In the rapidly evolving landscape of fintech, the traditional “piggy bank” has undergone a digital transformation. Cash App, a leader in the peer-to-peer (P2P) payment sector, has consistently introduced features designed to simplify the movement of money. One of the most impactful, yet often misunderstood, concepts within the ecosystem is the “Pool.” Whether used for collective gifting, shared household expenses, or collaborative savings goals, understanding how to pool money on Cash App is essential for anyone looking to optimize their personal finance strategy in a social world.

Managing money is no longer a solitary endeavor. As we move toward a “social finance” model, the ability to aggregate funds from multiple sources into a single, transparent ledger is a vital tool for financial literacy and efficiency. This article explores the mechanics of pooling funds on Cash App, the strategic advantages for your personal budget, and the security protocols that keep your collective wealth safe.

Understanding the Mechanism of Cash App Pools

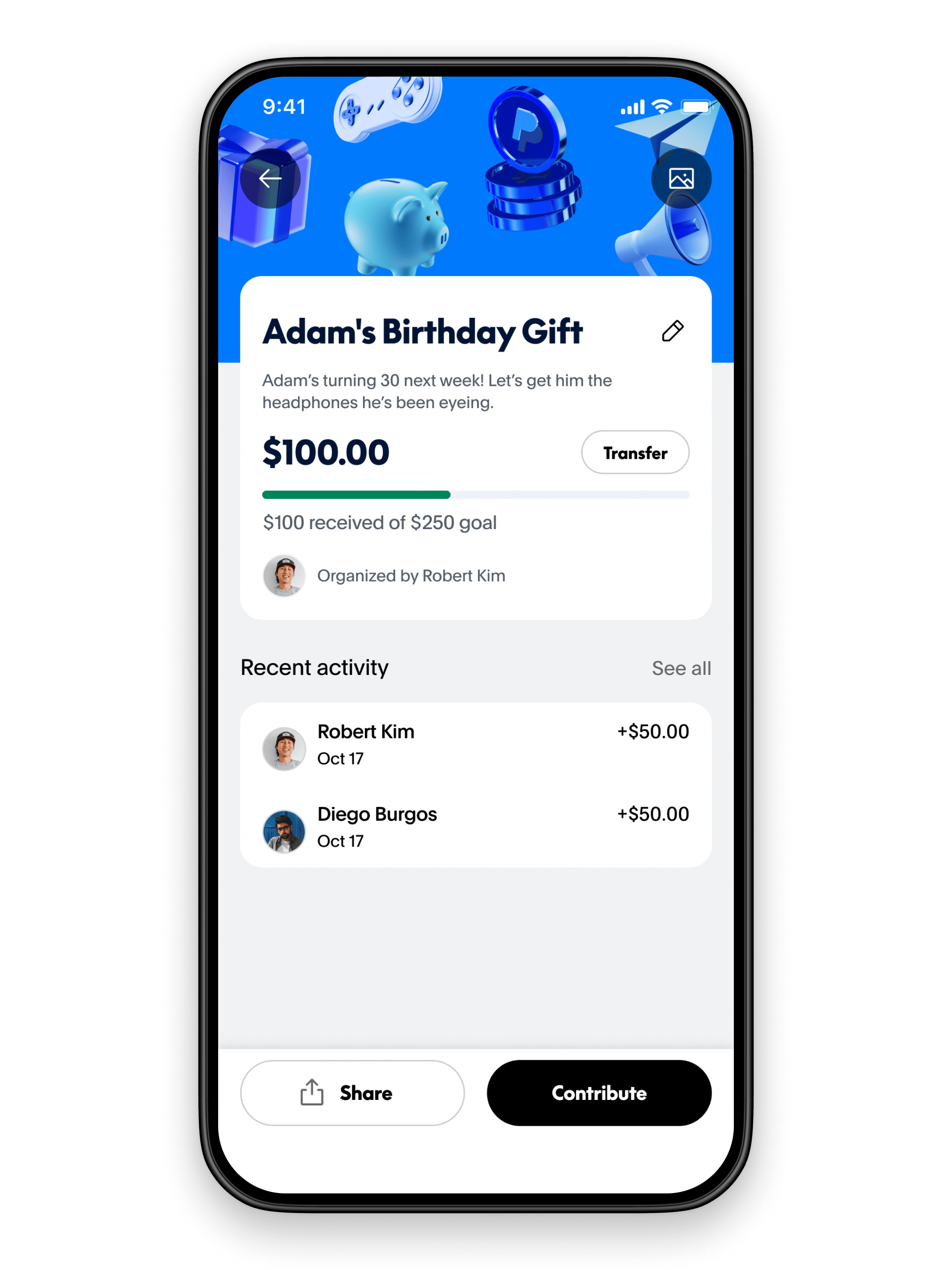

To grasp the concept of a “pool” on Cash App, one must first understand the shift from individual transactions to collective funding. While Cash App initially gained fame for simple one-to-one transfers, the “Pool” functionality (often integrated via the “Request” and “Savings” features) allows multiple users to contribute to a central financial objective.

The Concept of Collaborative Finance

Collaborative finance is a subset of personal finance that emphasizes transparency and shared responsibility. In the context of Cash App, a pool acts as a digital repository where funds are gathered for a specific purpose. Unlike a standard personal balance, a pool is often earmarked for a “social contract”—an agreement between friends, family, or colleagues to fund a specific event or purchase.

This mechanism removes the friction of “who owes whom.” By designating a central organizer (the “Pool Lead”), the app facilitates a streamlined flow of capital. The pool lead utilizes their account as the hub, leveraging Cash App’s intuitive interface to track incoming micro-contributions and ensure that the total sum meets the intended financial target.

How Cash App Facilitates Group Contributions

The technical execution of a pool relies on the “Request” and “Activity” tabs. To start a pool, an individual typically initiates a series of requests to the involved parties. However, the sophistication lies in the tracking. Cash App provides a real-time ledger that allows the organizer to see exactly who has contributed and who hasn’t, effectively serving as a digital bookkeeper.

Furthermore, Cash App’s integration with traditional banking systems via “Add Cash” and “Cash Out” features ensures that these pooled funds remain liquid. Whether you are pulling money from a linked debit card or shifting funds from your “Savings” folder into the main “Cash Balance” for a group purchase, the ecosystem is designed to minimize the time-to-value for group capital.

Financial Benefits of Using Pools for Personal Budgeting

Incorporating group funding into your broader financial plan can lead to significant improvements in cash flow management. By using digital pools, individuals can avoid the “debt lag” that often occurs when one person pays for a group expense and waits weeks to be reimbursed.

Streamlining Shared Expenses and Bill Splitting

For many young professionals and students, shared living expenses represent a significant portion of their monthly outgoings. Rent, utilities, and grocery bills can be complex to manage when multiple parties are involved. A Cash App pool simplifies this by creating a centralized point of collection.

When a pool is utilized for recurring expenses, it serves as a “buffer” for your personal bank account. Instead of one individual’s balance taking a massive hit when the rent is due, the pool ensures that the funds are aggregated well in advance. This practice promotes financial discipline among all members of the group, as the transparent nature of the app’s activity feed holds everyone accountable to the shared budget.

Goal-Oriented Savings: Crowdfunding for Life Events

One of the most powerful applications of the pooling concept is in “milestone savings.” Whether it is a wedding gift, a milestone birthday trip, or a charitable donation, pooling money allows a group to achieve a higher purchasing power than any single individual could manage alone.

From a personal finance perspective, this is an exercise in “sinking funds.” By setting a goal and pooling resources over time, the financial burden is distributed. This prevents “budget shock”—the sudden depletion of savings due to an unplanned social obligation. Using Cash App to manage these funds ensures that the money is kept separate from daily spending money, reducing the temptation to dip into the group’s capital for personal use.

Strategic Wealth Management within the Cash App Ecosystem

As you accumulate larger sums within a pool, it is important to view these funds through the lens of strategic wealth management. It is not just about collecting money; it is about managing that capital with the same rigor you would apply to an investment portfolio or a high-yield savings account.

Security and Transparency in Shared Digital Wallets

Financial security is the cornerstone of any pooling arrangement. Cash App employs high-level encryption and fraud detection to protect users’ balances. When managing a pool, the “Organizer” has a fiduciary responsibility to the group. Fortunately, the app’s architecture supports this by providing a clear paper trail.

Every contribution to the pool is timestamped and recorded. This transparency is vital for maintaining trust within a social or professional group. Moreover, the ability to set up “Security Locks” (requiring a PIN or Touch ID for every transfer) adds a layer of protection against unauthorized “Cash Outs.” For the pool to be successful, participants must feel confident that their capital is being handled with institutional-grade security.

Integrating Pools into Your Long-Term Financial Plan

While Cash App is often viewed as a “spending” tool, its “Savings” and “Bitcoin” features allow for more sophisticated financial maneuvers. A sophisticated user might pool funds for a group investment or use the “Round Up” feature on the Cash Card to grow a communal pot passively.

By treating the pool as a micro-business or a dedicated fund, you can better track your “Net Outflow” on social activities. Insightful budgeting requires knowing exactly where every dollar goes; pooling communal costs makes this tracking much easier. Instead of seeing twenty small transactions to different friends, you see one dedicated “Pool” contribution, allowing for cleaner categorization in your monthly financial review.

Optimizing Your Cash App Pool for Maximum Efficiency

To get the most out of the pooling feature, one must move beyond the basics and adopt best practices used by financial managers and project coordinators. Efficiency in digital finance is about reducing “friction” and maximizing the “velocity of money.”

Best Practices for Managing Group Funds

- Designate a Single Point of Contact: To avoid confusion, one person should act as the “Treasurer.” This person is responsible for initiating requests and providing updates to the group.

- Set Hard Deadlines: In any financial pool, “liquidity timing” is everything. Set clear deadlines for contributions to ensure the funds are available when the bill or purchase is due.

- Use Descriptive Notes: Cash App allows you to add notes to payments. Always use clear, professional labeling (e.g., “July Rent – Unit 4B” or “Hawaii Trip Fund”) to ensure the ledger remains easy to audit.

- Verify Identities: Ensure everyone in the pool has a “Verified” account. This increases the transaction limits and provides an extra layer of security for the group’s collective assets.

Avoiding Common Pitfalls in Social Finance

The biggest risk in pooling money is the “social default”—when a member of the group fails to contribute their share. To mitigate this, successful pool managers often use the “Request” feature as a gentle nudge. Additionally, it is wise to keep the pool’s purpose narrow and well-defined.

Another common pitfall is the failure to account for “transfer times.” While Cash App-to-Cash App transfers are instant, moving that money to a traditional bank account (unless using “Instant Deposit” for a fee) can take 1-3 business days. A savvy financial manager will always build in a 48-hour “buffer” to ensure the funds are truly liquid when they are needed for an external payment.

Conclusion: The Future of Communal Capital

The “Pool” concept on Cash App is more than just a convenience; it is a reflection of a broader shift toward communal capital and transparent financial management. By leveraging these tools, you can transform the way you interact with your social circle’s finances, moving from a state of reactive “debt-chasing” to a state of proactive, strategic budgeting.

As we continue to navigate an increasingly digital economy, the ability to aggregate, manage, and deploy funds collectively will become a hallmark of the financially savvy individual. Whether you are saving for a collective dream or simply trying to keep the lights on in a shared apartment, mastering the art of the Cash App pool is a critical step in your journey toward total financial control. By combining the speed of modern technology with the discipline of traditional personal finance, you can ensure that your money—and the money of your community—is always working toward its highest and best use.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.