Navigating the financial landscape of electric vehicle (EV) ownership involves more than just calculating the initial purchase price or the savings at the charging station. For prospective and current Tesla owners, one of the most significant recurring line items in their budget is insurance. Tesla Insurance, the company’s in-house provider, has disrupted the traditional insurance market by leveraging real-time data to determine premiums. However, the question of “how much” remains complex, dictated by a convergence of personal finance variables, regional market shifts, and the unique risk profile of high-performance software-on-wheels.

Understanding the Economics of Tesla Insurance

To understand the cost of insuring a Tesla, one must first recognize that the company is not merely an automaker but a financial services entity. By offering its own insurance product, Tesla aims to solve a specific market inefficiency: traditional insurers often charge exorbitant premiums for EVs because they lack historical data or fear the high cost of proprietary repairs.

How Tesla Disrupts Traditional Insurance Math

Traditional insurance companies rely on actuarial tables—historical data based on age, gender, credit score, and general accident trends. Tesla, conversely, utilizes a “Real-Time Driving Behavior” model. From a personal finance perspective, this shifts the power dynamic from the insurer to the driver. Instead of being penalized for being in a high-risk demographic (such as being a young male driver), the premium is dictated by how the individual actually operates the vehicle.

This disruption means that the “cost” of Tesla insurance is a moving target. For a disciplined driver, the financial advantage can be substantial, often undercutting traditional providers by 20% to 30%. However, for those who frequently engage in aggressive braking or late-night driving, the financial burden may exceed that of a standard policy from Geico or Progressive.

The Average Monthly Premium: What the Data Says

While individual quotes vary wildly, market data suggests that the average cost for Tesla Insurance typically ranges between $150 and $350 per month. For a high-end Model S Plaid or Model X, premiums can easily climb toward $450 or more, reflecting the higher replacement value and repair complexity of these flagship vehicles.

In the broader context of personal finance, these figures represent a significant portion of the total cost of ownership (TCO). When budgeting for a Tesla, financial advisors suggest allocating approximately 1.5% to 2.5% of the car’s value annually for insurance. For a $50,000 Model 3, this equates to roughly $1,250 a year on the low end, though real-world rates in high-traffic urban areas often push this higher.

Factors Influencing Your Tesla Insurance Premiums

The price of a policy is rarely static. Several financial levers determine whether your monthly bill is a manageable expense or a significant financial drain.

The Impact of Location and Regional Markets

Insurance is heavily regulated at the state level, which creates massive discrepancies in cost. Currently, Tesla Insurance is available in a growing list of states, including Texas, California, Illinois, and Florida. In California, state laws prevent Tesla from using real-time driving data to set prices, meaning premiums there are more stable but often higher for safe drivers. In contrast, a driver in Texas can see their monthly premium fluctuate based on their “Safety Score,” creating a dynamic monthly expense that requires careful cash-flow management.

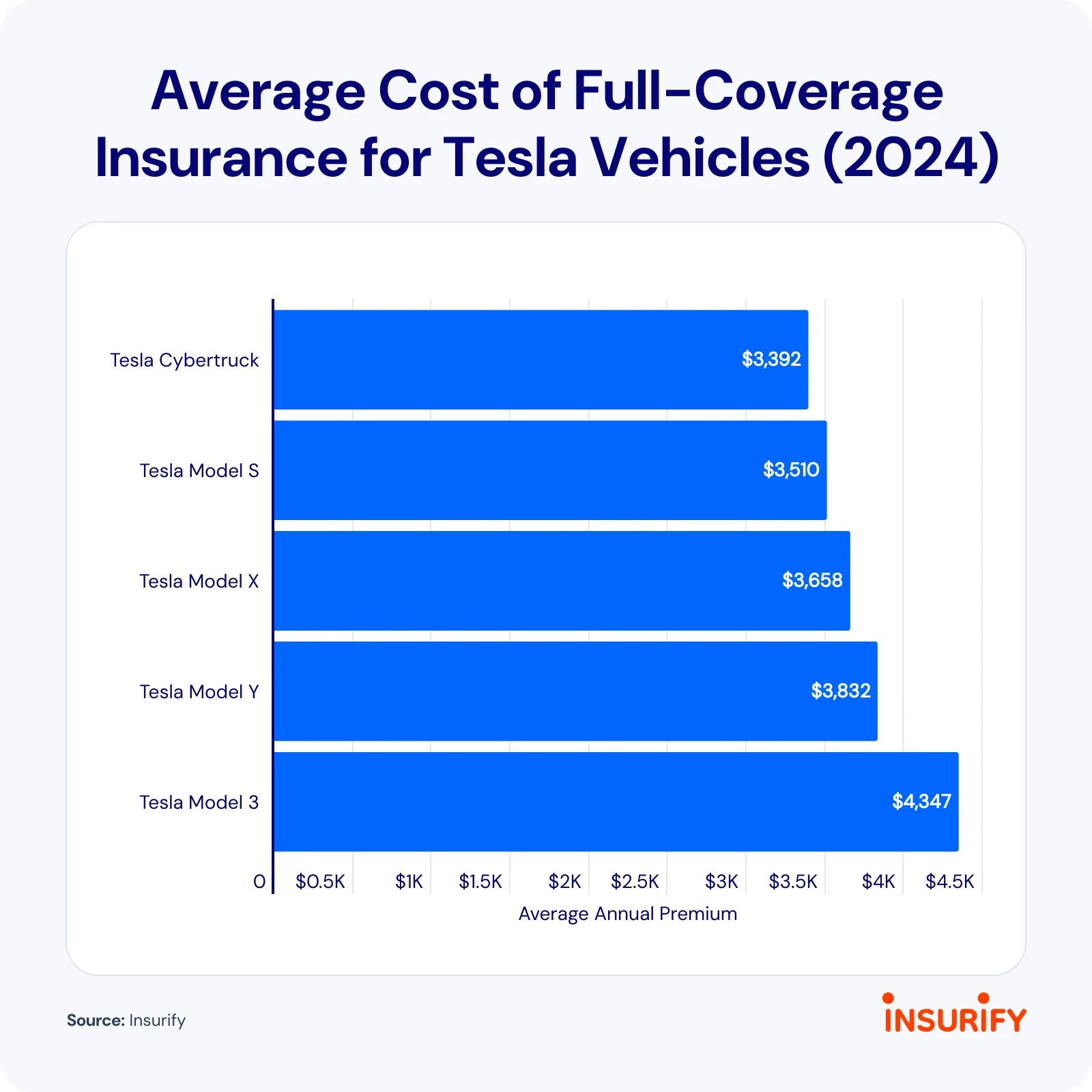

Vehicle Model Variations and Their Financial Weight

The specific model you choose is perhaps the largest fixed variable in the insurance equation.

- Model 3 and Model Y: These are the most “affordable” to insure. Because they are produced in high volumes, parts are more readily available, and the replacement cost is lower.

- Model S and Model X: These are luxury assets. Their aluminum intensive frames, complex falcon-wing doors (in the case of the Model X), and high-performance motors make them expensive to repair. Financially, the insurance for these models reflects the “luxury tax” inherent in high-value asset protection.

Driver Profile and Coverage Limits

Even with Tesla’s tech-forward approach, traditional financial variables still apply. Your choice of deductible is a primary factor. A $500 deductible will result in higher monthly premiums but lower out-of-pocket costs during an accident. Conversely, a $2,000 deductible lowers the monthly bill, shifting the financial risk back to the owner. For those using the Tesla as a business asset or a primary commuter vehicle, high liability limits (e.g., 100/300/100) are recommended to protect personal net worth, though this adds a premium to the base cost.

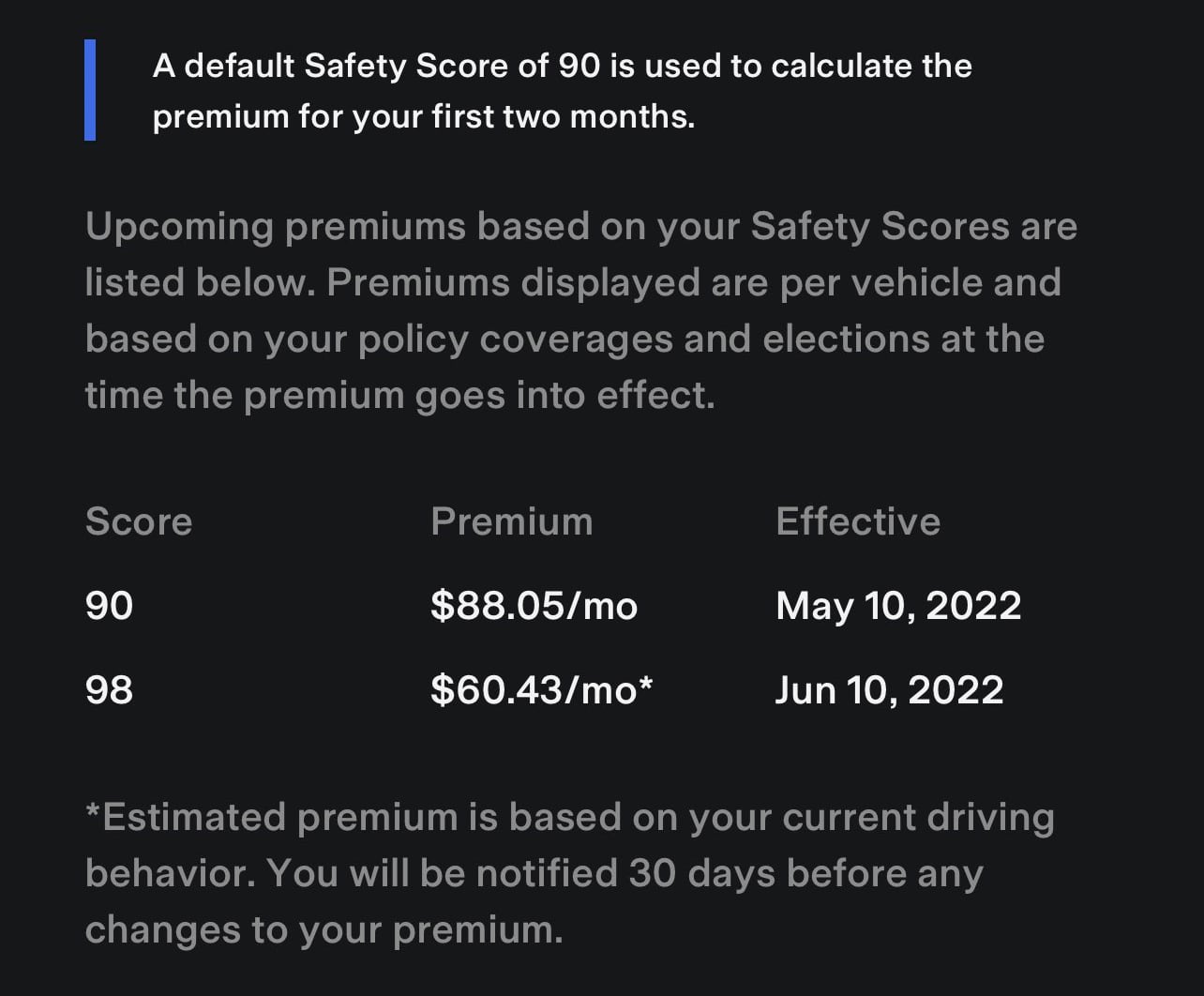

The Financial Impact of the “Safety Score” Model

The hallmark of Tesla’s insurance product is the Safety Score. This is a pedagogical tool for your wallet—it essentially gamifies personal finance by rewarding safe driving with lower bills.

Real-Time Telematics vs. Traditional Actuarial Tables

The Safety Score 2.0 (and its iterations) tracks specific metrics: Forward Collision Warnings per 1,000 miles, Hard Braking, Aggressive Turning, Unsafe Following, and Forced Autopilot Disengagements. From a budgetary standpoint, this creates a variable expense. A driver with a score of 98 might pay $120 a month, while that same driver, if their score drops to 85 due to aggressive driving, might see that bill spike to $190 the following month. This volatility requires a different approach to monthly budgeting than the “set it and forget it” nature of traditional insurance.

The Potential Savings for Defensive Drivers

For the financially savvy owner, the Safety Score represents an opportunity for “income optimization” by reducing expenses. By adhering to the metrics Tesla’s sensors track, a driver can effectively “earn” a discount every month. This makes Tesla Insurance particularly attractive to retirees or low-mileage drivers who tend to exhibit less risky behavior. Over a five-year ownership period, the delta between a high-score premium and a low-score premium can amount to several thousand dollars in saved capital.

Comparing Tesla Insurance to Traditional Providers

Before committing to Tesla’s in-house offering, a thorough cost-benefit analysis against legacy providers is essential.

Cost-Benefit Analysis: Tesla vs. Legacy Insurers

Many owners find that while Tesla offers the lowest initial quote, legacy insurers like State Farm or Amica might offer “bundle discounts” if the owner also carries homeowners or life insurance with them. When analyzing the money trail, one must look at the total household insurance spend. If switching your auto insurance to Tesla saves you $400 a year but causes you to lose a $500 multi-policy discount on your home insurance, the move is a net financial loss.

Hidden Costs: Repair Times and Parts Availability

A critical, often overlooked financial aspect of Tesla Insurance is the claims process. Tesla Insurance is integrated with Tesla Service Centers. While this can streamline communication, Tesla has historically faced criticism for long repair wait times. From a financial perspective, if your car is in the shop for two months and your insurance policy has limited “Rental Reimbursement” coverage, you may find yourself paying for a rental out-of-pocket or continuing to make high monthly car payments on a vehicle you cannot drive. These “frictional costs” must be factored into the overall value proposition of the insurance provider.

Strategic Financial Planning for Tesla Ownership

Choosing an insurance policy is a cornerstone of a sound financial strategy for any high-value asset. With a Tesla, this strategy requires a deeper dive into the total cost of ownership (TCO).

Total Cost of Ownership (TCO) Considerations

When evaluating the “how much” of Tesla insurance, it should be viewed alongside fuel savings and maintenance. A Tesla might cost $200 more per month to insure than a Toyota Camry, but it may save $250 a month in gasoline and $50 a month in oil changes and scheduled maintenance. Therefore, on a net-basis, the higher insurance cost is often offset by operational efficiencies. Financial planning for an EV should always be done on a “per-mile” basis rather than just looking at the monthly premium in isolation.

Maximizing Your ROI through Insurance Choices

To get the most out of your investment, consider the following financial moves:

- Monitor Your Score: In states where telematics are allowed, treat your Safety Score as a financial metric. Improving your score is equivalent to finding a high-yield savings account for your insurance premiums.

- Adjust Coverage Based on Depreciation: As the vehicle ages and its market value drops, reassess your collision and comprehensive coverage. For an older Model 3 with high mileage, increasing the deductible can free up cash flow for other investments.

- Gap Insurance: Because Teslas can experience rapid price fluctuations (due to Tesla’s frequent MSRP changes), ensure your financial exposure is covered. If you financed the vehicle with a low down payment, “Gap Insurance” is a vital financial tool to ensure you aren’t “underwater” if the car is totaled and the insurance payout is less than your loan balance.

In conclusion, the cost of Tesla insurance is a multifaceted financial calculation. It is defined by a blend of innovative technology and traditional risk assessment. While the premiums may be higher than those for an internal combustion engine vehicle in some scenarios, the ability to control costs through driving behavior offers a unique financial lever. By treating insurance as a dynamic component of a broader financial plan, Tesla owners can effectively manage their premiums and ensure that their transition to sustainable transport is as fiscally responsible as it is environmentally conscious.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.