In an era dominated by instantaneous digital transfers, peer-to-peer payment apps, and biometric security, the humble paper check remains a surprisingly resilient fixture of the global financial system. Whether you are setting up direct deposit for a new job, paying a contractor, or authorizing a large-scale business transaction, you will inevitably be asked for your routing number.

To the untrained eye, the string of numbers at the bottom of a check can look like a cryptic code. However, understanding exactly which number is the routing number is not just a matter of convenience—it is a foundational aspect of personal finance and financial literacy. This guide will help you identify your routing number, understand its critical role in the banking infrastructure, and ensure you are using it securely in your financial life.

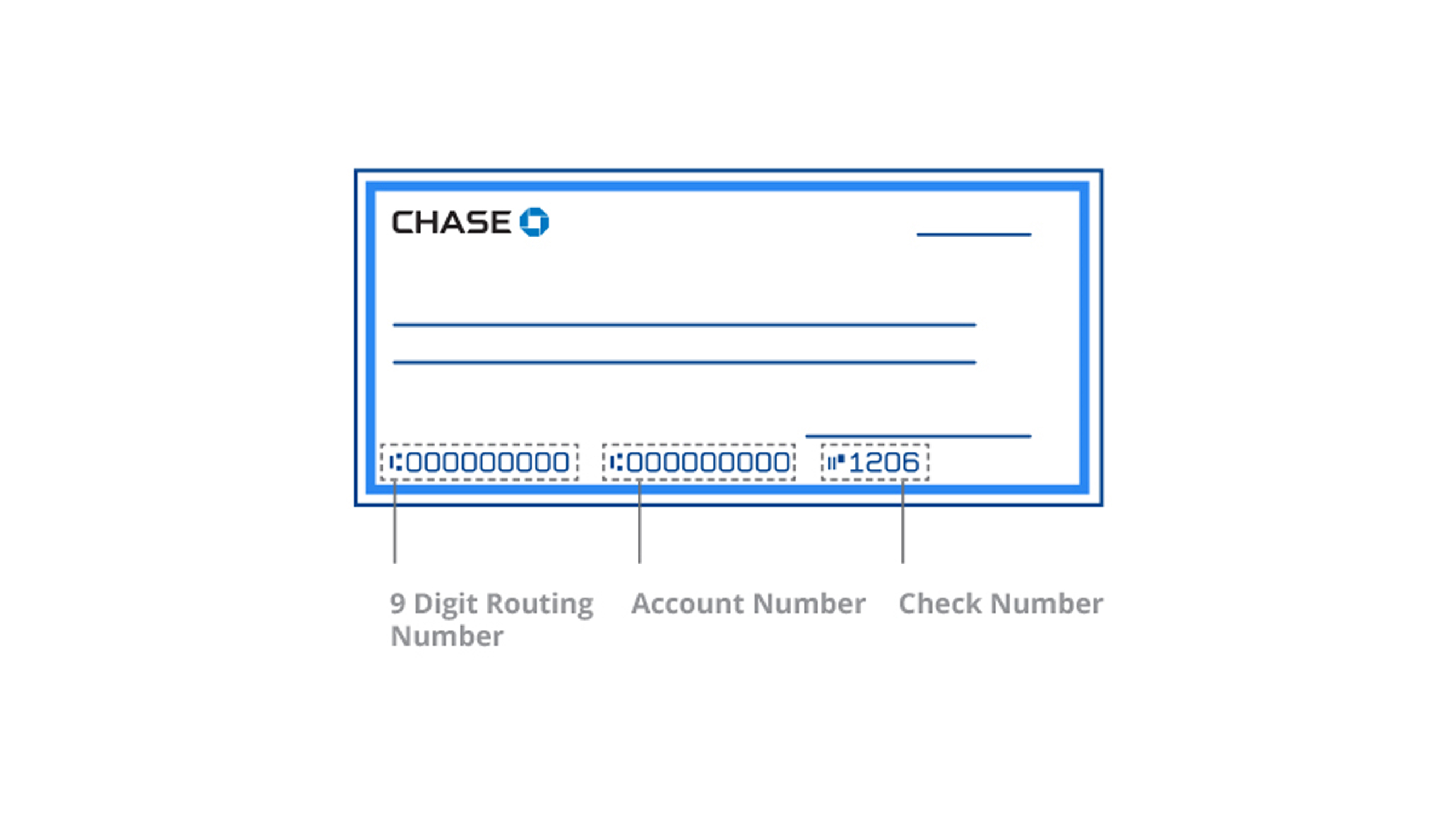

Anatomy of a Check: Identifying the Routing Number

When you look at a standard personal or business check, the most important information is printed along the bottom edge. This area is known as the MICR (Magnetic Ink Character Recognition) line. Banks use specialized machines to read this line to process checks quickly and accurately.

The Bottom Row Mechanics

The MICR line typically consists of three distinct sets of numbers. If you are looking at a check, the numbers are usually arranged from left to right. In almost all standard US banking formats, the routing number is the first set of numbers on the far left. It is framed by a specific symbol that looks like a vertical line with a colon (⑆).

The Nine-Digit Rule

One of the easiest ways to verify you have found the correct number is to count the digits. In the United States, a routing number—also known as an ABA (American Bankers Association) routing transit number (RTN)—is always exactly nine digits long. If the number you are looking at has eight or ten digits, you are likely looking at the account number or the check number instead.

Routing vs. Account Numbers

The middle set of numbers on the MICR line is your unique account number. While the routing number identifies the financial institution, the account number identifies your specific piece of that institution. To the right of the account number, you will find the check number, which usually matches the number printed in the top right corner of the check. Distinguishing between these three is vital; providing an account number when a routing number is requested will result in a failed transaction and potential “insufficient funds” or “incorrect data” fees.

Why Routing Numbers Matter in Modern Finance

While you might only look for a routing number when you have a physical check in hand, this nine-digit code is the backbone of the electronic banking system. It serves as a digital address that tells the financial network exactly where money needs to go.

ACH Transfers and Direct Deposits

Most modern “Money” management involves Automated Clearing House (ACH) transfers. When your employer sends your paycheck via direct deposit, or when you set up an automatic payment for a utility bill, the ACH network uses your routing number to find your bank and your account number to find your specific funds. Without a valid routing number, the electronic handshake between two different banks cannot occur.

Wire Transfers vs. Routing Numbers

It is a common misconception in personal finance that the routing number on your check is used for all types of transfers. In reality, some banks use a different routing number for domestic wire transfers than they do for ACH transfers or paper checks. Wire transfers are handled through the Fedwire system, and using the “check” routing number for a wire transfer can lead to significant delays or the funds being returned to the sender. Always verify with your bank’s website if they have a specific “Wire Routing Number.”

Business Finance and Vendor Payments

For entrepreneurs and small business owners, the routing number is an essential tool for cash flow management. When paying vendors through a business portal, you must provide accurate routing data to avoid late fees. Furthermore, understanding the routing system allows business owners to reconcile their books more effectively, as they can track exactly which institution processed a specific payment.

ABA vs. ACH: Understanding the Variations

The world of financial tools can be confusing because terms are often used interchangeably. However, in the context of routing numbers, there is a historical and functional distinction that every savvy investor and account holder should understand.

The American Bankers Association (ABA) History

The routing number system was created by the American Bankers Association in 1910. Its original purpose was to simplify the sorting and shipping of physical paper checks. Each number in the nine-digit sequence has a meaning: the first two digits indicate the Federal Reserve district, the third indicates the specific processing center, and the remaining digits identify the specific bank.

Different Routing Numbers for Different Transactions

As banking evolved from physical to digital, the way these numbers are used changed. Today, large national banks (like Chase, Bank of America, or Wells Fargo) may have dozens of different routing numbers. A customer in California will have a different routing number than a customer in New York, even if they use the same bank. Furthermore, some institutions have a specific routing number dedicated solely to electronic (ACH) transactions and another for physical checks. Before setting up a significant financial link, such as an investment account or a high-yield savings account transfer, always check your bank’s “Routing Number” page to ensure you are using the correct one for that specific transaction type.

Locating Your Routing Number Without a Physical Check

We are rapidly moving toward a “checkless” society. Many modern “neobanks” and online-only financial institutions do not even issue physical checkbooks unless specifically requested. If you don’t have a check in front of you, there are several reliable ways to find your routing number.

Online Banking Dashboards

The most efficient way to find your routing number is through your bank’s secure online portal. Once you log in, navigate to “Account Details” or “Account Summary.” Most banks will list the routing number right next to your account number. This is often the most accurate source because it will specify if the number is for ACH, Wire, or Direct Deposit.

Mobile Apps and E-Statements

If you are on the go, your bank’s mobile app is a powerful financial tool. Most apps have a “Direct Deposit” or “Account Info” section that provides a digital image of a “voided check,” clearly labeling the routing and account numbers. Additionally, if you download a PDF of your monthly bank statement, the routing number is frequently printed at the top or bottom of the first page.

Contacting Your Financial Institution

If you are ever in doubt—especially for large transactions like a down payment on a home or a major investment—call your bank’s customer service or visit a local branch. Providing the wrong routing number can lead to “funds in limbo,” which can take days or weeks to recover. A quick confirmation with a bank representative can provide peace of mind in your financial dealings.

Protecting Your Financial Information

While the routing number itself is public information (anyone can look up the routing number for a specific bank online), the combination of your routing number and your account number is the “key” to your financial castle. Protecting this information is a cornerstone of digital security and personal finance.

The Risks of Sharing Routing and Account Numbers

If a malicious actor gains access to both your routing and account numbers, they can potentially initiate unauthorized ACH withdrawals from your account. This is why you should never send a photo of a check or your banking details over unencrypted email or SMS. Financial institutions use secure portals for a reason; always use those channels when providing sensitive data.

Best Practices for Check Security

If you still use physical checks, treat them with the same care you would treat cash. Store your checkbook in a locked drawer, and when you need to provide a “voided check” for a payroll department, ensure you write “VOID” in large letters across the center so it cannot be used as a negotiable instrument. Furthermore, regularly monitor your bank statements for any unauthorized ACH transactions. Most banks have a limited window (often 60 days) for you to dispute an unauthorized electronic transfer.

Conclusion: The Foundation of Financial Literacy

Identifying the routing number on a check is a simple task that carries significant weight in the world of personal and business finance. It is the bridge between your physical assets and the digital economy. By understanding that the routing number is the nine-digit code on the bottom left of your check, and by recognizing its role in ACH and wire transfers, you empower yourself to manage your money with greater precision and security.

In the complex landscape of modern financial tools, the details matter. Whether you are automating your savings, launching a side hustle, or simply paying your monthly rent, being confident in your banking data is the first step toward long-term financial health and security. Always double-check the digits, verify the transaction type, and keep your account information guarded. Knowledge is the best asset in any financial portfolio.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.