UBI offers a continuous opportunity for savings, transforming insurance from a fixed annual cost into a flexible expense influenced by daily habits. This represents a significant shift in how personal finance intersects with insurance.

Looking Ahead: Autonomous Vehicles and Insurance

The advent of autonomous vehicles is poised to fundamentally disrupt the car insurance industry. As cars become self-driving, the liability for accidents could shift from the driver to the vehicle manufacturer or software provider. This seismic change could lead to a dramatic reduction in human-error related accidents, potentially lowering insurance costs across the board. However, it will also introduce new complexities, such as cybersecurity risks and software malfunction liabilities, which will need to be factored into future insurance models. While still some years away, financial planners should monitor these developments as they will profoundly impact transportation costs.

In conclusion, the question “who has cheap car insurance?” doesn’t have a universal answer. It’s a call to action for every driver to become a proactive financial manager of their car insurance expenses. By understanding the factors influencing premiums, strategically shopping for policies, optimizing driving habits, and regularly reviewing coverage, you can demystify the process and unlock substantial savings, ensuring your protection doesn’t come at an exorbitant price.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.