In the landscape of American personal finance and macroeconomics, the definition of “poverty” is not merely a social observation; it is a critical financial metric. For policymakers, financial advisors, and the general public, understanding what constitutes poverty in the United States is essential for navigating the complexities of social safety nets, tax implications, and the broader economic health of the nation. While the concept of poverty might seem subjective, the U.S. government utilizes precise mathematical formulas to determine who falls below the line of economic self-sufficiency.

This article explores the financial structures that define poverty in the US, the difference between various federal measures, and the economic challenges that these metrics often fail to capture in a modern, high-inflation environment.

The Dual Architecture of Federal Poverty Measures

To understand how poverty is calculated in the US, one must first distinguish between the two primary measures used by the government. Although they are related, they serve distinct purposes in the realm of business finance and public administration.

The Census Bureau Poverty Thresholds

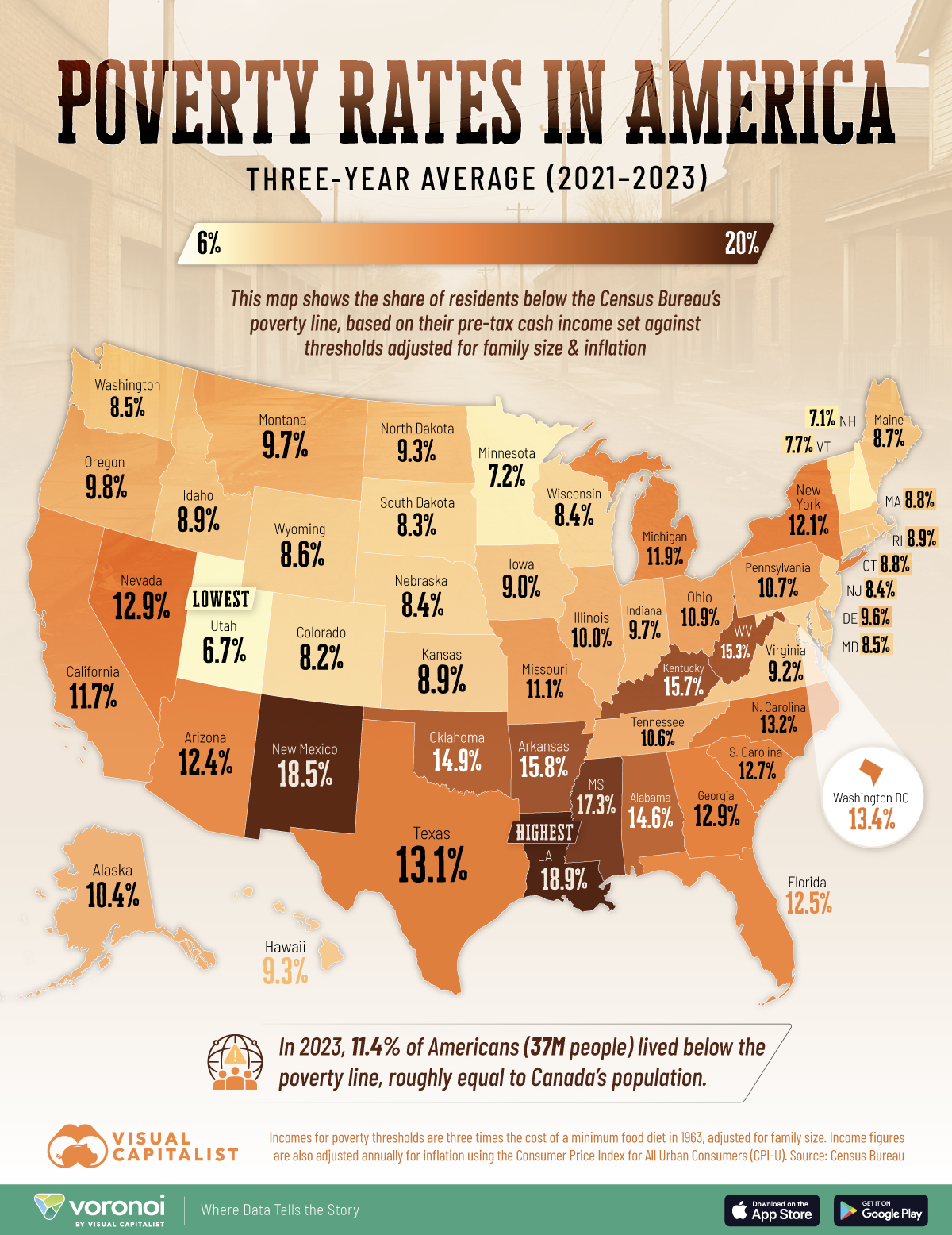

The Poverty Thresholds are the original version of the federal poverty measure. Updated annually by the Census Bureau, these thresholds are primarily used for statistical purposes—tracking the number of people in poverty across the country. They are calculated based on family size, the number of children, and the age of the householder.

The thresholds are strictly a financial snapshot. They do not vary geographically, meaning the threshold for a family of four in rural Mississippi is the same as for a family in San Francisco. This statistical tool allows economists to track poverty trends over decades, providing a baseline for analyzing the effectiveness of economic policies and national financial health.

The HHS Poverty Guidelines

While the Census Bureau tracks the data, the Department of Health and Human Services (HHS) issues the “Poverty Guidelines.” These are the figures that most Americans interact with in their daily financial lives. These guidelines are a simplified version of the thresholds and are used to determine eligibility for various federal programs, such as the Supplemental Nutrition Assistance Program (SNAP), Medicaid, and the Children’s Health Insurance Program (CHIP).

For a single individual in 2024, the poverty guideline typically sits around $15,060, while for a family of four, it is approximately $31,200 (with variations for Alaska and Hawaii). From a personal finance perspective, these numbers are the “gatekeepers” to essential subsidies that can significantly alter a household’s monthly budget.

The Orshansky Paradox: The History of the Calculation

The financial formula used to determine these thresholds dates back to the early 1960s, developed by Mollie Orshansky of the Social Security Administration. The calculation was based on the “Economy Food Plan”—the lowest cost for a nutritionally adequate diet—multiplied by three, as research at the time suggested families spent about one-third of their after-tax income on food.

Critics and financial experts often point out that while the cost of food has decreased as a percentage of the average budget, the costs of housing, healthcare, and education have skyrocketed. This historical calculation remains the backbone of US poverty metrics, creating a significant gap between official figures and the actual “cost of living.”

The Supplemental Poverty Measure (SPM) and Modern Financial Realities

Recognizing the limitations of the official poverty measure, the US government introduced the Supplemental Poverty Measure (SPM) in 2011. This metric provides a more nuanced look at a household’s financial health by incorporating modern economic variables that the official thresholds ignore.

Incorporating Regional Cost of Living

One of the most significant flaws in the official poverty measure is its failure to account for geographic differences in the cost of living. A salary of $30,000 might provide a modest but stable life in some Midwestern towns, but it represents extreme financial distress in major metropolitan hubs like New York City or Seattle. The SPM adjusts for these regional differences, particularly in housing costs, providing a more accurate picture of how much “money” is actually required to survive in different parts of the country.

Accounting for Non-Cash Benefits and Necessary Expenses

Unlike the official measure, which only looks at gross before-tax cash income, the SPM accounts for “near-money” benefits. This includes the financial value of SNAP benefits, housing subsidies, and the Earned Income Tax Credit (EITC). Conversely, it also subtracts necessary expenses that reduce a family’s disposable income, such as federal and state income taxes, childcare expenses, and out-of-pocket medical costs.

From an investing and personal finance standpoint, the SPM is a much better indicator of “discretionary income” potential within a population. It reveals how government interventions effectively lift millions out of poverty, even if their gross income remains below the official threshold.

The Impact of the “Benefits Cliff”

In the study of business finance and labor economics, the “benefits cliff” is a critical phenomenon related to poverty measures. This occurs when a small increase in income—perhaps through a raise or a side hustle—results in a total loss of government assistance that exceeded the value of the raise. For many families living near the poverty line, earning more money can actually lead to a worse financial position, creating a cycle of poverty that is difficult to break without strategic financial planning.

The Gap Between “Official Poverty” and Financial Self-Sufficiency

Even with the SPM, there is a growing consensus among financial experts that the “poverty line” is significantly lower than what is required for true financial stability. This has led to the development of the “Self-Sufficiency Standard.”

Defining Economic Stability vs. Survival

Official poverty measures are designed to identify “destitution”—the point at which a family cannot meet basic survival needs. However, in modern personal finance, “stability” requires more than just survival. It requires the ability to save for emergencies, invest in retirement, and maintain insurance. The Self-Sufficiency Standard often finds that families need two to three times the official poverty level income just to meet their basic needs without public or private assistance.

The Rise of the “ALICE” Population

United Way and other financial researchers use the acronym ALICE: Asset Limited, Income Constrained, Employed. This demographic represents the “working poor”—those who earn above the federal poverty level but less than what is needed to survive in the current economy. These individuals often have no savings and are one car repair or medical bill away from financial ruin. From a market perspective, this group represents a significant portion of the workforce that remains financially vulnerable despite being fully employed.

Inflation and the Eroding Value of Income

Inflation acts as a silent tax on those near the poverty line. While poverty guidelines are adjusted annually for inflation using the Consumer Price Index (CPI), these adjustments often lag behind the real-world price increases of essential goods like rent and energy. For those on fixed incomes or low-wage hourly roles, the “real” value of their money often diminishes faster than federal thresholds can keep pace with, leading to a perpetual state of financial catch-up.

Financial Tools and Strategies for Moving Beyond the Threshold

For individuals and families hovering near the poverty line, financial management is not just about budgeting; it is about strategic navigation of resources. Moving from poverty to financial security requires a multi-faceted approach to income and asset building.

Leveraging Tax Credits as Capital

For many low-income households, the annual tax refund—driven by the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC)—is the largest single “infusion of capital” they receive all year. Financial advisors specializing in low-income populations emphasize the importance of using these funds not just for consumption, but as a “seed” for an emergency fund or to pay off high-interest debt, which is a major barrier to wealth accumulation.

The Importance of Financial Literacy and Micro-Investing

Access to financial tools is often a barrier for those in poverty. “Underbanked” individuals often rely on predatory check-cashing services or payday loans that strip away their wealth. Promoting financial literacy—understanding credit scores, interest rates, and the power of compound interest—is a vital tool for economic mobility. Furthermore, the rise of fintech apps that allow for micro-investing and fractional shares has lowered the barrier to entry for the stock market, allowing those with limited income to begin building an asset base, however small.

Diversifying Income Through Side Hustles

In the modern digital economy, the ability to generate “online income” or engage in “side hustles” has become a lifeline for those near the poverty line. Whether it is freelance work, the gig economy, or selling goods through digital marketplaces, diversifying income streams helps mitigate the risk of the “benefits cliff” and provides a buffer against the volatility of low-wage employment.

The Macroeconomic Outlook: Poverty and National Wealth

Ultimately, the definition of poverty in the US is a reflection of the nation’s economic priorities. While the US remains one of the wealthiest countries in the world, the persistence of a large population living at or near the poverty threshold indicates a disconnect in the distribution of economic growth.

From a business finance perspective, poverty represents “lost human capital.” When a significant portion of the population is focused solely on survival, their ability to innovate, consume, and invest is suppressed, which ultimately slows the growth of the entire economy. Understanding what is considered poverty is the first step in addressing the systemic financial barriers that prevent millions of Americans from participating fully in the national economy.

As we move forward, the conversation around poverty in the US will likely shift from “minimum survival” to “financial inclusion.” Ensuring that more households have the tools to build assets, protect their income from inflation, and navigate the complexities of modern finance is essential for the long-term economic vitality of the country. For now, the poverty line remains a stark, mathematical reminder of the work that remains to be done in achieving broad-based financial prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.