The national interest rate is a concept often discussed in financial news, yet its precise meaning and far-reaching implications can remain elusive to many. Far from a single, static figure, the “national interest rate” typically refers to the benchmark interest rate set by a country’s central bank, a powerful entity tasked with maintaining economic stability. This rate acts as a foundational cost of money, influencing everything from the interest you earn on your savings to the rate you pay on your mortgage, credit card, or business loan. Understanding this pivotal economic indicator is crucial for anyone navigating personal finance, investing, or running a business. It is a cornerstone of monetary policy, designed to steer the economy towards desired outcomes such as stable prices, maximum employment, and sustainable growth.

Demystifying the National Interest Rate: Core Concepts

At its heart, an interest rate is the cost of borrowing money or the reward for saving it. When we speak of the “national interest rate,” we are typically referring to the policy rate set by the country’s central bank. This rate doesn’t directly dictate every single interest rate in the economy, but it serves as a critical benchmark that influences all others.

The Central Bank’s Pivotal Role

In most developed economies, the central bank is the primary authority responsible for monetary policy. For instance, in the United States, this role falls to the Federal Reserve (the “Fed”); in the Eurozone, it’s the European Central Bank (ECB); and in the United Kingdom, it’s the Bank of England (BoE). These institutions are independent of government influence to a significant degree, allowing them to make decisions based purely on economic data and their mandates. Their key mechanism for influencing the economy is the setting of a target range for their primary policy rate. This rate is the interest rate at which commercial banks can borrow or lend excess reserves to each other overnight, directly impacting the availability and cost of money within the banking system.

Key Policy Rates: Benchmarks for the Economy

Different central banks have different names for their benchmark rates, but their function is largely similar.

- Federal Funds Rate (U.S.): The target rate for interbank overnight lending of reserves. While the Fed doesn’t directly set this rate, it influences it through open market operations (buying and selling government securities). Changes to this rate filter through the entire financial system.

- Main Refinancing Operations Rate (Eurozone): The rate at which commercial banks can borrow money from the ECB for one week against collateral. This is a key rate for guiding short-term market rates.

- Bank Rate (U.K.): The interest rate the Bank of England charges other banks for lending money. It is the official cost of borrowing money for banks and, therefore, influences the rates they offer to customers.

These policy rates are not the rates individuals or businesses pay directly on loans, but rather the base from which commercial banks set their own prime rates, mortgage rates, and savings rates. For example, if the central bank raises its policy rate, it becomes more expensive for commercial banks to borrow money, and they, in turn, pass these higher costs on to their customers.

Nominal vs. Real Rates: A Crucial Distinction

When discussing interest rates, it’s vital to differentiate between nominal and real rates.

- Nominal Interest Rate: This is the advertised interest rate, the one you see on a loan agreement or a savings account statement. It’s the stated percentage return or cost without adjusting for inflation.

- Real Interest Rate: This rate accounts for inflation. It represents the true cost of borrowing or the true return on saving after considering the erosion of purchasing power due to rising prices. The formula is approximately: Real Interest Rate = Nominal Interest Rate – Inflation Rate.

For investors and savers, the real interest rate is more important because it reflects the actual increase in their purchasing power. A high nominal interest rate on savings might seem attractive, but if inflation is even higher, the real return could be negative, meaning your money is losing value over time. Conversely, borrowers might face higher nominal rates, but if inflation is robust, the real cost of their debt could be lower than it appears.

The Mechanics of Monetary Policy: How Rates are Set

The decision to adjust the national interest rate is not taken lightly. It involves extensive analysis, debate, and forecasting by the central bank’s monetary policy committee. These decisions are rooted in the central bank’s mandate, which typically involves balancing multiple, sometimes conflicting, economic objectives.

Economic Indicators Guiding Decisions

Central banks meticulously monitor a vast array of economic indicators to gauge the health and trajectory of the economy. Key data points include:

- Inflation Rates: Measured by indices like the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE), inflation is arguably the most critical factor. If inflation is rising above the central bank’s target (often around 2%), rates are likely to be raised to cool down the economy and curb price increases.

- Employment Data: Unemployment rates, job creation numbers, wage growth, and labor force participation rates provide insights into the strength of the labor market. A strong labor market might signal economic overheating, potentially prompting rate hikes, while a weak one might necessitate rate cuts to stimulate activity.

- Economic Growth (GDP): Gross Domestic Product (GDP) growth indicates the overall expansion or contraction of the economy. Robust growth might suggest inflationary pressures, whereas sluggish growth could signal a need for stimulus through lower rates.

- Consumer Spending and Business Investment: These indicators reflect demand within the economy. Strong demand can lead to inflation, while weak demand might require lower rates to encourage spending and investment.

- Housing Market Data: Home sales, prices, and construction starts can reveal broader economic trends and consumer confidence.

- Global Economic Conditions: International trade, currency movements, and economic performance of major trading partners can also influence domestic monetary policy.

Navigating the Dual Mandate: Inflation and Employment

Many central banks operate under a “dual mandate,” aiming to achieve both stable prices (low and predictable inflation) and maximum sustainable employment. This balancing act is complex.

- Combating Inflation (Tightening Policy): When inflation is too high, the central bank may raise interest rates. This makes borrowing more expensive, discouraging consumer spending and business investment, thereby reducing overall demand in the economy and putting downward pressure on prices. This is known as “tightening” monetary policy.

- Stimulating Growth and Employment (Loosening Policy): When the economy is sluggish or unemployment is high, the central bank may lower interest rates. This makes borrowing cheaper, encouraging individuals to take out loans for homes and cars, and businesses to invest and hire. This increased demand helps boost economic activity and create jobs. This is known as “loosening” or “accommodative” monetary policy.

The challenge lies in the trade-offs. Aggressively fighting inflation might lead to higher unemployment, while prioritizing employment could risk igniting inflation. Central banks strive for a delicate balance, adjusting rates incrementally to guide the economy toward its desired equilibrium.

Tools Beyond the Policy Rate

While adjusting the benchmark interest rate is the primary tool, central banks have other mechanisms to implement monetary policy:

- Quantitative Easing (QE) and Quantitative Tightening (QT): During periods of severe economic distress or when interest rates are already at zero (the “zero lower bound”), central banks may resort to QE. This involves buying large quantities of government bonds and other securities to inject liquidity into the financial system, lower long-term interest rates, and encourage lending and investment. Conversely, QT involves reducing the balance sheet by selling assets or letting them mature, effectively withdrawing liquidity.

- Reserve Requirements: The percentage of deposits that banks must hold in reserve, rather than lend out. While less frequently adjusted now, lowering reserve requirements can free up funds for lending.

- Forward Guidance: Communicating the central bank’s future intentions regarding monetary policy to influence market expectations and long-term interest rates. This transparency can help manage market volatility and guide economic behavior.

Far-Reaching Impact: How National Rates Influence Your Money

The national interest rate is not an abstract economic concept; its ripples spread throughout the financial system, directly affecting individuals, businesses, and the broader economy. For anyone managing personal finances or operating a business, understanding these impacts is paramount.

Borrowing Costs: Mortgages, Loans, and Credit

Perhaps the most direct and visible impact of national interest rate changes is on borrowing costs.

- Mortgages: Adjustable-rate mortgages (ARMs) typically see immediate changes when the central bank adjusts its policy rate. Even fixed-rate mortgages are indirectly affected, as long-term rates tend to move in tandem with expectations for future short-term rates. A hike in the national rate generally means higher monthly mortgage payments for ARM holders and higher rates for new fixed-rate borrowers, making homeownership more expensive.

- Credit Cards: Most credit cards have variable interest rates tied to a benchmark like the prime rate, which directly correlates with the central bank’s policy rate. When the central bank raises rates, credit card APRs typically follow suit, making it more costly to carry a balance.

- Personal Loans and Auto Loans: While often fixed, rates for new personal and auto loans will generally rise or fall in response to national rate changes.

- Business Loans: For businesses, particularly those reliant on variable-rate lines of credit or seeking new capital, changes in the national rate directly impact their cost of borrowing. Higher rates can deter investment and expansion, while lower rates encourage it.

Savings and Investments: Opportunities and Challenges

For savers and investors, changes in the national interest rate present a different set of dynamics.

- Savings Accounts and Certificates of Deposit (CDs): When national rates rise, banks typically offer higher interest rates on savings accounts and CDs, making it more attractive to save money. Conversely, in a low-rate environment, returns on traditional savings vehicles can be minimal.

- Bonds: Bond prices and interest rates have an inverse relationship. When the national interest rate rises, newly issued bonds offer higher yields, making existing bonds with lower yields less attractive. This causes the price of existing bonds to fall. Conversely, when rates fall, existing bonds with higher yields become more valuable, and their prices rise.

- Stock Market: The impact on stocks is more nuanced. Higher interest rates can be negative for stocks because they increase borrowing costs for companies, reduce consumer spending (which hurts corporate earnings), and make bonds more competitive as an alternative investment. However, if rate hikes signal a strong economy, earnings might still grow. Lower rates, conversely, can boost corporate profits and make stocks more appealing relative to bonds.

- Real Estate Investment: Higher rates generally cool down the housing market by making mortgages more expensive, potentially leading to slower price appreciation or even declines. For real estate investors, this can impact property values and rental yields.

Business Decisions and Economic Growth

Beyond borrowing costs, the national interest rate profoundly influences the broader business landscape and overall economic growth.

- Investment and Expansion: Lower interest rates incentivize businesses to borrow money for capital investments (new factories, equipment, research and development), leading to job creation and economic expansion. Higher rates make such investments more costly and riskier, potentially slowing growth.

- Consumer Demand: As borrowing becomes cheaper or more expensive for consumers, their ability and willingness to spend on big-ticket items like homes, cars, and durable goods change. This directly impacts businesses that rely on consumer demand.

- Profitability: For companies with significant variable-rate debt, changes in interest rates can directly impact their profitability. Higher rates mean higher interest expenses, eroding profit margins.

- Inflation Expectations: The central bank’s actions also influence inflation expectations. If businesses and consumers expect inflation to be controlled, they can make more confident long-term financial plans.

International Implications: Trade and Currency Value

The national interest rate also has a significant bearing on a country’s currency value and international trade.

- Currency Strength: Higher national interest rates typically make a country’s currency more attractive to foreign investors seeking higher returns on their investments (e.g., bonds). This increased demand can strengthen the currency. Conversely, lower rates can weaken it.

- Trade Balance: A stronger currency makes a country’s exports more expensive for foreign buyers and imports cheaper for domestic consumers. This can lead to a widening trade deficit. A weaker currency has the opposite effect, potentially boosting exports and narrowing the trade deficit.

- Capital Flows: Higher rates can attract foreign capital, while lower rates might encourage capital outflow, impacting a country’s financial stability and investment landscape.

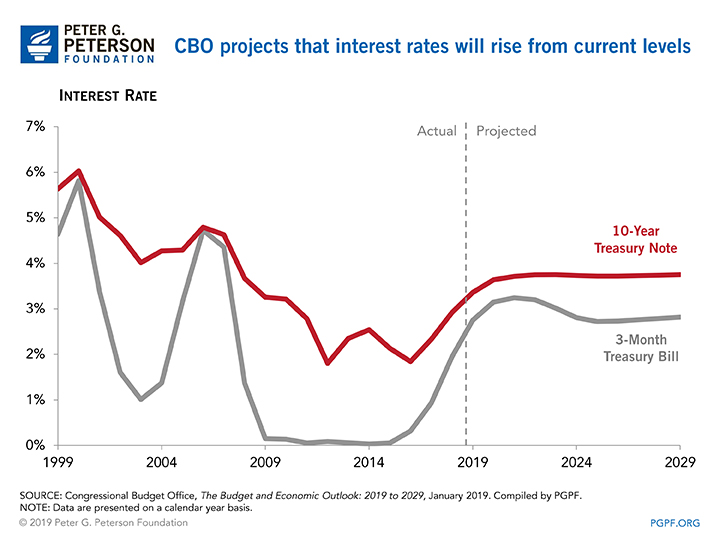

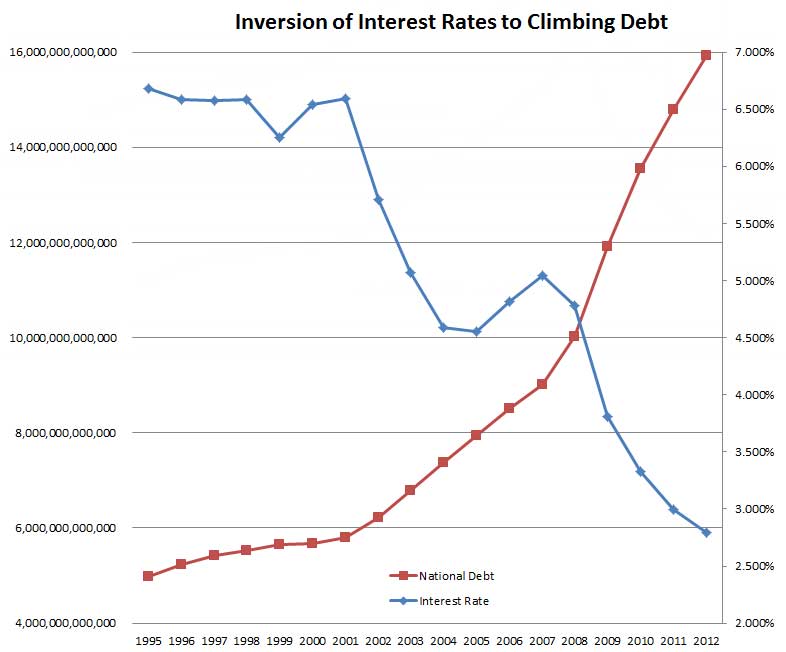

Historical Perspectives and Future Outlook

The national interest rate is not static; it has fluctuated dramatically throughout history, reflecting evolving economic conditions and central bank philosophies. Understanding these patterns offers valuable insights for anticipating future trends.

Decades of Rate Fluctuations: Lessons Learned

- 1970s and Early 1980s: This era saw extremely high inflation, prompting central banks (notably the Federal Reserve under Paul Volcker) to aggressively raise rates to unprecedented levels to bring prices under control, even at the cost of significant economic recession. This period underscored the central bank’s commitment to price stability.

- The Great Moderation (Mid-1980s to 2007): Characterized by relatively low inflation and stable economic growth, this period saw interest rates generally trending downwards, punctuated by targeted adjustments to manage economic cycles.

- The Global Financial Crisis (2008-2009) and Beyond: Central banks slashed rates to near zero and implemented unconventional policies like quantitative easing to prevent a complete economic collapse and stimulate recovery. This demonstrated the limits of traditional interest rate policy and the innovative measures central banks can take.

- The Post-Pandemic Era: The COVID-19 pandemic introduced new challenges, leading to supply chain disruptions, massive fiscal stimulus, and a subsequent surge in inflation. Central banks worldwide responded with rapid and significant rate hikes, marking a return to a more aggressive tightening cycle after years of low rates.

These historical cycles teach us that interest rates are dynamic tools, constantly adapted to prevailing economic circumstances. The core lesson for individuals and businesses is that the cost of money is rarely constant.

The Ever-Evolving Economic Landscape

The future trajectory of national interest rates will depend on a confluence of factors, including:

- Inflation Persistence: Whether current inflationary pressures prove transitory or become deeply entrenched.

- Economic Growth Resilience: The ability of economies to withstand higher rates without falling into deep recession.

- Geopolitical Events: Conflicts, trade wars, and global supply chain disruptions can all impact inflation and growth, influencing central bank decisions.

- Technological Advancements: Innovation can boost productivity and potentially dampen long-term inflationary pressures.

- Demographic Shifts: Aging populations and changes in labor force participation can affect economic potential and wage growth.

Central banks will continue to navigate these complexities, striving to achieve their mandates in an increasingly interconnected and unpredictable world. Their decisions will be closely watched by markets, governments, and, most importantly, by individuals and businesses whose financial well-being is directly tied to the cost of money.

![]()

Staying Informed: A Prudent Approach to Personal Finance

For individuals and businesses alike, staying informed about the national interest rate and the central bank’s monetary policy is not merely academic; it is a fundamental aspect of prudent financial management.

- Budgeting and Debt Management: Understand how rate changes affect your variable-rate debt (credit cards, ARMs) and plan accordingly. In a rising rate environment, prioritizing debt repayment can save significant money.

- Saving and Investing: Adjust your savings strategy to take advantage of higher returns on traditional savings vehicles when rates rise. Reassess your investment portfolio, considering how different asset classes perform in various rate environments. Diversification remains key.

- Major Purchases: If contemplating a large purchase requiring financing (home, car, business expansion), be aware of the prevailing interest rate environment and its potential future direction. Locking in a favorable fixed rate when available can provide certainty.

- Business Planning: Businesses should factor interest rate forecasts into their financial planning, capital expenditure decisions, and working capital management.

In conclusion, the “national interest rate,” primarily the central bank’s policy rate, is a vital economic lever. It is a complex mechanism, influenced by a myriad of economic data and wielded with the dual aim of price stability and full employment. Its impact on borrowing costs, investment returns, business decisions, and overall economic health is profound and far-reaching, making a solid understanding of this concept indispensable for sound financial decision-making in any sphere.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.