In the intricate dance of global finance, few economic indicators hold as much sway over the everyday financial lives of individuals and businesses as the prime rate. Often mentioned in passing on financial news channels or whispered among loan officers, its movements can dictate the cost of borrowing, the profitability of savings, and the strategic decisions of companies both large and small. While its exact value fluctuates, understanding its underlying mechanisms, its impact, and how to navigate its shifts is crucial for anyone keen on astute financial management.

This article will demystify the prime rate, explaining its origins, its profound influence across various financial products, the forces that drive its changes, and practical strategies for borrowers, savers, and investors alike. As a cornerstone of the money market, the prime rate is far more than just a number; it’s a barometer of economic health and a key determinant of financial opportunity and challenge.

Understanding the Prime Rate: The Benchmark of Lending

The prime rate is, at its core, the interest rate that commercial banks charge their most creditworthy corporate customers. It serves as a benchmark for a vast array of other lending products, making it a critical figure for anyone tracking the cost of money.

Defining the Prime Rate: A Bank’s Preferred Rate

Historically, the prime rate was seen as the lowest rate at which a bank would lend money. While highly creditworthy borrowers might negotiate rates below prime, for the majority, the prime rate represents a foundational floor from which other rates are derived. Each commercial bank in the United States sets its own prime rate. However, for all practical purposes, this rate moves in near-unison across the industry. Why? Because it is overwhelmingly influenced by a single, powerful entity: the U.S. Federal Reserve.

Typically, the prime rate is calculated by adding a fixed spread—historically 300 basis points, or 3 percentage points—to the target federal funds rate set by the Federal Open Market Committee (FOMC). So, if the federal funds rate target is 2%, the prime rate will generally be 5%. This predictable relationship makes the prime rate a direct reflection of the Fed’s monetary policy stance.

The Federal Funds Rate Connection: The Fed’s Invisible Hand

To truly grasp the prime rate, one must first understand the federal funds rate. This isn’t a rate you or I can directly access. Instead, it’s the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight, on an uncollateralized basis. The FOMC, the monetary policy-making body of the Federal Reserve System, sets a target range for this rate.

When the FOMC decides to raise the federal funds rate, it signals a tightening of monetary policy, making it more expensive for banks to borrow from one another. This increased cost trickles down. Banks, facing higher costs themselves, subsequently raise their prime rate to maintain profitability and manage their cost of funds. Conversely, when the Fed lowers the federal funds rate, it eases monetary conditions, making interbank borrowing cheaper, and banks typically respond by lowering their prime rate. This symbiotic relationship ensures that the prime rate directly translates the Fed’s broader economic strategy into tangible lending costs across the financial system.

Why it Matters to You: A Sneak Peek

Even if you don’t run a Fortune 500 company, the prime rate’s movements are profoundly relevant. It directly or indirectly impacts the interest rates on credit cards, home equity lines of credit (HELOCs), certain mortgages, small business loans, and even some student loans. Understanding its trajectory can empower you to make more informed decisions about borrowing, saving, and investing, positioning you to capitalize on opportunities or mitigate potential risks.

The Prime Rate’s Ripple Effect on Your Personal & Business Finances

The prime rate acts as a foundational benchmark, influencing a vast array of financial products that are crucial to both individual consumers and the broader business landscape. Its shifts don’t just change a number on a spreadsheet; they alter the cost of daily living and the viability of strategic investments.

Variable-Rate Loans and Credit Cards: Direct Exposure

For many consumers, the most immediate and direct impact of a changing prime rate is felt through variable-rate financial products.

- Credit Card APRs: The vast majority of credit cards have variable Annual Percentage Rates (APRs) that are directly tied to the prime rate. Your cardholder agreement will typically state your APR as “Prime Rate + X%.” This means that when the prime rate increases, so does the interest you pay on any outstanding credit card balance. Over time, even small increases can lead to significantly higher minimum payments and a prolonged debt repayment period.

- Home Equity Lines of Credit (HELOCs): HELOCs are popular tools for homeowners to access the equity in their homes. Almost universally, HELOCs feature variable interest rates, often quoted as “Prime Rate + X%.” A rising prime rate translates directly into higher monthly payments for HELOC users, potentially straining household budgets. Conversely, a falling prime rate offers relief, reducing monthly outlays.

- Adjustable-Rate Mortgages (ARMs): While less common than fixed-rate mortgages, ARMs also tie their interest rate adjustments to a benchmark, which is often the prime rate (though other indexes like SOFR or LIBOR, historically, were also used). After an initial fixed-rate period (e.g., 5/1 ARM), the interest rate on an ARM adjusts periodically, meaning changes in the prime rate can lead to significant swings in monthly mortgage payments.

Business Loans and Lines of Credit: Capital Cost & Growth

For businesses, especially small and medium-sized enterprises (SMEs), the prime rate is a critical factor in managing operational costs and funding growth.

- Small Business Loans: Many traditional bank loans for small businesses, particularly revolving lines of credit or variable-rate term loans, are priced based on the prime rate. An increase in the prime rate directly raises the cost of borrowing for working capital, equipment purchases, or inventory financing. This can impact a company’s profitability and cash flow.

- Corporate Lines of Credit: Larger corporations also utilize lines of credit linked to the prime rate. While they often have more sophisticated financing options, the prime rate still influences their short-term borrowing costs for liquidity management and temporary financing needs.

- Investment Decisions: For businesses contemplating expansion, new equipment, or research and development, the cost of financing is paramount. A higher prime rate makes borrowing more expensive, potentially making some projects less financially viable and leading companies to defer or cancel investment plans, which can slow economic growth.

Mortgages and Auto Loans (Indirect Impact): Broader Market Influence

While fixed-rate mortgages and most auto loans aren’t directly indexed to the prime rate, its movements profoundly influence the broader lending market and, by extension, these products.

- Fixed-Rate Mortgages: The rates for fixed-rate mortgages are more closely tied to the yields on long-term U.S. Treasury bonds. However, the Federal Reserve’s actions, which directly impact the prime rate, also affect the overall economic environment, inflation expectations, and investor appetite for bonds. When the Fed raises rates, it typically signals a belief in a stronger economy or a need to combat inflation, which can push Treasury yields higher, thus increasing fixed mortgage rates.

- Auto Loans: Similarly, auto loan rates are influenced by the overall interest rate environment. Lenders’ cost of funds, which is indirectly tied to the prime rate and the federal funds rate, dictates the rates they can offer to consumers. While less volatile than credit card rates, auto loan rates will generally trend upwards or downwards in line with broader interest rate movements.

In essence, the prime rate serves as a barometer that reflects the prevailing cost of money in the economy. Its shifts create a ripple effect, impacting everything from a homeowner’s monthly budget to a small business’s ability to expand, making it a pivotal figure in personal and corporate finance.

The Federal Reserve’s Mandate and Prime Rate Movements

The Federal Reserve stands as the central bank of the United States, possessing an immense influence over the prime rate through its monetary policy decisions. Understanding its mandate and tools is key to predicting potential shifts in borrowing costs.

The Dual Mandate: Inflation and Employment at the Forefront

The Federal Reserve operates under a “dual mandate” bestowed upon it by Congress: to promote maximum employment and stable prices (low and stable inflation). These two objectives often require a delicate balancing act.

- Maximum Employment: The Fed aims for an economy where everyone who wants a job can find one, and unemployment rates are low.

- Stable Prices: This refers to keeping inflation in check, generally targeting a 2% annual inflation rate. High inflation erodes purchasing power and creates economic uncertainty, while deflation (falling prices) can stifle demand and lead to recessions.

When the economy is strong and employment is high, but inflation starts to accelerate beyond the 2% target, the Fed typically steps in to cool down the economy by raising interest rates. Conversely, during periods of economic weakness, high unemployment, or low inflation, the Fed tends to lower rates to stimulate borrowing, spending, and investment.

Tools of Monetary Policy: Steering the Economy

The primary tool the Fed uses to influence the prime rate is the federal funds rate target range. By adjusting this target, the Fed can make it more or less expensive for banks to lend to each other overnight, directly impacting the cost of funds for commercial banks, which then translates into their prime rate.

Beyond the federal funds rate, the Fed also employs other tools:

- Quantitative Easing (QE) and Quantitative Tightening (QT): QE involves the Fed buying large quantities of government bonds and other securities to inject liquidity into the financial system and lower long-term interest rates. QT, the reverse, involves reducing its balance sheet, which can put upward pressure on long-term rates. While these tools primarily affect longer-term rates, they contribute to the overall economic environment that influences the Fed’s stance on the federal funds rate.

- Discount Rate: This is the interest rate at which commercial banks can borrow directly from the Federal Reserve. While less frequently used than the federal funds rate, it acts as a backstop and a signal of the Fed’s policy stance.

- Reserve Requirements: These are the amounts of funds that banks must hold in reserve against deposits. Changes to reserve requirements can affect the amount of money banks have available to lend, though this tool is now rarely used.

Reading Between the Lines: FOMC Statements and Economic Data

The FOMC meets eight times a year (roughly every six weeks) to assess economic conditions and make monetary policy decisions. The statements released after these meetings are scrutinized by economists, investors, and businesses worldwide. They provide crucial insights into the Fed’s outlook on inflation, employment, and future interest rate policy.

Furthermore, the Fed constantly monitors a wide array of economic data to inform its decisions:

- Inflation data: Consumer Price Index (CPI), Producer Price Index (PPI), and Personal Consumption Expenditures (PCE) price index (the Fed’s preferred measure).

- Employment data: Non-farm payrolls, unemployment rate, wage growth.

- GDP growth: Gross Domestic Product, a broad measure of economic activity.

- Consumer spending and confidence reports.

- Manufacturing and services sector surveys.

By analyzing these indicators, the Fed gauges the health of the economy and determines whether to tighten (raise rates) or ease (lower rates) monetary policy. Understanding these signals is essential for anyone trying to anticipate prime rate movements.

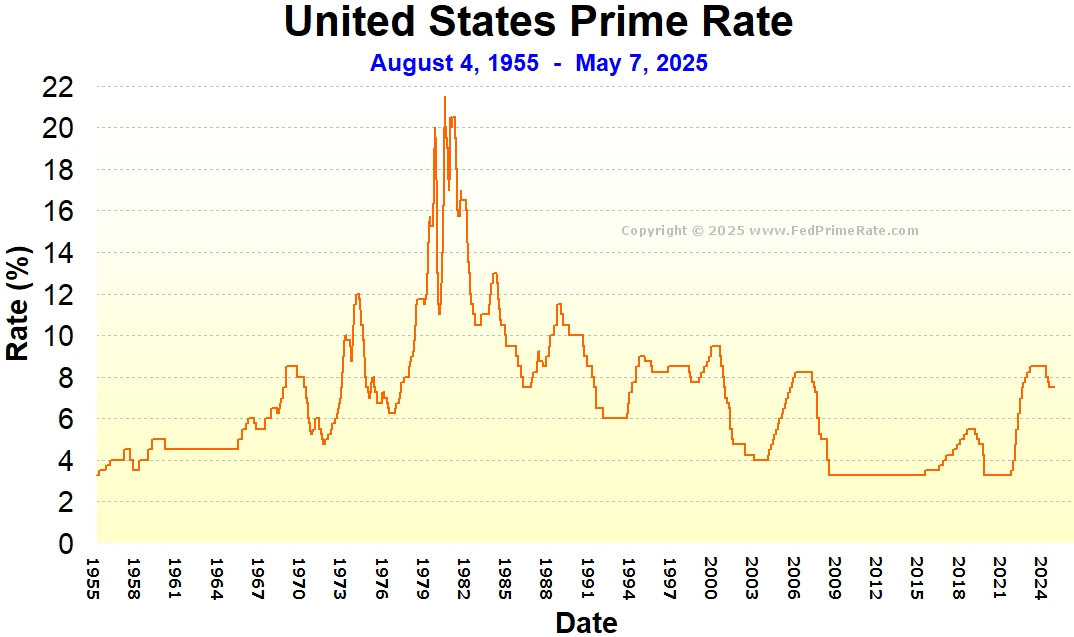

Historical Context of Prime Rate Shifts

The prime rate has seen significant volatility throughout history. In the late 1970s and early 1980s, under then-Fed Chair Paul Volcker, the prime rate soared to unprecedented levels (peaking at 21.5% in 1980-81) to combat runaway inflation. Conversely, during the 2008 financial crisis and the COVID-19 pandemic, the prime rate plummeted to historic lows (3.25%) as the Fed aggressively cut rates to stimulate the economy. These historical swings underscore the Fed’s power and the cyclical nature of interest rate environments, each bringing its own set of challenges and opportunities for financial planning.

Navigating the Current and Future Prime Rate Landscape

Keeping abreast of the prime rate isn’t just an academic exercise; it’s a dynamic aspect of sound financial planning. Given that its exact value can change, understanding where to find current information and how to strategize around its likely future trajectory is paramount.

Current Prime Rate Status: Where to Find the Latest Data

As of the current date, I cannot provide a real-time prime rate, as this information changes. However, staying informed is straightforward. You can typically find the most up-to-date prime rate by:

- Checking Major Bank Websites: Large commercial banks (e.g., JPMorgan Chase, Bank of America, Wells Fargo) prominently display their current prime rate on their websites, often in their interest rate or lending sections. Since banks move in lockstep, checking one major bank is usually sufficient.

- Financial News Outlets: Reputable financial news sources (e.g., The Wall Street Journal, Bloomberg, Reuters, CNBC) regularly report on the prime rate, especially following FOMC meetings or significant economic announcements.

- Federal Reserve Publications: The Federal Reserve Board’s website may also provide information on the current federal funds target rate, from which the prime rate can be easily inferred (add 3.00%).

In recent periods, after a significant cycle of rate hikes by the Federal Reserve aimed at combating inflation, the prime rate reached multi-decade highs. The current financial landscape is often characterized by discussions around whether the Fed will maintain these higher rates, or if and when rate cuts might commence, depending on inflation trends and employment data.

Strategies for Borrowers in a High/Volatile Rate Environment

When the prime rate is high or subject to frequent changes, borrowers need to be proactive and strategic.

- Prioritize High-Interest, Variable-Rate Debt: Focus on paying down credit card balances and HELOCs aggressively. Every extra payment reduces the principal, thereby lessening the impact of rising interest costs.

- Consider Refinancing: If you have a variable-rate loan and expect rates to remain high or rise further, explore refinancing into a fixed-rate loan if possible. This can provide payment stability and predictability. For example, consolidating high-interest credit card debt into a personal loan with a fixed rate might offer significant savings.

- Evaluate Loan Terms Carefully: When taking out new loans, meticulously compare fixed-rate versus variable-rate options. While variable rates might initially seem lower, they carry the risk of future increases.

- Manage Credit Card Usage: If rates are high, minimizing new credit card debt and paying balances in full each month becomes even more critical to avoid accruing significant interest charges.

Implications for Savers and Investors: Opportunities Amidst Change

A rising prime rate isn’t solely a challenge for borrowers; it often presents opportunities for savers and certain investors.

- Higher Yields on Savings Accounts: When interest rates rise, banks tend to offer higher annual percentage yields (APYs) on savings accounts, money market accounts, and Certificates of Deposit (CDs). This is an opportune time to ensure your emergency fund and other short-term savings are earning competitive rates.

- Attractive Bond Market Returns: Bond yields generally move in the same direction as interest rates. For investors, new bond issues or bond funds purchased in a rising rate environment can offer more attractive returns compared to periods of low rates. However, existing bonds with lower fixed rates may see their market value decline as new, higher-yielding bonds become available.

- Equity Market Volatility: Rising rates can sometimes create headwinds for the stock market, particularly for growth stocks or companies that rely heavily on borrowing. Higher borrowing costs can squeeze corporate profits, and higher bond yields make equities relatively less attractive. However, other sectors, such as financials, can sometimes benefit. Investors should review their portfolio allocation and potentially consider sectors that are more resilient to higher interest rates or those that benefit from stronger economic conditions that might accompany rising rates.

Proactive Financial Planning: Your Best Defense

Regardless of the prime rate’s direction, the most effective strategy is always proactive financial planning.

- Maintain an Emergency Fund: A robust emergency fund can shield you from unexpected expenses without resorting to high-interest debt, especially in a rising rate environment.

- Create and Stick to a Budget: Understanding your income and expenses allows you to identify areas for saving or debt repayment, making you less vulnerable to interest rate fluctuations.

- Seek Professional Advice: A financial advisor can provide personalized guidance, helping you understand how prime rate movements specifically impact your unique financial situation and adjust your strategies accordingly.

The prime rate, a seemingly simple number, is a powerful economic force with far-reaching implications. By understanding its mechanics, recognizing its impact on various financial products, and adopting proactive strategies, you can confidently navigate the dynamic landscape of interest rates and make sound financial decisions that align with your long-term goals. Staying informed about the Federal Reserve’s policy decisions and broader economic trends will always be your best defense and offense in managing your money effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.