The question “What is the housing interest rate today?” is perhaps the most significant inquiry in the modern financial world for homeowners, prospective buyers, and real estate investors alike. However, the answer is rarely a single, static number. Housing interest rates are a dynamic reflection of the global economy, domestic fiscal policy, and individual financial health. In a shifting economic climate where inflation and Federal Reserve policies dominate the headlines, understanding the nuances of mortgage rates is essential for making informed personal finance decisions.

In this comprehensive guide, we will explore the mechanisms that drive housing interest rates, how current market trends are reshaping the real estate landscape, and the strategies you can employ to secure the best possible terms for your financial future.

Understanding How Mortgage Rates Are Determined

To understand why housing interest rates are where they are today, one must look beyond the local bank branch. Mortgage rates are influenced by a complex interplay of macroeconomic factors that dictate the cost of borrowing across the entire economy.

The Influence of the Federal Reserve and Monetary Policy

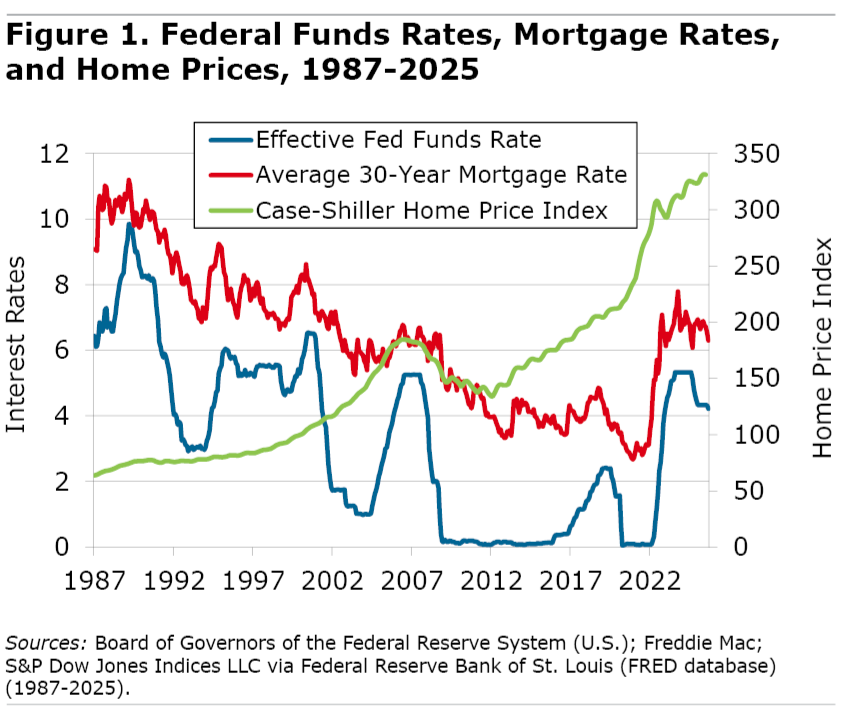

While the Federal Reserve does not set mortgage rates directly, its influence is profound. The “Fed” controls the federal funds rate—the interest rate at which commercial banks borrow and lend to one another overnight. When the Fed raises this rate to combat inflation, the cost of borrowing increases across the board. Banks pass these higher costs on to consumers in the form of higher interest rates for credit cards, personal loans, and, most significantly, mortgages. Conversely, when the economy slows, the Fed may lower rates to stimulate borrowing and investment.

The Relationship with the 10-Year Treasury Yield

If you want to track where mortgage rates are headed on a daily basis, look at the 10-year Treasury yield. There is a strong historical correlation between the yield on government bonds and the interest rates on 30-year fixed-rate mortgages. Investors view both as long-term, relatively low-risk investments. When investors demand higher yields on Treasury bonds due to inflation concerns or economic growth, mortgage lenders must also raise their rates to remain competitive and attract capital.

Inflation and the Purchasing Power of the Dollar

Inflation is the silent enemy of the fixed-rate mortgage. If a lender issues a 30-year loan at 4%, but inflation rises to 6%, the lender is essentially losing purchasing power over time. To compensate for this risk, lenders increase interest rates during periods of high inflation. Today’s housing interest rates are a direct reflection of the market’s ongoing battle to stabilize the Consumer Price Index (CPI) and return to a predictable economic baseline.

Current Market Trends and Their Financial Impact

The housing market has undergone a radical transformation over the last few years. Moving from the historic lows of the early 2020s to the current elevated environment has created a unique set of challenges and opportunities for those in the “Money” niche.

The “Lock-In” Effect and Inventory Constraints

One of the most significant trends resulting from today’s interest rates is the “lock-in” effect. Many existing homeowners are currently sitting on mortgage rates between 2.5% and 4%. For these individuals, selling their current home and buying a new one at today’s rates (which may be 6.5% or higher) represents a massive increase in monthly housing costs. This has led to a stagnation in housing inventory, as owners are reluctant to move, which in turn keeps home prices high despite the higher cost of borrowing.

Comparative Historical Context

While today’s rates may feel high compared to the 3% rates of 2021, a historical perspective offers a different view. In the early 1980s, mortgage rates peaked at over 18%. Throughout the 1990s and 2000s, rates in the 6% to 8% range were considered standard. Understanding that current rates are closer to the historical average—rather than an unprecedented anomaly—can help buyers adjust their expectations and focus on the long-term appreciation of real estate as an asset class.

The Shift Toward Adjustable-Rate Mortgages (ARMs)

As fixed rates have climbed, there has been a renewed interest in Adjustable-Rate Mortgages. These loans typically offer a lower “teaser” rate for an initial period (such as 5, 7, or 10 years) before adjusting based on market conditions. For savvy financial planners who intend to sell or refinance before the adjustment period kicks in, ARMs can be a strategic tool to lower initial monthly payments and maintain cash flow.

Factors That Influence Your Individual Interest Rate

The “national average” rate reported in the news is a benchmark, but the actual rate you are offered depends heavily on your personal financial profile. Understanding these variables allows you to take proactive steps to improve your borrowing power.

Credit Score: The Ultimate Financial Lever

Your FICO score is the single most important factor in determining your interest rate. Lenders use this score to assess the risk of default. A borrower with a score of 760 or higher will almost always receive the “prime” rate, while someone with a score in the low 600s might face rates that are 1% to 2% higher. Over the life of a 30-year loan, that small percentage difference can equate to hundreds of thousands of dollars in interest.

The Loan-to-Value (LTV) Ratio

The size of your down payment significantly impacts your risk profile. A higher down payment results in a lower LTV ratio, which makes lenders more comfortable. Generally, a down payment of 20% or more eliminates the need for Private Mortgage Insurance (PMI) and can help you secure a slightly lower interest rate. For investors, LTV is even more critical, as investment property loans typically require higher equity stakes than primary residences.

Debt-to-Income (DTI) and Financial Stability

Lenders don’t just look at what you make; they look at what you owe. Your DTI ratio—the percentage of your gross monthly income that goes toward paying debts—helps lenders determine if you can afford the mortgage payment. A lower DTI suggests financial stability and can lead to more favorable loan terms and a smoother underwriting process.

Strategic Financial Planning in a High-Rate Environment

In the world of personal finance, “waiting for rates to drop” is often a losing strategy. Instead, successful participants in the real estate market employ specific financial maneuvers to mitigate the impact of current rates.

The “Marry the House, Date the Rate” Philosophy

This popular adage suggests that if you find the right property at a fair price, you should proceed with the purchase regardless of the current interest rate. The logic is that you can always refinance your mortgage if rates drop in the future, but you cannot change the purchase price of the home. This strategy relies on the assumption that home values will continue to appreciate, and that the opportunity cost of waiting (i.e., paying rent or missing out on equity growth) exceeds the cost of the higher interest rate.

Buying Down the Rate with Points

Mortgage points, also known as discount points, allow you to pay an upfront fee at closing to “buy down” your interest rate. One point typically costs 1% of the total loan amount and lowers your interest rate by about 0.25%. This is an excellent strategy for those who plan to stay in their home for a long time, as the monthly savings will eventually outweigh the initial cost of the points.

The Importance of Shopping Multiple Lenders

Many consumers make the mistake of only getting a quote from their primary bank. However, mortgage rates and closing costs can vary significantly between retail banks, credit unions, and online mortgage lenders. By obtaining at least three different Loan Estimates, you can leverage competition to secure a lower rate or reduced fees, potentially saving thousands over the life of the loan.

The Long-Term Outlook for Housing Finance

Predicting the exact movement of housing interest rates is impossible, but we can look at economic indicators to gauge the direction of the wind. As the Federal Reserve continues to monitor labor market data and inflation reports, the market anticipates a period of stabilization.

For the disciplined investor and the prepared homebuyer, today’s interest rates are simply a variable to be managed rather than an insurmountable barrier. By focusing on credit health, maximizing down payments, and utilizing tools like rate locks and points, you can navigate the complexities of the mortgage market with confidence.

In conclusion, “the housing interest rate today” is more than just a percentage; it is a reflection of the current economic pulse. While the era of 3% mortgages may be in the rearview mirror, the fundamental value of real estate as a pillar of personal wealth remains unchanged. By staying informed and strategically managing your finances, you can turn today’s market conditions into a foundation for long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.