In the intricate world of finance, where transactions range from simple cash exchanges to multi-million dollar corporate mergers, understanding the underlying instruments that facilitate these dealings is paramount. Among these crucial instruments is the promissory note—a seemingly straightforward document that underpins a vast array of financial obligations, both personal and commercial. Often misunderstood or overlooked in its fundamental importance, the promissory note serves as a legally binding testament to a debt, outlining the terms of repayment and safeguarding the interests of both borrower and lender.

At its core, a promissory note is more than just an “IOU”; it’s a formal, written promise by one party (the maker or borrower) to pay a definite sum of money to another party (the payee or lender) at a specified future date or on demand. This document formalizes a loan agreement, making it a critical component of personal finance, business transactions, and even investment strategies. Delving into its structure, types, legal implications, and practical applications reveals its indispensable role in maintaining financial order and certainty.

The Fundamentals of a Promissory Note

To truly grasp the significance of a promissory note, one must first understand its foundational principles and the essential elements that define its legality and utility. It’s a document born of trust but solidified by legal enforceability, designed to provide clarity and security in financial arrangements.

Defining the Core Concept

A promissory note is essentially a written contract that details the terms of a loan between two parties. Unlike a verbal agreement, which can be prone to misinterpretation or forgetfulness, a promissory note provides a clear, undeniable record of the borrower’s promise to repay. It quantifies the debt, specifies the interest (if any), and sets a timeline for repayment, thereby removing ambiguity and establishing a transparent framework for the financial relationship. This clarity is vital, as it offers both parties a reference point and a legal basis for action should disputes arise.

The concept itself dates back centuries, evolving from simple handwritten promises to sophisticated financial instruments recognized by modern legal systems worldwide. Its enduring presence in finance speaks to its effectiveness as a reliable mechanism for managing debt and credit.

Key Elements of a Valid Promissory Note

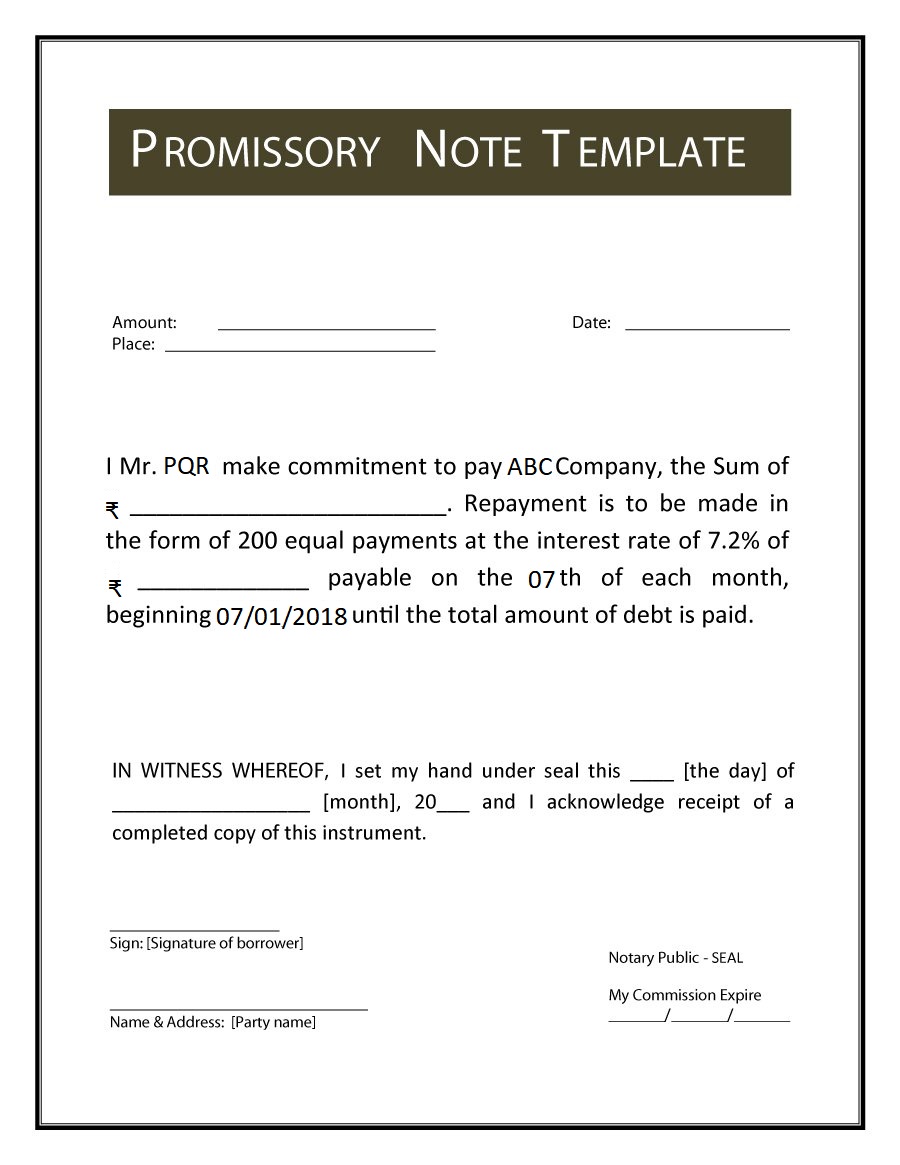

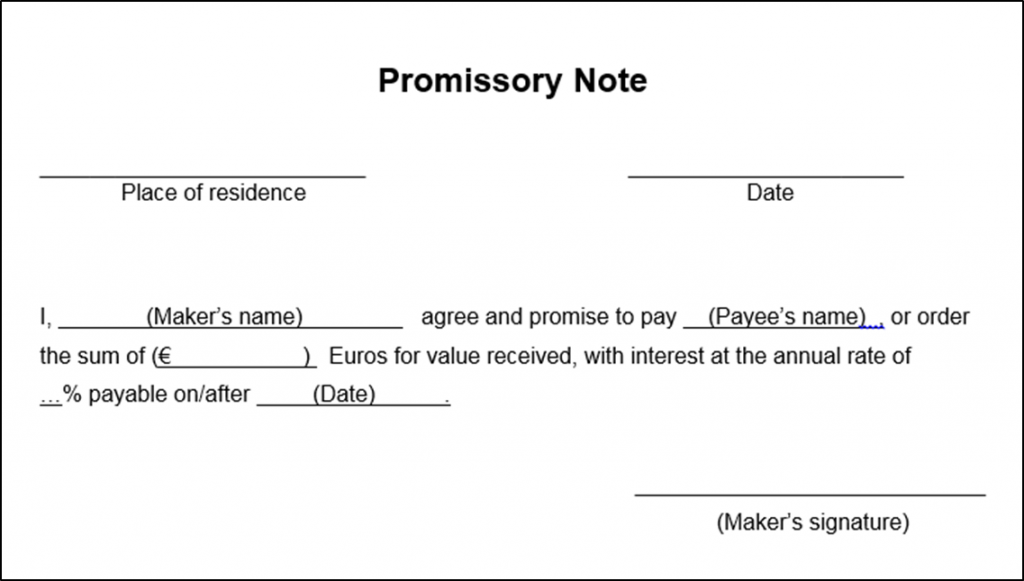

For a promissory note to be legally enforceable and serve its intended purpose, it must contain several critical components. Omitting any of these can render the note invalid or complicate its enforcement.

- Principal Amount: The exact sum of money borrowed and promised to be repaid. This must be a specific, fixed amount.

- Parties Involved: Clearly identified names and addresses of both the borrower (maker) and the lender (payee).

- Terms of Repayment: This includes the repayment schedule (e.g., lump sum, installments), due dates, and any grace periods.

- Interest Rate: If applicable, the annual percentage rate (APR) charged on the principal, and how interest is calculated (e.g., simple, compound).

- Date of Issuance: The date the note was created and signed.

- Signatures: The legally binding signatures of all borrowers. Often, the lender’s signature is not required for the note to be valid, but some forms may include it for acknowledgement.

- Maturity Date: The date by which the entire loan, including interest, must be repaid. For demand notes, this might be “on demand.”

- Collateral (if any): Details of any assets pledged by the borrower to secure the loan.

- Default Clause: Specifies what constitutes a default and the actions the lender can take in such an event (e.g., accelerating repayment, seizing collateral).

- Governing Law: The state or jurisdiction whose laws will govern the note.

Parties Involved

Typically, there are two primary parties to a promissory note:

- The Maker (Borrower): The individual or entity who promises to pay the specified sum of money. They are creating the debt and are legally obligated to fulfill the terms of the note.

- The Payee (Lender): The individual or entity to whom the money is owed. They are the recipient of the payments and hold the right to enforce the terms of the note.

In some cases, especially in more complex financial arrangements, a guarantor might also be involved. A guarantor is a third party who agrees to take on the borrower’s debt obligation if the borrower defaults. This adds an extra layer of security for the lender.

Types and Applications of Promissory Notes

The versatility of promissory notes allows them to be adapted for a wide range of financial scenarios, from informal family loans to sophisticated business financing. Understanding the different types and their applications is crucial for leveraging them effectively within the “Money” domain.

Secured vs. Unsecured Notes

One of the most significant distinctions in promissory notes lies in whether they are secured or unsecured:

- Secured Promissory Notes: These notes are backed by collateral, meaning the borrower pledges specific assets (like real estate, vehicles, or equipment) that the lender can seize and sell if the borrower defaults. The presence of collateral significantly reduces the risk for the lender, often leading to more favorable interest rates for the borrower. Mortgages are a prime example, where the property itself serves as collateral.

- Unsecured Promissory Notes: These notes are not backed by any specific collateral. The lender’s only recourse in case of default is the borrower’s general creditworthiness and legal action. Due to the higher risk for the lender, unsecured notes often carry higher interest rates or are only offered to borrowers with excellent credit histories. Personal loans, credit card debt, and some student loans typically fall into this category.

Demand vs. Term Notes

The repayment schedule also categorizes promissory notes:

- Demand Promissory Notes: With a demand note, the lender can “demand” repayment of the entire principal and any accrued interest at any time, usually with a specified notice period. There is no fixed maturity date. These are less common for large, long-term loans but can be useful for flexible arrangements.

- Term Promissory Notes: These notes specify a fixed repayment schedule, including installment amounts and a definitive maturity date by which the entire loan must be repaid. Most traditional loans (car loans, mortgages, business loans) are term notes, offering predictability for both parties.

Promissory Notes in Personal Finance

In personal finance, promissory notes often formalize loans between individuals, such as family members or friends. While informal, these loans can benefit greatly from a promissory note to prevent misunderstandings and preserve relationships. They are also used in more formal settings, like student loans from private lenders or specific personal installment loans. They provide a clear framework for repaying a loan for a down payment on a house, medical expenses, or an educational pursuit, ensuring that expectations are clearly set and legally binding.

Promissory Notes in Business Finance

For businesses, promissory notes are a flexible tool for various financing needs. Small businesses might use them for short-term working capital, borrowing from an investor or another business. They can facilitate vendor financing, where a supplier provides goods on credit and accepts a promissory note for payment. In larger contexts, they might be part of more complex financial instruments or used in the sale of a business, where the buyer issues a note to the seller for a portion of the purchase price. They are particularly useful for private loans to a company, where traditional bank financing might be unavailable or undesirable.

Promissory Notes in Real Estate

Real estate transactions frequently employ promissory notes. The most common example is a mortgage, which consists of two primary documents: a promissory note (the promise to repay the loan) and a mortgage or deed of trust (the legal instrument that pledges the property as collateral). Promissory notes are also used in seller financing (or owner financing), where the seller of a property acts as the lender, accepting a promissory note from the buyer for a portion of the purchase price, often with the property as collateral. This can make property ownership accessible when traditional bank loans are not an option.

Legal Implications and Enforceability

The legal backbone of a promissory note is what gives it its power and reliability as a financial instrument. Understanding this legal framework is essential for both lenders looking to protect their assets and borrowers seeking to understand their obligations.

The Legal Framework

In the United States, promissory notes are governed primarily by state contract law and Article 3 of the Uniform Commercial Code (UCC), which deals with negotiable instruments. The UCC provides a standardized set of laws that govern commercial transactions, ensuring consistency across states regarding the creation, transfer, and enforcement of promissory notes. This framework dictates what makes a note valid, how it can be transferred, and the rights and responsibilities of each party.

What Makes a Note Legally Binding?

Beyond including the key elements mentioned earlier, a promissory note becomes legally binding when it is properly executed, meaning all parties (at least the maker) have signed it with the intent to be bound by its terms. For a promissory note to be enforceable, there must typically be:

- Offer and Acceptance: The lender offers the loan, and the borrower accepts the terms.

- Consideration: Something of value exchanged between the parties (e.g., the money loaned by the lender, the promise to repay by the borrower).

- Legal Capacity: Both parties must be of legal age and sound mind to enter into a contract.

- Lawful Purpose: The loan must be for a legal activity; a note for an illegal gambling debt, for instance, would be unenforceable.

While notarization is not strictly required for a promissory note to be legally valid, it can add an extra layer of authenticity and make it harder for a borrower to later claim their signature was forged.

Consequences of Default

Defaulting on a promissory note means failing to adhere to its terms, most commonly by missing payments. The consequences of default can be severe and vary based on whether the note is secured or unsecured, and what the default clause specifies:

- Secured Notes: The lender can initiate foreclosure proceedings or repossess the collateral (e.g., a home, car, or business equipment) to recover their losses.

- Unsecured Notes: The lender’s options are more limited. They may sue the borrower in court to obtain a judgment for the outstanding debt. If successful, they can then pursue wage garnishment, bank account levies, or place liens on other assets the borrower owns.

- Credit Impact: Defaulting will severely damage the borrower’s credit score, making it difficult to obtain future loans or credit.

- Accelerated Payment: Many notes include an acceleration clause, allowing the lender to demand the entire outstanding balance immediately upon default, rather than waiting for scheduled payments.

Assignment and Transferability

One significant feature of promissory notes is their transferability. A lender (payee) can often sell or “assign” the note to a third party. This means the new party becomes the legal owner of the debt and has the right to collect payments from the borrower. This is common in financial markets; for example, original mortgage lenders often sell their loans to other financial institutions. The borrower’s obligations generally remain the same, but they will now be making payments to a different entity. This negotiability is a key aspect that allows promissory notes to function within the broader financial system as assets that can be bought and sold.

Advantages and Disadvantages

Like any financial instrument, promissory notes present both opportunities and risks for the parties involved. A balanced perspective is crucial before entering into such an agreement.

Benefits for the Lender

- Legal Protection: Provides a legally enforceable document for debt recovery.

- Clear Terms: Eliminates ambiguity regarding repayment, interest, and deadlines.

- Flexibility: Can be customized to suit specific loan situations, including interest rates and repayment schedules.

- Collateral Option: For secured notes, it offers an asset to seize in case of default, reducing risk.

- Transferability: The note can be sold or assigned, providing liquidity if the lender needs cash before the loan matures.

Benefits for the Borrower

- Access to Capital: Can provide financing when traditional bank loans are unavailable or impractical (e.g., private loans, family loans, seller financing).

- Potentially Better Terms: In private arrangements, interest rates or repayment terms might be more flexible or favorable than institutional lenders.

- Formalizes Informal Loans: Helps maintain good relationships by professionalizing loans between friends or family.

- Clear Understanding of Obligation: Provides a transparent record of what is owed and when, aiding in financial planning.

Risks and Drawbacks for Both Parties

- For the Lender:

- Default Risk: The primary risk is that the borrower may not repay the loan, especially with unsecured notes.

- Enforcement Costs: Pursuing legal action to collect on a defaulted note can be time-consuming and expensive.

- Interest Rate Risk: If interest rates rise after the note is issued, the lender might be locked into a lower return.

- For the Borrower:

- Legal Obligation: Once signed, it’s a binding contract. Failure to repay has significant legal and financial consequences.

- Impact on Credit: Defaulting on a formal promissory note can severely damage credit.

- Lack of Flexibility: While customizable, the terms are fixed once agreed upon, making changes difficult without lender consent.

- Complexity: Can be complex to draft correctly, especially for those without legal expertise, leading to potential loopholes.

Creating and Managing a Promissory Note

The process of creating and managing a promissory note demands attention to detail and, often, professional guidance to ensure its efficacy and legal soundness.

Essential Clauses to Include

Beyond the core elements, several clauses are critical for a robust promissory note:

- Late Payment Penalties: Fees or increased interest rates for missed or late payments.

- Prepayment Penalty/Option: Whether the borrower can repay the loan early without penalty, or if a penalty applies.

- Waiver of Presentment: A clause where the borrower waives their right to demand presentation of the note for payment.

- Attorney’s Fees Clause: States that the defaulting party will be responsible for the other party’s legal fees if a lawsuit is initiated.

- Severability Clause: If one part of the note is found to be unenforceable, the rest of the note remains valid.

- Amendment Clause: Outlines the process for making changes to the note in the future.

The Importance of Professional Guidance

While templates for promissory notes are readily available online, relying solely on them without legal review can be risky. Engaging an attorney ensures that the note is:

- Legally Sound: Compliant with state and federal laws, including usury laws (which cap interest rates).

- Customized: Tailored to the specific circumstances of the loan, addressing unique risks and needs.

- Enforceable: Contains all necessary clauses to protect the parties involved and stands up in court if necessary.

For significant sums or complex arrangements, legal advice is an investment that can prevent costly disputes down the line.

Record Keeping and Due Diligence

Both lenders and borrowers must practice meticulous record-keeping. Lenders should maintain a copy of the original signed note, all payment records, and any correspondence related to the loan. Borrowers should keep copies of the note, receipts for all payments made, and any amendments. This due diligence ensures that both parties have a clear trail of the transaction, which is invaluable in resolving discrepancies or proving compliance/non-compliance.

Conclusion

The promissory note, far from being a mere piece of paper, is a cornerstone of modern financial transactions. It is a testament to the power of a written promise, formalized by law, to facilitate the flow of capital and manage debt obligations across personal, business, and real estate sectors. Its ability to provide clarity, legal enforceability, and a structured framework for repayment makes it an indispensable tool for anyone involved in lending or borrowing money.

Whether you are lending money to a family member, financing a business venture, or securing a mortgage, understanding the intricacies of a promissory note is not just about legal compliance; it’s about safeguarding financial interests, fostering trust, and ensuring that financial promises are honored. By recognizing its fundamental components, diverse applications, and legal weight, individuals and businesses can navigate the complexities of financial agreements with confidence and foresight, ensuring stability and predictability in their monetary dealings.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.