In the complex world of personal finance, understanding the terms and conditions associated with any form of borrowing is paramount. Among the most crucial concepts you’ll encounter is the Annual Percentage Rate, commonly abbreviated as APR. While it might seem like just another number, the APR is your key to unlocking the true cost of a loan or credit card, allowing you to make informed financial decisions. This article will delve into what an APR rate is, how it’s calculated, what it encompasses, and why it’s an indispensable tool in your financial toolkit, especially when navigating the landscape of personal finance, investing, and even business finance.

Deciphering the APR: More Than Just an Interest Rate

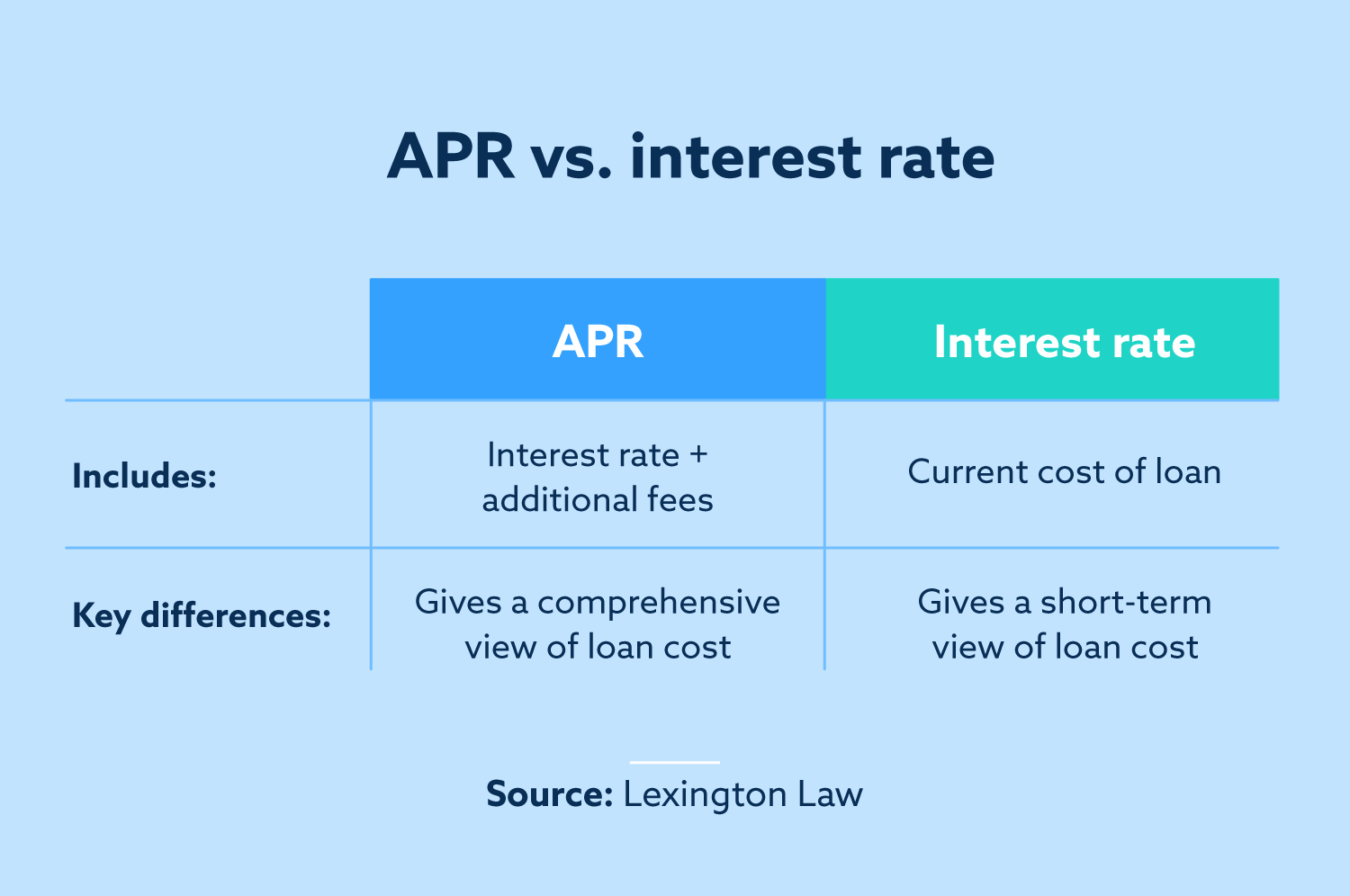

At its core, an APR represents the annual cost of borrowing money. However, it’s a more comprehensive figure than a simple interest rate. Think of it as the “all-in” price of a loan. While the interest rate tells you how much you’ll pay the lender for the privilege of using their money, the APR also factors in other charges and fees associated with obtaining and maintaining the loan. This holistic approach makes it a much more accurate reflection of your total financial obligation.

Why APR Matters: Unveiling the Hidden Costs

The distinction between an interest rate and an APR is vital because many loans and credit products come with various fees. These can include:

- Origination fees: Charged by lenders to process a new loan application.

- Discount points: Fees paid to reduce the interest rate on a mortgage.

- Mortgage insurance premiums: Required for certain home loans.

- Annual fees: Common on credit cards, charged for the privilege of having the card.

- Service fees: For maintaining the loan or account.

Without considering these additional costs, you might be misled into believing a loan with a seemingly lower interest rate is more affordable. The APR accounts for these expenses, rolling them into a single, annualized percentage that provides a standardized way to compare different loan offers.

The APR vs. Interest Rate: A Crucial Distinction

Let’s illustrate with an example. Imagine you’re looking at two personal loans:

- Loan A: Offers a 5% interest rate and no fees.

- Loan B: Offers a 4.5% interest rate but charges a 2% origination fee.

On the surface, Loan B appears cheaper due to its lower interest rate. However, when you factor in the origination fee, the APR for Loan B will likely be higher than its stated interest rate, potentially making Loan A the more cost-effective option overall. The APR calculation will amortize that 2% fee over the life of the loan, revealing the true annual cost.

How APR is Calculated: Unpacking the Formula

The precise calculation of APR can vary slightly depending on the type of credit product and regulatory guidelines. However, the general principle involves annualizing the interest and fees associated with the loan.

For Fixed-Rate Loans (like Mortgages or Car Loans):

The basic formula aims to find the interest rate that equates the present value of all scheduled payments (including principal and interest) to the net amount borrowed (principal minus upfront fees). In simpler terms, it’s the interest rate that makes the loan’s total cost, considering fees, consistent with the amount you actually receive and repay over the loan’s term.

The calculation typically involves:

- Determining the total finance charge: This includes all interest payments plus any upfront fees.

- Dividing the total finance charge by the net amount financed: This gives you the total cost of credit relative to the amount borrowed.

- Annualizing the result: This figure is then converted into an annual percentage.

For example, if you borrow $10,000 and pay $500 in interest and $100 in origination fees over one year, your total cost is $600. Your APR would be $600 / $10,000 = 6%. If the loan term is longer, the fees are spread out, leading to a potentially lower APR than if all fees were concentrated upfront.

For Credit Cards (Revolving Credit):

Credit card APRs are typically stated as a “periodic rate,” which is then multiplied by the number of periods in a year (usually 12 for monthly billing cycles) to arrive at the Annual Percentage Rate.

- Periodic Rate = Annual Interest Rate / Number of Billing Cycles per Year

So, if a credit card has an APR of 18%, its monthly periodic rate would be 18% / 12 = 1.5%. This 1.5% is applied to your outstanding balance each month if you don’t pay your balance in full. Credit card APRs can also be variable, meaning they can change based on economic indicators like the prime rate.

Types of APR: Not All APRs Are Created Equal

It’s important to recognize that different types of credit products might have slightly different APR structures and disclosures.

1. Purchase APR:

This is the most common APR associated with credit cards. It applies to purchases you make with the card. Many credit cards offer introductory 0% APR periods, which can be incredibly beneficial for large purchases, allowing you to pay them off over time without incurring interest.

2. Balance Transfer APR:

This APR applies when you transfer a balance from one credit card to another. Often, balance transfer offers come with a low or 0% introductory APR for a specific period. However, it’s crucial to understand what the APR will be after the introductory period expires, as it can significantly impact the cost of carrying that debt.

3. Cash Advance APR:

Taking cash out using your credit card typically comes with a much higher APR than the purchase APR, and interest often starts accruing immediately with no grace period.

4. Penalty APR:

This is a punitive rate that can be triggered if you miss payments or violate the terms of your credit agreement. Penalty APRs are usually very high and can significantly increase the cost of your debt.

5. Mortgage APR:

When obtaining a mortgage, the APR includes not only the interest rate but also other loan costs such as private mortgage insurance (PMI), origination fees, and discount points. This provides a more accurate picture of your total housing cost.

6. Auto Loan APR:

Similar to mortgages, auto loan APRs incorporate the interest rate along with lender fees, such as origination fees or dealer fees, to give you a complete understanding of the cost of financing your vehicle.

The Importance of APR in Financial Decision-Making

Understanding and comparing APRs is fundamental to making sound financial choices, whether you’re a student managing a credit card, a homeowner financing a property, or a business owner seeking capital.

Personal Finance and Budgeting

For individuals, a low APR on a credit card can make it easier to manage expenses and avoid accumulating high-interest debt. When comparing different credit cards for everyday spending or planned purchases, always prioritize the one with the lowest APR, especially if you anticipate carrying a balance. This can save you hundreds, if not thousands, of dollars over time. Similarly, when considering personal loans for debt consolidation or significant purchases, comparing APRs is crucial for selecting the most affordable option.

Investing and Side Hustles

While APR primarily relates to borrowing, its principles can indirectly influence investment and side hustle decisions. For example, if you’re considering taking out a loan to fund a business venture or invest in a specific opportunity, the APR of that loan will directly impact the profitability of your endeavor. A high APR can eat into your returns, making the investment less attractive. Understanding the cost of capital is as important as understanding potential returns. For online income opportunities or side hustles that might require upfront investment, comparing the cost of financing against the projected income is a critical step.

Business Finance and Growth

For businesses, the APR on loans, lines of credit, or other forms of financing is a critical factor in their financial planning and growth strategy. A lower APR means lower interest expenses, freeing up capital for reinvestment in the business, expansion, or research and development. When seeking business loans, comparing the APRs from different lenders is essential to securing the most favorable terms. This directly impacts the business’s profitability and its ability to compete.

Smart Strategies for Managing APR

Navigating the world of APRs requires a strategic approach:

- Shop Around: Never accept the first loan or credit card offer you receive. Compare APRs from multiple lenders and issuers.

- Read the Fine Print: Always carefully review all terms and conditions, especially regarding fees, grace periods, and how the APR is calculated.

- Understand Introductory Offers: Take advantage of low or 0% introductory APRs, but make sure you have a plan to pay off the balance before the higher standard APR kicks in.

- Prioritize Debt Reduction: If you have high-interest debt, focus on paying it down as quickly as possible. The higher the APR, the more interest you accrue.

- Monitor Your Credit Score: A good credit score often qualifies you for lower APRs.

In conclusion, the Annual Percentage Rate is a powerful tool that provides a clear and comprehensive understanding of the true cost of borrowing. By understanding what it is, how it’s calculated, and its implications across various financial scenarios, you can make more informed decisions, save money, and build a stronger financial future. Whether you’re managing personal finances, exploring online income streams, or steering a business, mastering the concept of APR is a fundamental step towards financial literacy and success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.