Managing a business’s financial obligations requires a meticulous eye for detail, particularly when it comes to payroll tax reporting. Form 941, the Employer’s Quarterly Federal Tax Return, is a cornerstone of federal tax compliance for any entity with employees. While many modern businesses have transitioned to electronic filing, a significant number of organizations still prefer or require the submission of paper forms.

Knowing exactly where to mail Form 941—especially when you are filing without a payment—is critical. Sending your documentation to the wrong IRS processing center can result in processing delays, unnecessary correspondence, or even erroneous late-filing penalties. This guide provides a comprehensive breakdown of mailing locations and explores the financial strategies underlying payroll tax management.

The Geography of Payroll Tax Compliance: Mailing Addresses

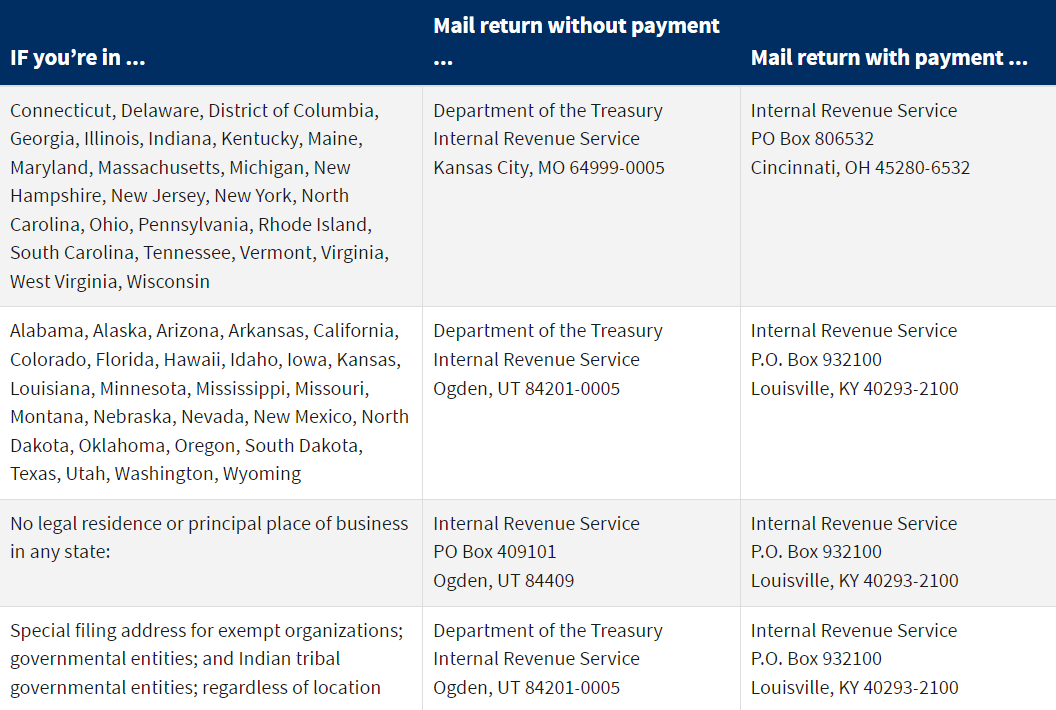

The Internal Revenue Service (IRS) utilizes different processing centers based on the geographic location of your business and whether or not you are enclosing a payment. For businesses that have already made their tax deposits via the Electronic Federal Tax Payment System (EFTPS) or those that have no tax liability for the quarter, the mailing address is distinct from those who are sending a physical check.

IRS Processing Centers for Filing Without Payment

If your business is located in the following states, and you are not including a payment, your filing destination is generally the Internal Revenue Service center in Ogden, UT:

- Alabama, Alaska, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming.

Mailing Address:

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0005

Conversely, if your business is headquartered in the following states and you are filing without a payment, you must mail your return to the Kansas City, MO facility:

- Connecticut, Delaware, District of Columbia, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin.

Mailing Address:

Department of the Treasury

Internal Revenue Service

Kansas City, MO 64999-0005

Special Considerations for Exempt Organizations and International Filers

If you are filing for an exempt organization or if your business location is not within the 50 states (such as Puerto Rico, the Virgin Islands, or a foreign country), the IRS typically directs these filings to the Ogden, Utah facility. Always ensure the “no payment” status is clear; if a payment is accidentally included in a “no payment” envelope, it may delay the processing of the check, potentially leading to interest charges if the payment is deemed late.

Strategic Financial Management: Why Filing Without Payment Occurs

In the realm of business finance, filing a Form 941 without an attached payment is not an indication of tax avoidance; rather, it is often a sign of sophisticated cash flow management and compliance with federal deposit schedules.

The Role of the Electronic Federal Tax Payment System (EFTPS)

Most businesses are required by law to deposit their payroll taxes (federal income tax withheld plus the employer and employee shares of Social Security and Medicare taxes) via EFTPS. For monthly or semi-weekly depositors, the money has already left the business bank account long before the quarterly return is due.

In this scenario, Form 941 serves as a reconciliation statement. It informs the IRS of the total liability for the quarter, which the IRS then matches against the deposits already received. Filing without payment is the standard procedure for any business that is fully “paid up” through electronic transfers. From a financial management perspective, using EFTPS is superior to mailing checks as it provides an immediate digital audit trail and reduces the risk of mail fraud or loss.

Managing Quarters with Zero Liability

There are instances where a business may remain active but have no employees or paid wages during a specific quarter. This is common in seasonal industries or during periods of corporate restructuring. Even if the liability is zero, the IRS generally expects a return if the business is still registered as an active employer. Filing a “Zero Return” is a vital defensive financial move. It prevents the IRS from generating an estimated tax assessment—an automated process where the government assumes you owe money based on previous quarters and begins a collection sequence that can freeze business assets.

Correcting Overpayments through Form 941

Financial officers often encounter situations where a business overpaid its taxes in a previous period. When filing the current Form 941, a business may apply that overpayment (credit) to the current quarter. If the credit covers the entire balance, the return is mailed without a new payment. Strategically, this keeps capital within the business rather than waiting for a refund check, which can take months to process.

The Financial Implications of Filing Accuracy and Deadlines

The quarterly deadlines for Form 941 are non-negotiable: April 30, July 31, October 31, and January 31. Understanding the financial weight of these deadlines is essential for maintaining a healthy balance sheet.

The True Cost of Late Filing

The IRS imposes a “failure-to-file” penalty of 5% of the unpaid tax for each month or part of a month that a return is late, up to a maximum of 25%. Even if you have paid all your taxes via EFTPS but fail to mail the Form 941, you are still technically out of compliance. While the penalty is calculated based on “unpaid” tax, the administrative burden of resolving a missing return notice can cost a business hundreds of dollars in professional accounting fees and lost productivity.

The Trust Fund Recovery Penalty (TFRP)

In the world of business finance, payroll taxes are considered “trust fund taxes” because the employer holds the employees’ money in trust until it is remitted to the government. The IRS is notoriously aggressive in collecting these. If a business fails to file and pay, the IRS can move beyond the corporate entity and hold “responsible persons” (owners, officers, or even key employees) personally liable for the unpaid taxes. This is one of the few instances where the “corporate veil” is easily pierced, making the timely mailing of Form 941 a matter of personal financial security for business leaders.

Utilizing Certified Mail as a Financial Safeguard

When mailing a return without payment, the business loses the “proof” that a cashed check provides. Therefore, from a risk management standpoint, it is imperative to use USPS Certified Mail with a Return Receipt Requested. This $10–$15 investment serves as legal proof of filing. In the event of an IRS audit or a “Notice of Unfiled Return,” having a stamped certified mail receipt can save a business thousands of dollars in erroneously assessed penalties and interest.

Optimizing the Payroll Cycle for Better Cash Flow

Beyond the mechanics of mailing forms, high-performing businesses use the Form 941 process as a quarterly financial checkup.

Quarterly Reconciliation Processes

Before the 941 is mailed, the financial department should reconcile the payroll journal, the general ledger, and the EFTPS deposit records. This “three-way match” ensures that the business is not over-reporting liability (which wastes cash) or under-reporting liability (which invites penalties).

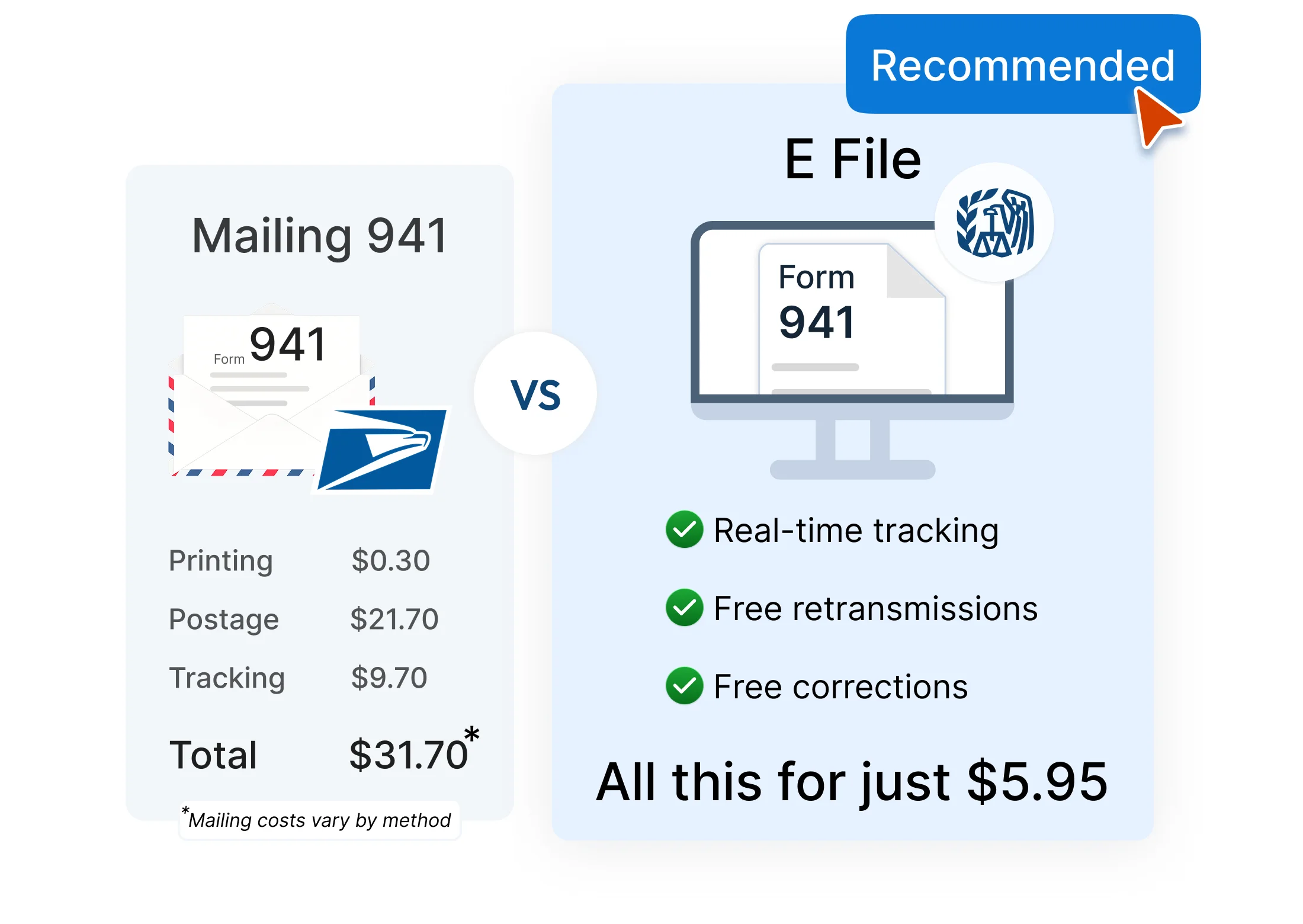

Transitioning to E-Filing for Enhanced Security

While this guide details where to mail paper forms, a sound financial strategy often involves moving toward e-filing. Electronic filing provides an immediate receipt from the IRS, confirming that the return has been accepted. For a business looking to lean out its administrative processes, e-filing eliminates the variables of the postal service and ensures that the financial data reaches the IRS Treasury systems with 100% accuracy.

Preparing for Year-End Reporting

The four quarterly 941 filings must perfectly align with the annual Form 940 (FUTA) and the W-2/W-3 forms sent to the Social Security Administration. Discrepancies between the quarterly “no payment” filings and the year-end totals are a major red flag for tax authorities. By ensuring the 941 is mailed to the correct address and contains verified data, a business sets the stage for a seamless year-end financial close.

Conclusion

Determining where to mail Form 941 without payment is more than just a logistical task; it is a vital component of a business’s broader financial health and regulatory compliance. Whether you are mailing your return to Ogden or Kansas City, the act represents the final step in a quarterly cycle of responsible stewardship of employee funds.

By adhering to the correct mailing protocols, leveraging EFTPS for digital payments, and maintaining rigorous documentation through certified mail, business owners can protect their organizations from unnecessary penalties. In the complex landscape of business finance, precision in the small details—like a mailing address—is what separates a vulnerable enterprise from one that is built on a foundation of stability and trust.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.