For the past few years, the housing market has felt like a high-stakes waiting game. Prospective homebuyers, current homeowners looking to upsell, and real estate investors have all been fixated on one metric: the mortgage interest rate. After a period of historic lows during the early 2020s, the sudden and aggressive climb of rates has left many wondering when the pendulum will swing back.

Understanding when home interest rates will go down requires a deep dive into the machinery of the global economy, the mandates of the Federal Reserve, and the shifting landscape of inflation. This article explores the factors currently holding rates steady, the indicators that will signal a decline, and the financial strategies you should employ while waiting for a more favorable borrowing environment.

Understanding the Mechanics of Mortgage Rates

To predict when rates will fall, we must first understand why they are currently high. Mortgage rates do not exist in a vacuum; they are the result of a complex interplay between government policy and market sentiment.

The Federal Reserve’s Role and the Federal Funds Rate

While the Federal Reserve does not directly set mortgage rates, its influence is paramount. The Fed sets the “Federal Funds Rate,” which is the interest rate at which banks lend to each other overnight. When the Fed raises this rate to combat inflation, the cost of borrowing increases across the board—from credit cards to business loans and, eventually, mortgages.

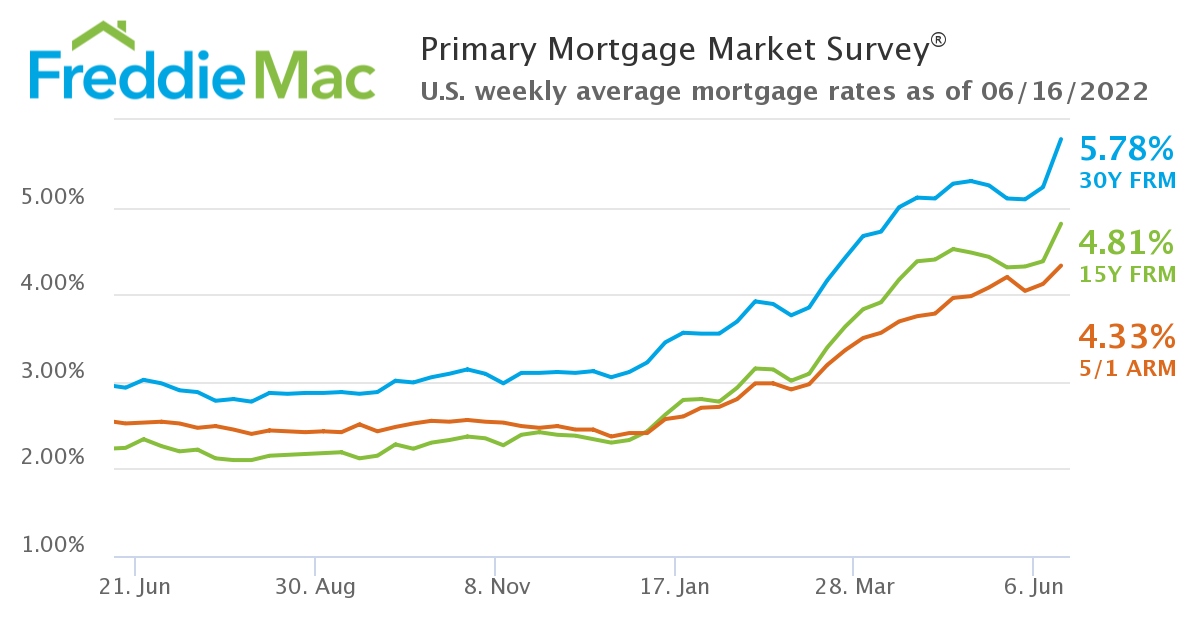

Between 2022 and 2024, the Fed engaged in one of the most aggressive rate-hiking cycles in history to cool down an overheating economy. Until the Federal Reserve sees definitive proof that inflation is permanently under control, they are unlikely to pivot toward significant rate cuts.

The 10-Year Treasury Yield and the “Spread”

Most fixed-rate mortgages are closely tied to the performance of the 10-year U.S. Treasury yield. Investors view Treasuries as “risk-free” assets. When investors demand higher yields on government bonds due to inflation concerns or economic uncertainty, mortgage lenders must raise their rates to remain competitive and cover their own risks.

Historically, there is a “spread” or a gap of about 1.5% to 2% between the 10-year Treasury yield and the average 30-year fixed mortgage rate. In recent times, this spread has widened due to market volatility. For home interest rates to drop significantly, we need to see both a decline in Treasury yields and a narrowing of this spread as the market stabilizes.

Economic Indicators That Trigger a Rate Decrease

Economists look for specific “green lights” before forecasting a downward trend in interest rates. If you are tracking the market, these are the data points that matter most.

The “2% Inflation Target” Milestone

The Federal Reserve has a dual mandate: maximum employment and price stability. “Price stability” has been mathematically defined as an annual inflation rate of 2%. As measured by the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index, inflation skyrocketed well above 8% in 2022.

While inflation has cooled significantly since then, the “last mile” of reaching that 2% goal has proven difficult. Rates will likely stay “higher for longer” until the Fed is confident that inflation is not just falling, but staying down. Any month where CPI data comes in lower than expected usually results in a temporary dip in mortgage rates as the market anticipates a future Fed cut.

Labor Market Cooling and Economic Growth

Paradoxically, “bad” news for the economy is often “good” news for interest rates. A robust labor market with high wage growth is generally inflationary. When everyone has a job and wages are rising, spending remains high, which keeps prices elevated.

If the labor market begins to show signs of softening—such as an increase in the unemployment rate or a decrease in monthly job additions—the Fed may feel pressured to lower interest rates to prevent a recession. A slowing GDP (Gross Domestic Product) is another indicator that the economy has cooled enough to justify lower borrowing costs.

Expert Projections and the 2024–2025 Outlook

Predicting the exact month rates will drop is impossible, but we can look at the consensus among major financial institutions like Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR).

Short-Term vs. Long-Term Expectations

In the short term (the next 3 to 6 months), the consensus suggests a “plateau.” Most experts believe that the peak of the rate cycle has passed, but they do not expect a rapid descent. Instead, we are likely to see incremental decreases of 0.1% to 0.25% at a time.

Looking toward late 2024 and into 2025, many forecasts suggest that the 30-year fixed rate could settle into the high 5% or low 6% range. While this is significantly higher than the 3% rates seen in 2021, it is much closer to the long-term historical average of 7% to 8% seen over the last 50 years.

Why We Might Not See “COVID-Era” Rates Again

It is vital for personal financial planning to manage expectations regarding how low rates will actually go. The 2% and 3% mortgage rates of the pandemic era were an anomaly caused by an unprecedented global emergency and massive government intervention.

In a “normal” healthy economy, those rates are generally unsustainable. Most economists agree that we are entering a “new normal” where a 5.5% mortgage is considered a great deal. Waiting for rates to return to 3% might result in years of missed equity growth as home prices continue to rise due to limited inventory.

Strategic Financial Planning in a High-Rate Environment

If you are looking to buy a home or refinance, you cannot control the Federal Reserve, but you can control your financial response to the current environment.

To Wait or Not to Wait? The Cost of Waiting

One of the biggest dilemmas in personal finance today is whether to buy now at a high rate or wait for rates to fall. The “Cost of Waiting” analysis suggests that if you wait for rates to drop by 1%, but home prices rise by 5% in that same period, you may actually end up with a higher monthly payment and less equity than if you had bought earlier.

Furthermore, when rates eventually do drop significantly, a flood of sidelined buyers will likely enter the market. This increased demand often leads to bidding wars, driving home prices up and negating the savings from the lower interest rate.

Mortgage Refinancing and Creative Financing Options

For those who choose to buy now, the prevailing mantra in the industry is “Marry the house, date the rate.” This implies buying the property you want now and planning to refinance the mortgage once rates inevitably decline in the future.

Additionally, buyers are exploring creative tools to mitigate high rates:

- Adjustable-Rate Mortgages (ARMs): These often offer a lower initial rate for the first 5, 7, or 10 years.

- Rate Buydowns: Buyers (or sellers, as a concession) can pay upfront “points” to the lender to permanently or temporarily lower the interest rate.

- Assumable Mortgages: Some government-backed loans (like FHA or VA loans) allow a buyer to “assume” the seller’s existing low-interest rate, though this requires a specific set of circumstances.

Conclusion: Navigating the Uncertainty

When will home interest rates go down? The most likely scenario is a gradual easing beginning in late 2024 and continuing through 2025, provided that inflation continues its slow descent toward the 2% target. However, the days of near-zero interest rates are likely behind us for the foreseeable future.

From a money management perspective, the best strategy is to focus on your personal “readiness” rather than trying to time a volatile market perfectly. Strengthening your credit score, increasing your down payment, and reducing your debt-to-income ratio will have a more significant impact on the rate you are offered than the fluctuations of the daily news cycle. By staying informed on economic indicators like CPI and Treasury yields, you can position yourself to act quickly when the market finally shifts in favor of the borrower.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.