In the intricate landscape of modern finance, certain numerical identifiers serve as crucial lynchpins, ensuring the smooth and accurate flow of money. Among these, the ABA Routing Number, often simply called a routing number, stands out as a fundamental component of the U.S. banking system. For millions of Chase Bank customers, understanding their specific Chase ABA number is not merely a technical detail but a prerequisite for engaging in a wide array of essential financial transactions, from receiving paychecks via direct deposit to paying bills automatically and initiating wire transfers. This comprehensive guide will demystify the Chase ABA number, explain its profound importance, and provide clear, actionable methods for locating the correct number for your financial needs.

Demystifying the ABA Routing Number: A Core Financial Identifier

At its heart, an ABA routing number is a nine-digit code that identifies the specific financial institution participating in a transaction. It acts much like a postal code for banks, directing funds to the correct bank out of thousands across the United States. Without this unique identifier, the vast network of interbank transfers would grind to a halt, making routine financial activities impossible.

What Exactly is an ABA Routing Number?

The term “ABA” originates from the American Bankers Association, which established this system in 1910 to process paper checks efficiently. Over time, its role evolved dramatically with the advent of electronic banking. Today, while still used for checks, the ABA routing number is predominantly used for electronic funds transfers (EFTs).

Each of the nine digits within an ABA routing number carries specific information, though customers typically don’t need to know the breakdown. Broadly, the first four digits often denote the Federal Reserve routing symbol, identifying the Federal Reserve Bank that serves the financial institution. The next four digits identify the bank itself, and the final digit is a checksum digit used for error detection, ensuring the number is valid.

It’s important to clarify that while “ABA routing number” is the formal name, it’s often used interchangeably with “routing number” or “routing transit number (RTN).” For most everyday electronic transactions like direct deposits and ACH payments, this is the number you need.

The Critical Role in Modern Finance

The ABA routing number is the backbone of numerous financial operations that individuals and businesses rely on daily. Its importance cannot be overstated, as virtually any movement of money between different U.S. financial institutions requires it.

- Facilitating Electronic Funds Transfers (EFTs): This broad category includes almost all digital money movements, from sending money to a friend’s account at another bank to transferring funds between your own accounts at different institutions.

- Direct Deposits: Whether it’s your salary, government benefits (like Social Security), tax refunds, or pension payments, direct deposit relies on your bank’s routing number to ensure funds land in your correct account at Chase. Employers and benefit providers require this number to initiate these transfers.

- Automated Clearing House (ACH) Transactions: The ACH network is a batch-processing system that facilitates a high volume of electronic credit and debit transactions. This includes automatic bill payments (e.g., mortgages, utilities, insurance premiums), recurring subscriptions, and direct debit payments. Without the correct routing number, these automated payments would fail, potentially leading to late fees or service interruptions.

- Wire Transfers (Domestic): While international wire transfers typically use SWIFT/BIC codes, domestic wire transfers within the U.S. utilize ABA routing numbers. These are often used for urgent, high-value transfers, and accuracy is paramount to avoid delays or misdirection of substantial funds.

- Check Processing: Even in the digital age, physical checks are still used. The routing number printed on a check directs the check to the correct bank for processing and clearing, enabling the funds to be debited from the payer’s account and credited to the payee’s.

Understanding these applications underscores why knowing and correctly using your Chase ABA number is fundamental to seamless financial management.

Finding Your Chase ABA Number: A Comprehensive Guide

Given the critical importance of the ABA routing number, Chase Bank provides multiple convenient and reliable ways for its customers to locate this essential piece of information. It’s always best to obtain the number directly from Chase or a verified source to ensure accuracy.

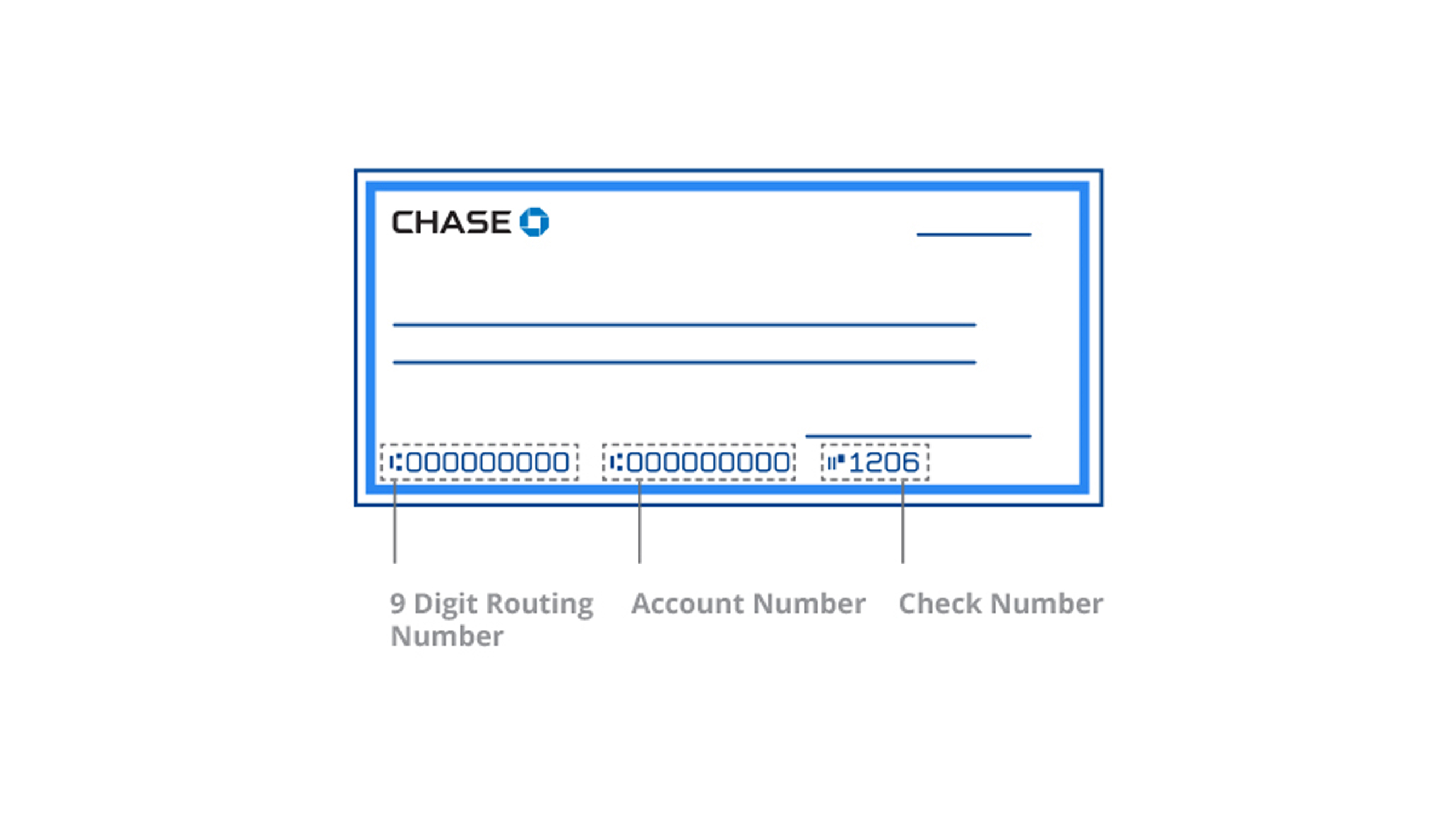

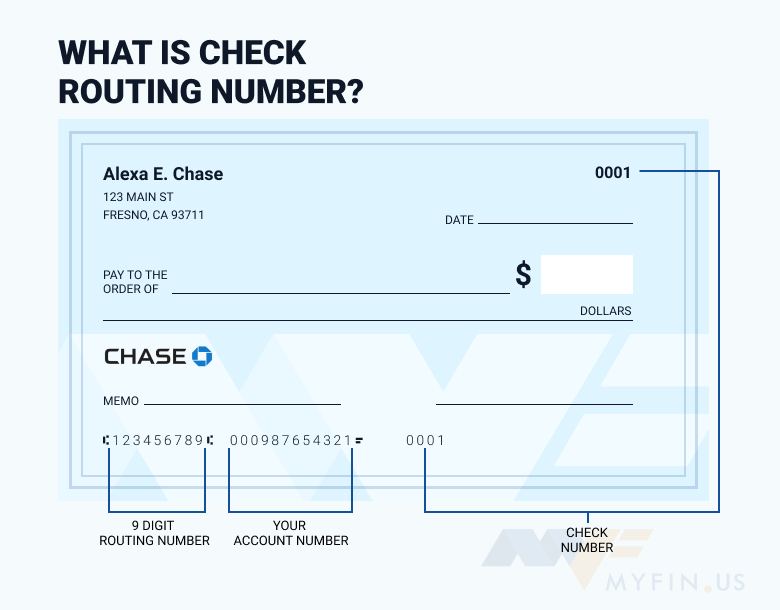

On Your Checks: The Easiest Method

For most checking accounts, the quickest way to find your routing number is right on your physical checks. Look at the bottom of a check. You will typically see three sets of numbers, separated by special characters.

The routing number is almost always the first set of nine digits on the far left. Immediately following it will be your account number, and then typically the check number. Always double-check to ensure you’re looking at the correct sequence, but this is a widely recognized standard.

Through Your Chase Online Banking Portal

Chase’s robust online banking platform is an excellent and secure resource for accessing your account details, including your routing number.

- Log In: Go to the official Chase website (chase.com) and log in to your account using your username and password.

- Select Your Account: Once logged in, navigate to the specific checking or savings account for which you need the routing number.

- View Account Details: Look for a section or tab labeled “Account Details,” “Customer Service,” or “Routing Number.” For checking accounts, the routing number is often prominently displayed near the account summary. For savings accounts, it might be listed under “Account Services” or similar.

- Confirm: Make a note of the 9-digit number displayed.

This method is particularly reliable as it comes directly from your secure banking portal and ensures you get the number associated with your specific account.

Via the Chase Mobile App

The Chase Mobile App offers a convenient way to access your banking information on the go, mirroring much of the functionality of the online banking portal.

- Open and Log In: Launch the Chase Mobile App on your smartphone or tablet and log in using your credentials or biometric authentication.

- Select Account: Tap on the specific checking or savings account you need the routing number for.

- Find Account Details: Look for an “Account Details,” “Show Details,” or “Routing Numbers” option, which might be found by tapping on the account itself or an information icon (like a small “i”).

- Retrieve Number: The routing number will be displayed alongside other account information.

The mobile app provides instant access and is ideal when you’re away from a computer.

Contacting Chase Customer Service

If you’re unable to find the routing number through online channels or on your checks, or if you have specific questions about its use for a particular transaction, contacting Chase customer service is a reliable option.

- Phone: Call the customer service number listed on the back of your debit card or on the official Chase website. Be prepared to verify your identity with personal information.

- Branch Visit: Visiting a local Chase branch allows you to speak directly with a banker who can provide the correct routing number for your account and answer any related questions. This is particularly useful for complex or unique transactions.

Utilizing Chase Bank Statements

Your monthly or quarterly bank statements, whether paper or electronic (e-statements), also contain your account’s routing number.

- Access Statements: Log into online banking or the mobile app to view your e-statements, or locate a physical statement.

- Locate Number: The routing number is typically printed prominently near your account number and other account details, often in the top section of the statement.

Always handle bank statements securely, as they contain sensitive financial information.

Navigating Multiple Chase Routing Numbers

One common point of confusion for customers is the existence of multiple routing numbers for a single bank, especially a large institution like Chase. It’s crucial to understand why this occurs and how to select the correct number for your specific transaction. Using the wrong routing number can lead to significant delays, rejected transactions, or even misdirected funds.

Why Different Routing Numbers Exist for Chase

The primary reasons for Chase having different routing numbers stem from its expansive operations and the varied nature of financial transactions.

- Geographical Variations: Historically, banks operated regionally, and routing numbers were assigned based on the Federal Reserve district where the bank was chartered or where the account was opened. Even though banking is now national, some of these legacy geographical distinctions persist. Chase, being a national bank with branches across many states, often has different routing numbers assigned to different regions or states. For example, a checking account opened in New York might have a different routing number than one opened in California, even within Chase.

- Purpose-Specific Numbers: Beyond geographical differences, Chase may use distinct routing numbers for different types of transactions or accounts.

- ACH (Automated Clearing House) Transactions: These are for routine electronic transfers like direct deposits and automatic bill payments. Most of the time, the routing number found on your checks or online banking is the correct ACH routing number.

- Wire Transfers: Domestic wire transfers, especially for higher value or time-sensitive transactions, sometimes require a specific wire transfer routing number, which might be different from the standard ACH number. This is because wire transfers typically process individually and in real-time, unlike ACH transactions which are batched.

- Savings vs. Checking Accounts: While often the same, there can sometimes be different routing numbers for checking and savings accounts, particularly if they are managed under different internal systems or geographical divisions.

- Impact of Mergers and Acquisitions: Over its long history, Chase (JPMorgan Chase & Co.) has grown through numerous mergers and acquisitions. When Chase acquires another bank, the acquired bank’s routing numbers might initially remain in use for some time or be phased out, leading to a period where multiple numbers are valid depending on when and where an account was opened.

Identifying the Correct Number for Your Transaction

The golden rule for routing numbers is: always verify the correct number for the specific transaction you are making and the account you are using.

- For Direct Deposit/ACH Payments: Generally, the routing number found on your checks or through your online banking for your checking account is the correct one. If you’re setting up direct deposit for a savings account, ensure you get the number specifically for that savings account, usually found in your online banking portal.

- For Domestic Wire Transfers: This is where extra caution is needed. While some banks use the same number for ACH and wires, many large banks like Chase have a dedicated wire transfer routing number. It’s imperative to confirm this directly with Chase (via online banking, customer service, or a branch) before initiating a wire transfer. Using an ACH routing number for a wire can cause significant delays or even send the funds to an intermediary bank that then needs to reroute them, incurring additional fees.

- Chase’s Official Routing Number Lookup Tools: Chase often provides dedicated pages on its website or sections within its online banking/mobile app that allow you to look up the correct routing number based on your state or the specific type of transaction. Always prioritize these official sources.

Never assume a routing number you found online on an unofficial site or heard from an unverified source is correct. A small error can lead to substantial financial headaches.

Security and Best Practices for Handling Your ABA Number

While the ABA routing number is a public identifier for a financial institution, its use in conjunction with your personal account number makes it a sensitive piece of information. Handling it with care and understanding its limitations are crucial for financial security.

Safeguarding Your Financial Information

The routing number itself isn’t a direct security risk, as it merely identifies your bank. However, when combined with your account number, it can be used to initiate transactions like ACH debits.

- Phishing Scams and Fraudulent Requests: Be extremely wary of unsolicited emails, texts, or phone calls asking for your routing and account numbers. Legitimate institutions rarely request this information via unsecure channels. Always verify the sender’s identity and the legitimacy of the request.

- Only Share with Trusted Parties: Only provide your routing and account numbers to legitimate businesses, employers, or government agencies for valid financial purposes (e.g., setting up direct deposit, paying bills, filing taxes).

- Secure Online Platforms: When entering your banking details online, ensure the website is secure (look for “https://” in the URL and a padlock icon).

Common Mistakes to Avoid

Preventing errors is key to seamless financial operations. Being aware of common pitfalls can save you time, stress, and potential financial losses.

- Confusing ABA Numbers with Account Numbers: This is perhaps the most frequent mistake. The routing number identifies the bank, while the account number identifies your specific account within that bank. Both are required for most transactions, and mixing them up will invariably lead to rejected payments or misdirected funds.

- Using an Old or Incorrect Routing Number: If you’ve changed banks, closed an account, or if Chase has updated its routing numbers (which happens occasionally), ensure you are using the most current and correct number for your active account. Always re-verify if you’re unsure.

- Mistaking Domestic Routing Numbers for International SWIFT/BIC Codes: A U.S. ABA routing number is only for domestic transactions within the United States. It will not work for international money transfers.

Understanding International Transfers: ABA vs. SWIFT/BIC

For sending or receiving money internationally, a different set of identifiers is used.

- SWIFT/BIC Codes: The Society for Worldwide Interbank Financial Telecommunication (SWIFT) assigns Bank Identifier Codes (BICs) to financial and non-financial institutions worldwide. These codes, typically 8 or 11 characters long, identify a bank in a global network. When you send or receive an international wire transfer, you will need the recipient’s bank’s SWIFT/BIC code, not their ABA routing number.

- Chase’s SWIFT Code: For international transfers to a Chase account, you would typically use Chase’s primary SWIFT code, which is usually CHASUS33. However, it’s always best to confirm the exact SWIFT code with Chase or the sender, as variations can exist for different types of international transactions or specific Chase entities.

Understanding the clear distinction between ABA routing numbers for domestic transfers and SWIFT/BIC codes for international transfers is crucial for successful cross-border financial activity.

In conclusion, the ABA routing number for Chase is a vital numerical identifier that underpins almost all domestic financial transactions. By understanding its purpose, knowing where to locate it reliably, and exercising due diligence in its use, Chase customers can ensure their financial operations proceed smoothly, securely, and without costly errors. Always verify, always confirm, and always prioritize official sources to safeguard your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.