In the complex ecosystem of global finance, certain entities operate behind the scenes to ensure stability, yet they remain largely invisible to the average consumer. Among the most critical of these players is the reinsurer. Often described as “insurance for insurance companies,” reinsurance is a fundamental pillar of business finance and risk management. Without the safety net provided by reinsurers, the insurance industry as we know it would be unable to handle the financial impact of large-scale disasters, ranging from hurricanes and wildfires to global pandemics and massive cyber-attacks.

For investors, business owners, and financial professionals, understanding the role of a reinsurer is essential. It is not merely a technical niche of the insurance world; it is a vital mechanism for capital management and a unique asset class in the realm of institutional investing. This article explores the mechanics of reinsurance, the various structures it takes, and why it remains one of the most significant forces in the world of money.

Understanding the Concept: Insurance for Insurers

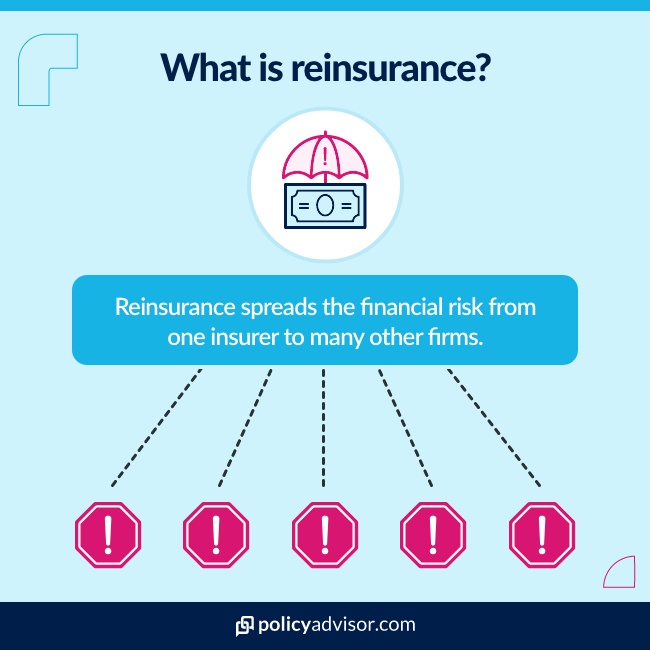

At its core, a reinsurer is a financial institution that provides insurance to other insurance companies (often called “ceding companies” or “primary insurers”). When an insurance company issues thousands of policies to homeowners or businesses, it takes on a massive amount of accumulated risk. If a single catastrophic event were to occur—such as a major earthquake in a densely populated city—the primary insurer might face more claims than its capital reserves can handle.

How Reinsurance Functions

To mitigate this risk, the primary insurer “cedes” a portion of its liabilities to a reinsurer. In exchange for a portion of the premiums collected from policyholders, the reinsurer agrees to pay a share of the losses if certain thresholds are met. This relationship allows the primary insurer to protect its balance sheet and maintain solvency. From a financial perspective, this is a form of risk distribution. By spreading risk across multiple global entities, the financial impact of a disaster is diluted, preventing any single company from collapsing.

The Transfer of Risk

The primary objective of a reinsurer is the effective transfer of risk. In the world of money, risk is a liability that requires capital to back it up. By transferring risk to a reinsurer, a primary insurance company effectively frees up capital. This “capital relief” allows the primary insurer to write more policies and take on more customers without needing to hold massive amounts of cash in reserve. For the reinsurer, the business model relies on the law of large numbers and geographical diversification. Because they take on risks from all over the world, a loss in one region (like a flood in Europe) is often offset by profitable years in another region (like a quiet hurricane season in the Atlantic).

The Mechanics of Reinsurance: Types and Structures

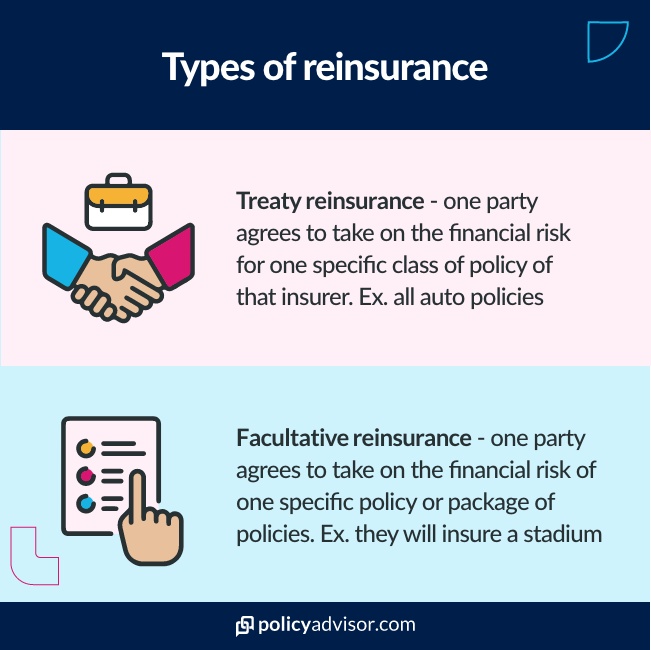

The reinsurance market is not a one-size-fits-all industry. Depending on the needs of the primary insurer and the appetite of the reinsurer, contracts are structured in various ways. These structures are generally categorized into two main types: Treaty and Facultative.

Treaty vs. Facultative Reinsurance

Treaty reinsurance is the most common form. It involves a broad agreement where the reinsurer agrees to cover a specific “book” of business or a whole category of risks for a set period. For example, a primary insurer might have a treaty that covers all its California property insurance policies. The reinsurer is obligated to accept all risks that fall within the treaty’s terms.

Facultative reinsurance, on the other hand, is much more specific. It is negotiated for a single risk or a specific policy. If an insurer is asked to cover a massive, high-value asset—such as a multi-billion dollar bridge or a professional sports stadium—they may seek facultative reinsurance specifically for that one project. This allows the primary insurer to take on high-stakes clients that would otherwise exceed their risk tolerance.

Proportional and Non-Proportional Agreements

Within these categories, the financial split is further defined as either proportional or non-proportional.

- Proportional (Quota Share): In this arrangement, the reinsurer and the primary insurer share a predetermined percentage of both premiums and losses. If the agreement is a 40% quota share, the reinsurer receives 40% of the premiums and pays 40% of every claim.

- Non-Proportional (Excess of Loss): This functions more like a traditional insurance policy with a high deductible. The reinsurer only pays if the losses exceed a certain amount, known as the “retention” or “attachment point.” This is the preferred method for protecting against “black swan” events or catastrophic peaks.

Why Reinsurance Matters: Capital Stability and Market Capacity

From a business finance perspective, the existence of reinsurers is what allows the global economy to function smoothly. Without them, the “capacity” of the insurance market would be severely limited, making it difficult for businesses to obtain the coverage they need to operate.

Managing Solvency and Regulatory Capital

Regulators require insurance companies to maintain a certain level of capital relative to the risks they carry. This is known as the solvency margin. If an insurance company’s risk profile grows too large for its capital base, it must either stop selling policies or find more capital. Reinsurance acts as a “virtual capital” source. By ceding risk, the insurer reduces its required capital levels, allowing it to grow its business efficiently. This is a critical strategic tool for CFOs in the insurance sector to optimize their return on equity.

Smoothing Earnings and Protecting Against Catastrophes

Volatility is the enemy of financial stability. For a publicly-traded insurance company, a single bad quarter due to a natural disaster can send stock prices tumbling. Reinsurance helps “smooth” these earnings. By capping the maximum loss an insurer can sustain from a single event, the reinsurer provides a level of predictability. This financial stability is why global reinsurers like Munich Re, Swiss Re, and Berkshire Hathaway’s General Re are considered cornerstones of the international financial system.

Reinsurance as an Investment Asset Class

For the sophisticated investor, the reinsurance market offers opportunities that are largely uncorrelated with traditional stock and bond markets. This makes it an attractive option for portfolio diversification within the “Money” niche.

Investing in Reinsurance Giants

The most direct way to gain exposure to this sector is by investing in the equity of major reinsurance companies. These firms are massive capital managers. They collect billions in premiums and invest that “float” (the money held between the time premiums are collected and claims are paid) into various financial markets. Large reinsurers are essentially a hybrid between an insurance entity and a massive hedge fund. For example, Warren Buffett’s success with Berkshire Hathaway is largely built on the intelligent use of insurance float provided by his reinsurance subsidiaries.

Insurance-Linked Securities (ILS) and Catastrophe Bonds

In recent decades, the boundary between the insurance market and the capital markets has blurred, leading to the rise of Insurance-Linked Securities (ILS). The most famous of these are “Catastrophe Bonds” (Cat Bonds).

In a Cat Bond deal, an insurer or reinsurer issues a bond to institutional investors. If no catastrophe occurs during the bond’s term, investors receive a high interest rate (yield). However, if a specific disaster occurs (like a Category 4 hurricane hitting Florida), the principal of the bond is “triggered” and used to pay insurance claims. For investors, Cat Bonds offer high yields that don’t fluctuate based on interest rates or tech stock bubbles; they only depend on whether a natural disaster happens, providing a unique diversification tool for a modern investment portfolio.

The Future of the Reinsurance Industry

As we move further into the 21st century, the reinsurance industry is facing new challenges that will redefine its role in business finance. The way these companies handle emerging risks will have a direct impact on the cost of living and the cost of doing business globally.

Climate Change and Systemic Risk

Climate change is perhaps the greatest challenge to the reinsurance model. As the frequency and severity of weather-related events increase, reinsurers must constantly update their mathematical models to price risk accurately. If reinsurers raise their prices significantly, primary insurers must pass those costs on to consumers, leading to higher premiums for homeowners and businesses. This “hard market” environment makes reinsurance a focal point of economic discussions regarding climate resilience and urban planning.

The Role of Reinsurance in Modern Business Finance

Beyond natural disasters, the industry is pivoting toward systemic risks like cyber warfare and pandemics. The 2020 COVID-19 pandemic highlighted the need for massive “backstop” facilities to handle global business interruption. As digital assets become more valuable than physical ones, the role of the reinsurer in protecting the digital economy will only grow.

In conclusion, a reinsurer is much more than a secondary layer of the insurance market. It is a sophisticated financial engine that enables global commerce by absorbing volatility and providing the capital necessary for growth. Whether viewed as a tool for corporate solvency, a stabilizer of the global economy, or a unique investment opportunity, the reinsurance industry remains an indispensable component of the world of money. For anyone looking to understand the mechanics of risk and reward on a global scale, the reinsurer is the ultimate case study in financial resilience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.