In the rapidly evolving landscape of personal finance, few tools have achieved the level of cultural and functional ubiquity as Venmo. Originally launched in 2009 and later acquired by PayPal, Venmo has transitioned from a simple mobile payment experiment into a cornerstone of the modern financial ecosystem. At its core, Venmo is a peer-to-peer (P2P) payment service that allows users to transfer funds via a mobile phone app. However, its implications for personal budgeting, business transactions, and the broader concept of “social finance” are profound.

Understanding Venmo requires looking beyond its interface to see how it functions as a financial intermediary. For millions of users, it has replaced the physical wallet, the checkbook, and even the ATM. This article explores Venmo through the lens of finance, examining its mechanics, its utility in personal and business management, and the cost structures that define its operations.

The Mechanics of Digital Payments: How Venmo Works

Venmo operates as a “digital wallet,” a middle layer between your traditional bank account and the people or businesses you interact with. Unlike a direct bank wire, which can be cumbersome and time-consuming, Venmo facilitates near-instantaneous ledger changes within its own ecosystem. To understand Venmo from a financial perspective, one must understand the flow of capital through its platform.

Linking Your Financial Foundation

The utility of Venmo begins with the integration of existing financial assets. Users link their debit cards, credit cards, or direct bank accounts to the app. From a financial strategy standpoint, the choice of link is significant. Linking a bank account or a debit card typically allows for fee-free transactions when sending money to individuals. In contrast, using a credit card incurs a standard 3% transaction fee, reflecting the processing costs imposed by credit providers. This distinction is crucial for users who leverage Venmo for high-frequency transactions, as these fees can quietly erode one’s monthly budget.

The Venmo Balance vs. Bank Transfers

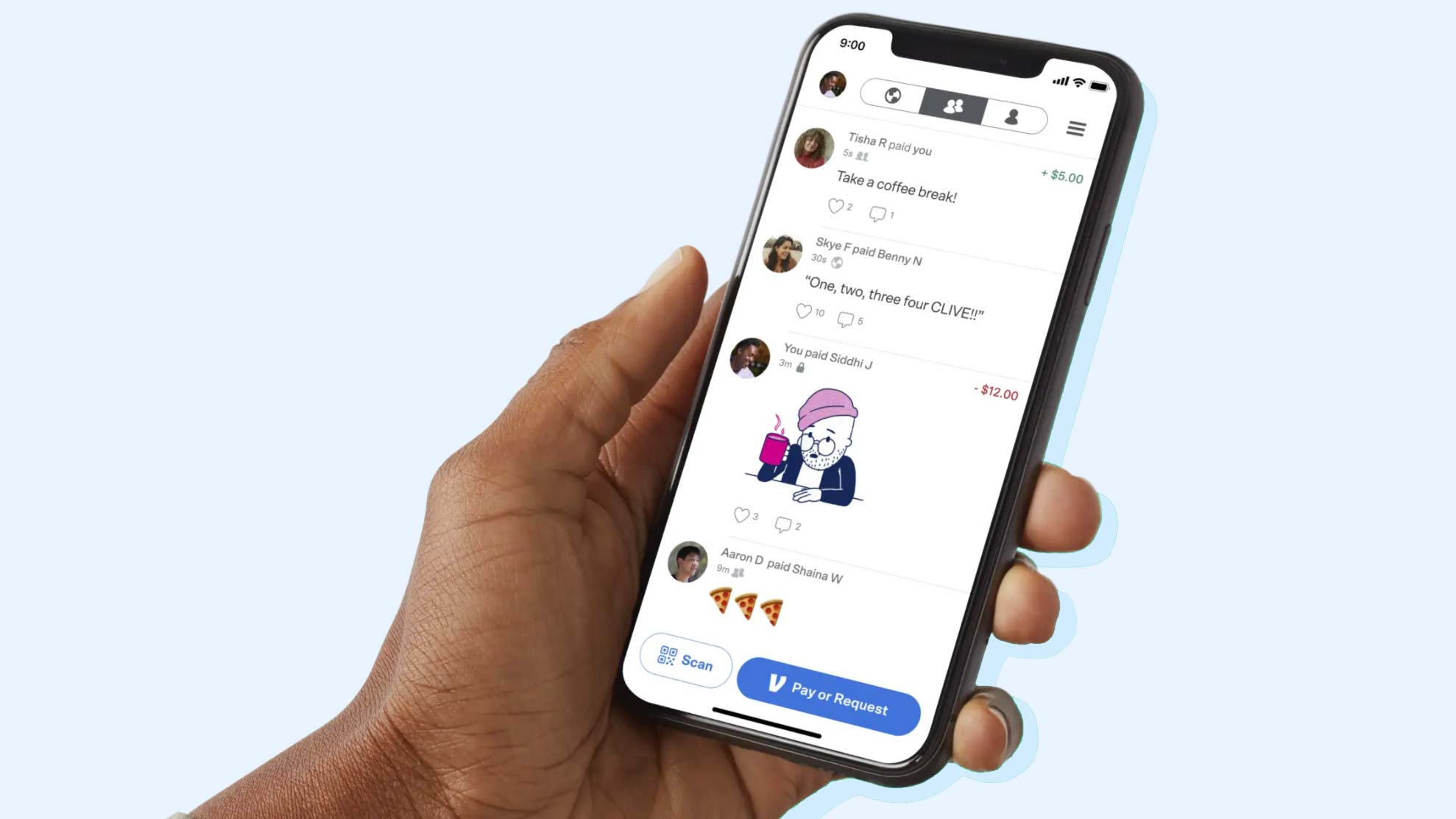

When you receive money on Venmo, the funds do not automatically move to your bank account. Instead, they sit in your “Venmo Balance.” This is a crucial distinction in digital finance. This balance acts as a liquid asset within the Venmo ecosystem; you can use it to pay others or make purchases at participating merchants without ever touching your primary bank account.

However, moving that money out of the Venmo ecosystem requires a “transfer.” Venmo offers two primary paths:

- Standard Transfer: This is free and typically takes 1 to 3 business days via the Automated Clearing House (ACH) network.

- Instant Transfer: For users needing immediate liquidity, Venmo offers a transfer to a debit card or bank account within minutes for a small percentage-based fee. From a financial planning perspective, relying on instant transfers is a cost that should be budgeted for, particularly for those using Venmo as a primary source of income.

Venmo for Personal Finance Management

Venmo’s greatest impact has been on the micro-level of personal finance: the daily exchange of small sums. By removing the friction of cash and the awkwardness of debt collection among friends, it has fundamentally changed how we manage shared expenses.

Splitting Expenses and Group Budgeting

One of the most effective uses of Venmo is its ability to facilitate “split-bill” scenarios. Whether it is rent, utilities, or a dinner check, the app allows for precise financial distribution. For individuals who are meticulous about budgeting, Venmo provides a digital paper trail. Each transaction can be categorized or searched, making it easier to track “social spending”—a category that often goes unmonitored in traditional banking statements. By using the “Request” feature, users can ensure they are reimbursed promptly, maintaining the health of their personal cash flow.

Avoiding Common Financial Pitfalls and Scams

As a financial tool, Venmo requires a level of fiscal responsibility regarding security. Because Venmo was designed for “friends and family,” it lacks the robust buyer protection programs found in traditional credit cards or even its parent company, PayPal, for personal transactions.

From a financial safety perspective, users must treat Venmo like cash. Once a payment is sent, it is notoriously difficult to reverse. Financial experts advise only sending money to known entities. Furthermore, the “social feed” feature—where transactions can be made public—presents a unique privacy concern. While it adds a layer of social engagement, savvy financial users often set their transactions to “Private” to ensure their spending habits and recipient lists remain confidential, protecting themselves from social engineering or targeted financial scams.

Expanding the Ecosystem: Venmo for Business and Commerce

While it started as a tool for friends, Venmo has aggressively expanded into the realm of business finance. This shift has provided small business owners, freelancers, and side-hustlers with a low-barrier-to-entry method for accepting digital payments.

The Rise of Venmo Business Profiles

For the modern entrepreneur, a Venmo Business Profile offers a professional way to accept payments without the need for a complex Point of Sale (POS) system. From a business finance perspective, this is a game-changer for micro-businesses like local artisans or freelance consultants.

However, using Venmo for business introduces a different set of financial rules. Unlike personal transfers, business transactions are subject to a seller fee (typically a small percentage plus a fixed cent amount). This fee covers the cost of transaction processing and provides the seller with a level of protection. Furthermore, payments received through a business profile are considered taxable income. Venmo is required to report these earnings to the IRS via Form 1099-K if they exceed certain thresholds, making it imperative for business owners to maintain accurate records for tax season.

Integrating Venmo into Merchant Checkouts

Beyond small-scale sellers, Venmo has integrated with major retailers and online platforms. Many e-commerce sites now offer “Pay with Venmo” at checkout. This integration allows users to leverage their Venmo balance for retail therapy, effectively treating the app as a secondary checking account. For the consumer, this offers convenience; for the merchant, it offers access to a younger, tech-savvy demographic that may prefer the mobile-first experience of Venmo over entering credit card details.

Fees, Limits, and the Cost of Convenience

No financial tool is truly free, and Venmo’s revenue model is built on specific service fees and interest. To use Venmo effectively as a financial instrument, one must be aware of the “cost of doing business” within the app.

Understanding Transaction and Withdrawal Fees

As previously mentioned, Venmo is largely free for the average user, provided they link a bank account and are patient with transfers. However, the costs scale with urgency and credit usage:

- Credit Card Fee: 3% for sending money.

- Instant Transfer Fee: Currently 1.75% (with a minimum and maximum cap).

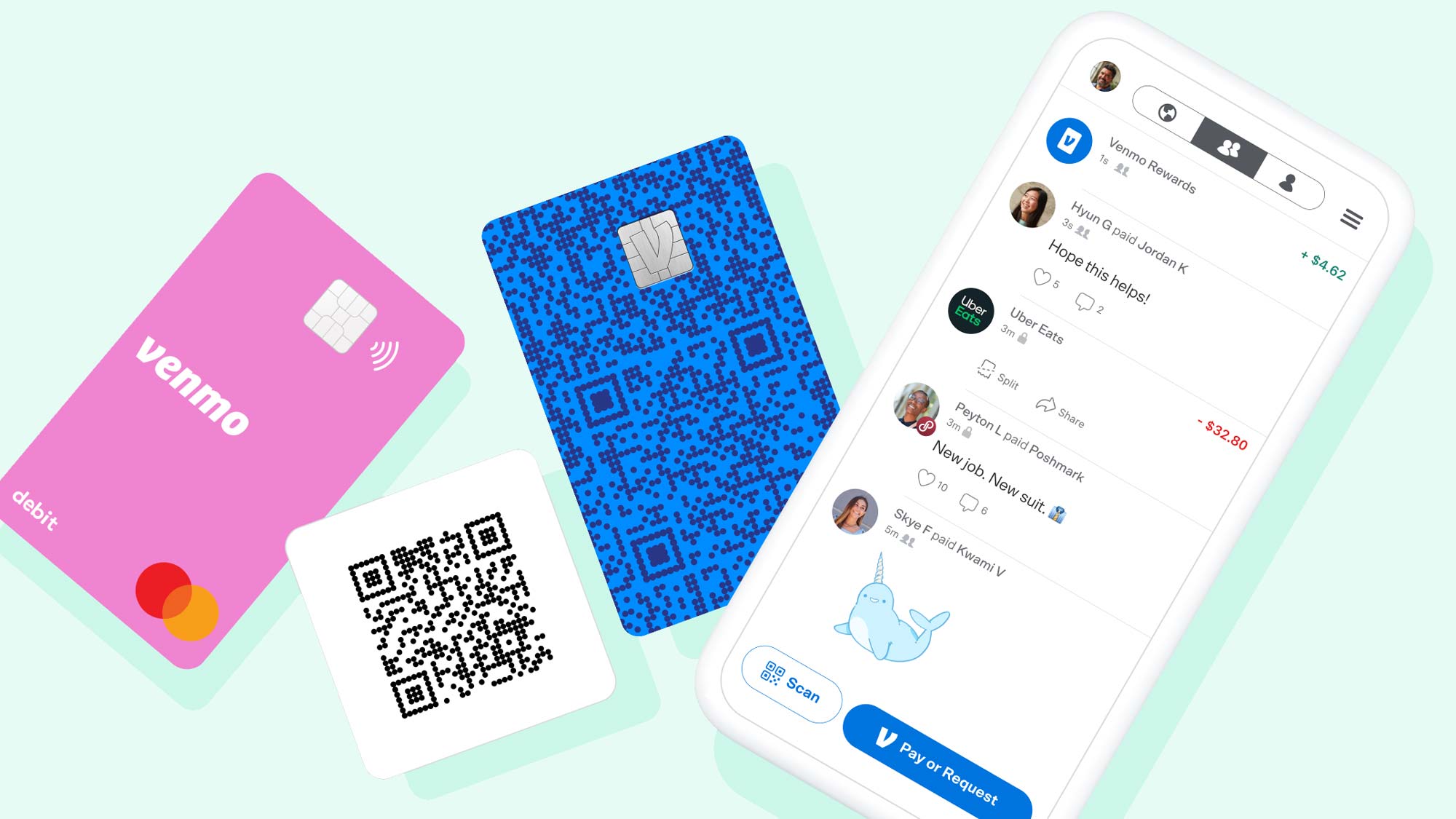

- Venmo Debit/Credit Card: Venmo offers its own physical cards. While these cards offer cashback rewards (a positive for personal finance), they also carry the standard risks of overspending and potential interest rates if the credit version is used.

Limits on Transfers and Spending

Venmo is not an infinite pool of capital. To comply with federal regulations and mitigate fraud risk, Venmo imposes “spending limits.” New users often have lower limits, which increase once their identity is verified. These limits apply to the amount you can send per week, the amount you can transfer to your bank, and the amount you can spend on the Venmo Debit Card. For those moving larger sums of money—perhaps for a down payment or a high-end purchase—Venmo may not be the appropriate tool, and traditional wire transfers remain the gold standard for high-value financial security.

The Future of Money: Cryptocurrency and Social Finance

Venmo continues to push the boundaries of what a P2P app can do, recently entering the world of alternative assets. This move positions Venmo not just as a payment app, but as a holistic financial platform.

Cryptocurrency as a Financial Asset

Venmo now allows users to buy, hold, and sell cryptocurrencies like Bitcoin and Ethereum directly within the app for as little as $1. From a personal finance perspective, this democratizes access to a volatile asset class. Users can use their Venmo balance to experiment with investing. However, the app charges a spread and a transaction fee for these trades, which can be higher than dedicated investment exchanges. It serves as an introductory “on-ramp” for the financially curious, though serious investors might find the lack of “private keys” or transferability to external wallets limiting.

The Evolution of the Financial Social Network

The “social” aspect of Venmo—adding emojis and notes to payments—serves a hidden financial purpose: it builds trust and verification. In the broader context of finance, Venmo is pioneering a world where money is not a static number in a ledger but a fluid part of social interaction. As Venmo integrates more deeply with payroll systems and investment tools, the line between a “social media app” and a “bank” continues to blur.

In conclusion, Venmo is far more than a tool for “paying someone back for pizza.” It is a sophisticated financial ecosystem that facilitates liquidity, enables small-scale entrepreneurship, and introduces users to new asset classes. By understanding the fees, the transfer mechanics, and the business implications, users can leverage Venmo as a powerful ally in their personal and professional financial journey. As with any financial tool, the key to success lies in transparency, security, and a clear understanding of the costs associated with the convenience it provides.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.