New York City stands as a global epicenter of finance, culture, and innovation, attracting millions of residents and businesses. However, for anyone living or working within its five boroughs, understanding the unique tax landscape is paramount to sound financial planning. Unlike many other major American cities, New York City imposes its own distinct income tax on its residents, layered on top of federal and New York State taxes. This multi-tiered system can be complex, often catching newcomers or those unfamiliar with its intricacies by surprise. This article will demystify the New York City income tax rate, exploring its structure, who is subject to it, and how it fits into the broader financial picture for individuals and businesses operating in this vibrant metropolis. Navigating these fiscal waters effectively is a cornerstone of personal finance and business financial health for anyone connected to NYC.

Understanding New York’s Multi-Layered Tax System

Before diving specifically into the New York City income tax, it’s crucial to grasp the context of the broader tax environment in the state. Taxation in New York operates on multiple levels, each with its own rules, rates, and implications. Ignoring any one layer can lead to significant financial missteps.

The Federal Income Tax Base

At the foundation of all income taxation in the United States is the federal income tax. This is a progressive tax system, meaning higher earners pay a larger percentage of their income in taxes. The Internal Revenue Service (IRS) collects these taxes based on an individual’s adjusted gross income (AGI), applying various brackets, deductions, and credits. This federal liability is universal for all U.S. citizens and residents, regardless of which state or city they call home, forming the initial layer of tax on your earnings. Understanding your federal tax obligations is the starting point for any tax planning in New York.

New York State Income Tax: A Progressive Structure

Beyond federal taxes, New York State imposes its own income tax on its residents and on income earned within its borders by non-residents. Like the federal system, New York State’s income tax is progressive, with rates increasing as taxable income rises. The state’s tax brackets and rates are updated periodically, reflecting economic conditions and legislative changes. New York State also offers various deductions and credits that can reduce an individual’s or business’s taxable income, making careful planning essential. This state-level tax significantly contributes to the overall tax burden for New Yorkers and sets the stage for the municipal layer.

The Distinctive Role of New York City Income Tax

What truly sets New York City apart from most other major U.S. cities is its authority to levy a separate income tax on its residents. This is not a common feature; many cities rely solely on property taxes, sales taxes, or other local fees. The New York City income tax is designed to fund the extensive public services and infrastructure required to support a city of its immense size and complexity – from education and public safety to sanitation and transportation. This city-level tax is applied in addition to federal and state income taxes, further impacting the take-home pay of residents. Its existence means that individuals earning income and residing within the five boroughs (Manhattan, Brooklyn, Queens, The Bronx, and Staten Island) face a distinct and often higher overall tax burden compared to those living elsewhere in New York State or in other major U.S. cities without a local income tax.

Delving into the NYC Resident Income Tax

The New York City income tax is specifically targeted at individuals who are considered residents of the city. Understanding the definition of a resident and the progressive rate structure is crucial for accurate tax planning and compliance.

Who is Considered an NYC Resident for Tax Purposes?

Determining residency for NYC income tax purposes is critical. Generally, you are considered a New York City resident if your domicile is in the city. Your domicile is typically your permanent home, the place you intend to return to whenever you are away. Even if you spend part of the year outside the city, if your domicile remains within NYC, you are considered a resident. Furthermore, if you maintain a permanent place of abode in NYC for substantially all of the taxable year (more than 183 days) and are not domiciled in the city but spend more than 183 days in the city, you may also be treated as a statutory resident. This “statutory resident” rule can sometimes be a trap for those who split their time between NYC and other locations, making it imperative to track days spent in the city carefully. The rules are designed to capture a broad range of individuals benefiting from the city’s infrastructure and services.

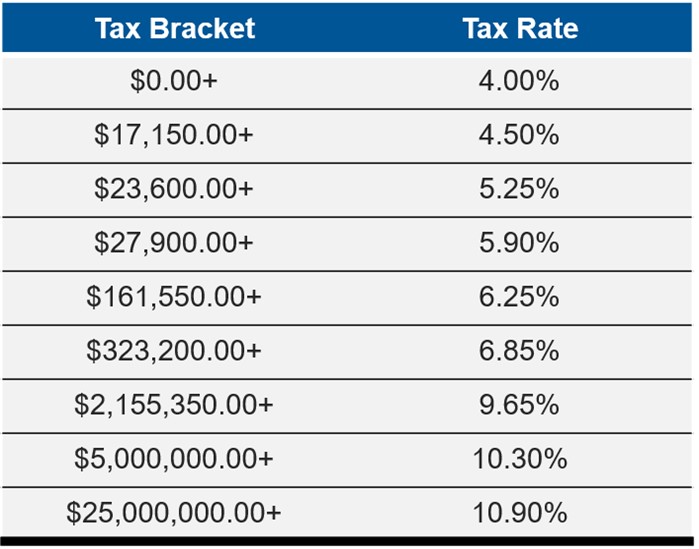

The Progressive Rate Structure for City Residents

Like federal and state taxes, New York City income tax is progressive. This means that as your taxable income increases, the percentage of that income you pay in city taxes also rises. The specific rates and brackets are subject to change by the city council and state legislature, but historically, they range from low single digits for lower income tiers to several percentage points for the highest earners. For example, as of recent tax years, the rates might range from approximately 3.078% for the lowest taxable income bracket to 3.876% or slightly higher for the top bracket. These rates apply to your New York City taxable income, which is often derived from your New York State taxable income after certain adjustments. This progressive nature ensures that the tax burden is distributed based on an individual’s ability to pay, but it also means high earners in NYC face a substantially higher combined income tax rate than residents in many other U.S. cities.

Calculating Your NYC Resident Income Tax Liability

Calculating your New York City income tax liability involves several steps. First, you determine your federal adjusted gross income (AGI). Then, you make specific modifications to arrive at your New York State AGI. From this, further modifications, deductions, and exemptions are applied to arrive at your New York State taxable income. Finally, your New York City taxable income is typically derived from your New York State taxable income, with specific NYC-related deductions or additions. Once your NYC taxable income is established, you apply the progressive city tax rates to determine your gross city tax. This process can be intricate, requiring careful attention to detail and a thorough understanding of federal, state, and city tax codes. Many residents utilize tax preparation software or enlist the services of a qualified tax professional to ensure accuracy.

Important Credits and Deductions for NYC Residents

Just as with federal and state taxes, New York City offers various credits and deductions that can reduce your overall city income tax liability. These can include deductions for certain retirement contributions, health savings accounts, and specific itemized deductions. NYC also has its own set of credits, which might include credits for dependent care, earned income, or specific educational expenses, though these can vary year by year. It is crucial for residents to explore all available credits and deductions for which they qualify. Leveraging these provisions effectively can significantly lower your effective tax rate and improve your financial standing. Staying informed about changes to these tax breaks is an ongoing responsibility for NYC residents aiming for optimal financial health.

Non-Resident Considerations: Working in NYC

While New York City directly taxes its residents’ income, the situation is different for individuals who work in the city but reside elsewhere. Understanding these distinctions is vital for commuters and remote workers alike.

New York State Tax Obligations for Non-Residents

If you work in New York City but do not reside in the city or even in New York State, you are generally still subject to New York State income tax on the income you earn within the state. This is because New York, like most states, asserts its right to tax income derived from sources within its borders, regardless of the taxpayer’s residency. Your employer will typically withhold New York State taxes from your pay. Non-residents must file a New York State income tax return to report this income and pay any taxes due, often claiming credits for taxes paid to their home state to avoid double taxation.

The Absence of a Direct NYC Non-Resident Income Tax

Crucially, New York City does not impose its separate income tax on non-residents who work within its boundaries. This is a significant distinction. If you live in New Jersey, Connecticut, or elsewhere in New York State (e.g., Westchester County or Long Island) and commute to work in Manhattan, you will pay federal and New York State income taxes on your NYC-derived income, but you will not pay New York City income tax. This absence of a direct NYC non-resident income tax is a major financial incentive for many who choose to live just outside the city while still benefiting from its job market.

The “Convenience of the Employer” Rule and Its Implications

For remote workers, the “convenience of the employer” rule in New York State can have significant implications. This rule states that if an employee’s primary office is in New York State (e.g., New York City), any work performed outside the state for the convenience of the employee (not for the necessity of the employer) is still considered New York State source income. This means that if you work remotely from another state but your employer’s office is in NYC, New York State may still consider your income as New York-sourced and therefore taxable by the state. While this primarily impacts New York State income tax, it’s a critical consideration for non-residents working for NYC-based companies, especially in the era of increased remote work. It underscores the complexity and the need for careful review of tax residency and income sourcing rules for anyone with ties to the New York job market.

Beyond Income Tax: Other NYC-Specific Taxes

While income tax is a significant component, it’s just one piece of the broader tax mosaic in New York City. Residents and businesses also contend with a variety of other local taxes that contribute to the overall cost of living and operating in the five boroughs.

Property Taxes: A Significant Local Burden

For homeowners and landlords, property taxes are one of the most substantial financial obligations in New York City. These taxes are levied by the city on real estate and are a primary source of revenue for municipal services. Property values in NYC are notoriously high, and consequently, property tax bills can be substantial, often representing a major ongoing expense. The actual tax amount depends on the property’s assessed value, the applicable tax rate, and any exemptions or abatements the property owner may qualify for. Understanding how property taxes are assessed and appealing valuations are crucial for property owners in the city.

Sales Tax in New York City

New York State imposes a statewide sales tax, and local jurisdictions, including New York City, can add their own sales tax on top of that. For consumers, this means that most purchases of goods and some services are subject to a combined sales tax rate that includes both state and city components. This rate is among the highest in the nation for a major city, making nearly every transaction slightly more expensive. While individual purchases may seem negligible, the cumulative effect of sales tax over a year can be significant for households. Certain items, like non-prepared food and prescription medications, are typically exempt from sales tax.

Business Taxes and Local Surcharges

Businesses operating in New York City face a unique array of local taxes in addition to federal and state corporate income taxes. These can include the General Corporation Tax (GCT), which is levied on corporations doing business in the city, or the Unincorporated Business Tax (UBT) for partnerships and sole proprietorships. The city also imposes various other fees, permits, and licenses that contribute to the cost of doing business. Understanding these specific business taxes is vital for entrepreneurs and established companies alike to ensure accurate financial projections and compliance. The complexity often necessitates specialized accounting and legal advice.

Payroll Taxes: The Metropolitan Commuter Transportation Mobility Tax (MCTMT)

An often-overlooked tax for both employers and employees in the New York metropolitan area is the Metropolitan Commuter Transportation Mobility Tax (MCTMT). This is a payroll tax imposed on certain employers and self-employed individuals within the Metropolitan Commuter Transportation District (MCTD), which includes New York City and several surrounding counties. The tax is calculated as a percentage of payroll expense or net earnings from self-employment. While it’s a state-level tax, its specific application to the NYC region makes it a direct financial consideration for those operating or working within the city’s economic orbit. For employers, it adds to the cost of hiring, and for self-employed individuals, it represents an additional layer of income-based taxation.

Strategies for Navigating NYC Income Tax

Given the complexities of New York City’s tax system, proactive strategies are essential for effective financial management. Without careful planning, individuals and businesses can face unnecessary burdens or missed opportunities.

Importance of Accurate Record-Keeping

The cornerstone of effective tax navigation is meticulous record-keeping. This includes maintaining organized records of all income sources, expenses (especially those that are tax-deductible), receipts, bank statements, and investment activities. For residents, tracking days spent inside and outside the city can be crucial for determining residency status. For businesses, detailed financial records are indispensable for calculating taxable income, managing payroll taxes, and demonstrating compliance with various city and state regulations. Accurate records not only simplify tax preparation but also provide crucial documentation in the event of an audit, safeguarding against potential penalties or discrepancies.

Leveraging Tax Software and Professionals

Navigating the multi-layered federal, state, and city tax codes can be overwhelming for many. Utilizing reputable tax preparation software can help automate calculations, identify potential deductions, and ensure correct form submission. However, for individuals with complex financial situations, high net worth, or for businesses, engaging a qualified tax professional (such as a Certified Public Accountant or an enrolled agent) is often the most prudent strategy. These professionals possess in-depth knowledge of current tax laws, can offer personalized advice, and help identify advanced tax planning opportunities that might otherwise be missed. Their expertise is particularly valuable in deciphering the nuances of New York City’s specific tax regulations.

Tax Planning for Major Life Events

Major life events — such as getting married, having children, buying a home, starting a business, or retiring — all have significant tax implications. Proactive tax planning around these events can lead to substantial savings or prevent unexpected tax liabilities. For instance, purchasing a home in NYC can introduce new property tax considerations and potential deductions for mortgage interest. Starting a business brings with it a host of new business tax obligations. Understanding how these life changes impact your federal, state, and city tax situation is crucial. Consulting with a financial advisor or tax professional before these events occur can help structure decisions in a tax-efficient manner.

Staying Informed About Tax Law Changes

Tax laws are not static; they evolve frequently at federal, state, and local levels. Legislative bodies in New York City and New York State regularly introduce new bills, adjust tax rates, and modify existing regulations. Staying informed about these changes is paramount for effective tax planning. Subscribing to financial news, following tax authority updates, and regularly reviewing tax professional insights can help individuals and businesses adapt their strategies accordingly. Ignoring new laws can lead to non-compliance or missed opportunities for tax optimization. A proactive approach to understanding the dynamic tax environment is a hallmark of strong financial acumen in New York City.

In conclusion, understanding “what is the New York City income tax rate” extends far beyond a simple percentage. It encompasses a comprehensive grasp of a unique, multi-layered tax system that integrates federal, state, and municipal obligations. For residents, this means navigating progressive city income taxes, while non-residents working in the city must consider state taxes and specific sourcing rules. Beyond income, property, sales, and various business taxes further shape the financial landscape of New York City. By embracing meticulous record-keeping, leveraging expert advice, engaging in proactive tax planning for life events, and staying abreast of legislative changes, individuals and businesses can effectively navigate this complex environment, ensuring financial health and compliance in one of the world’s most economically significant cities.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.