The Foundation of Online Card Security

In the vast and ever-expanding landscape of e-commerce, the security of online transactions remains a paramount concern for consumers, merchants, and financial institutions alike. At the forefront of this digital defense stands 3D Secure verification, a critical protocol designed to add an extra layer of authentication for card-not-present (CNP) transactions. Its primary purpose is to protect against fraud by verifying the cardholder’s identity, ensuring that only the legitimate owner of a credit or debit card can make purchases online.

Defining 3D Secure

3D Secure, which originally stood for “Three-Domain Secure,” refers to a security protocol developed by EMVCo (a consortium founded by Europay, MasterCard, and Visa) to enhance the security of internet payments. The “three domains” represent the three parties involved in the authentication process: the acquirer domain (the merchant and their bank), the issuer domain (the bank that issued the card to the customer), and the interoperability domain (the infrastructure provided by the card scheme to connect the other two domains). This protocol acts as a secure communication channel, allowing the card issuer to authenticate the cardholder during an online purchase, similar to entering a PIN at a physical point-of-sale terminal.

Evolution from 3D Secure 1.0 to EMV 3D Secure (2.0)

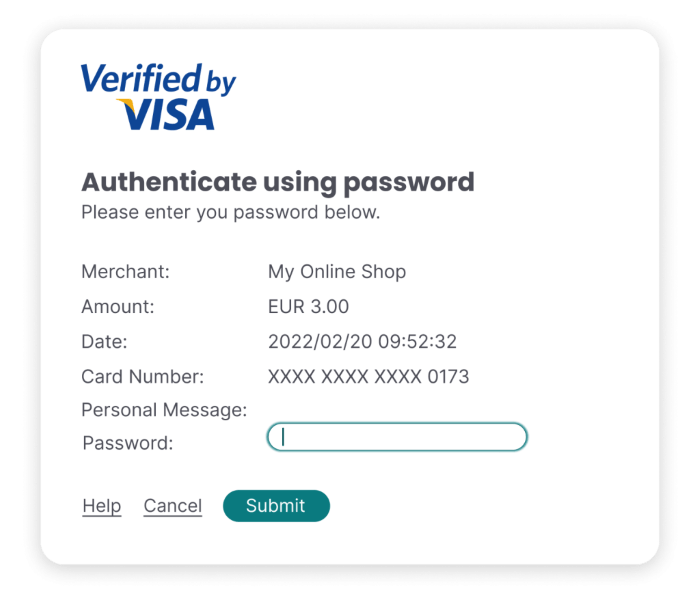

The initial iteration, often referred to as 3D Secure 1.0, was launched in the early 2000s under brand names like Verified by Visa and MasterCard SecureCode. While effective at reducing fraud, it often introduced friction into the checkout process, sometimes requiring users to remember static passwords or navigate pop-up windows, leading to higher cart abandonment rates. Recognizing these limitations and the evolving demands of modern e-commerce, EMVCo developed and released EMV 3D Secure, commonly known as 3D Secure 2.0 (or 3DS2). This newer version addresses many of the challenges of its predecessor by leveraging advanced risk-based authentication, real-time data exchange, and a more seamless user experience. It aims to reduce friction while simultaneously increasing security, marking a significant advancement in digital payment protection.

The Core Objective: Reducing Fraud

The fundamental objective of 3D Secure is to dramatically reduce card-not-present fraud. CNP fraud occurs when a credit card is used for an online, phone, or mail order transaction without the physical card being present. By requiring cardholders to authenticate themselves directly with their issuing bank, 3D Secure places the responsibility for verification with the entity best equipped to confirm identity. This mechanism helps to prevent unauthorized use of stolen card details, even if the card number, expiry date, and CVV are compromised, thereby protecting both consumers from financial loss and merchants from chargebacks associated with fraudulent transactions.

How 3D Secure Works: A Technical Overview

Understanding the technical mechanics behind 3D Secure is crucial for appreciating its role in securing online transactions. The process is a sophisticated interplay between the consumer, the merchant’s payment gateway, and the cardholder’s issuing bank, orchestrated through the card scheme’s secure messaging infrastructure. This multi-party communication ensures that a robust authentication decision can be made in real-time without significantly delaying the purchase flow, particularly with the advancements introduced in 3D Secure 2.0.

The Transaction Flow

When a consumer initiates an online payment on a merchant’s website that supports 3D Secure, the process begins even before the payment is formally authorized. The merchant’s payment gateway sends specific transaction data to the card network, initiating the 3D Secure flow. With 3D Secure 2.0, a vast array of contextual data points — including device information, shipping address, browser type, transaction history, and more — are collected and transmitted to the card issuer. The issuer’s risk engine then analyzes this data. In low-risk scenarios, the transaction may proceed through “frictionless flow” where authentication happens silently in the background without any visible interaction from the cardholder. For higher-risk transactions or when more data is needed, the issuer may request “challenge flow,” prompting the cardholder for additional verification directly. Once authenticated (or deemed low-risk), the transaction proceeds to standard authorization.

Authentication Methods

3D Secure 1.0 primarily relied on static passwords that users would set up with their bank. This often led to forgotten passwords and a cumbersome user experience. 3D Secure 2.0, however, significantly diversifies and modernizes authentication methods. While some issuers might still use static passwords, the protocol now heavily favors dynamic, multi-factor authentication. Common methods include:

- One-Time Passcodes (OTPs): A unique code sent via SMS to the cardholder’s registered mobile number or to their email address, which must be entered on the verification screen.

- Biometric Authentication: Leveraging fingerprint scanning or facial recognition through a banking app on a smartphone.

- App-Based Approval: A push notification sent to the cardholder’s banking app, requiring a simple tap to approve the transaction.

- Knowledge-Based Authentication (KBA): Answering security questions familiar only to the cardholder.

These varied methods aim to provide a more secure, yet often more convenient, authentication experience, adapting to modern consumer expectations and device capabilities.

The Role of Acquirers, Issuers, and Merchants

Each party plays a distinct role in the 3D Secure ecosystem. The merchant (and their acquiring bank) is responsible for implementing 3D Secure on their payment gateway. This involves integrating the necessary APIs and ensuring that transaction data is correctly sent and received. The card issuer (the cardholder’s bank) is at the heart of the authentication process. They receive the transaction data, run it through their risk assessment engines, and ultimately decide whether to request a challenge or proceed with frictionless authentication. They are also responsible for presenting the authentication challenge to the cardholder if required. The card schemes (Visa, MasterCard, etc.) provide the interoperability domain, acting as the secure messaging layer that facilitates communication between the merchant’s system and the issuer’s system, ensuring that data is securely transmitted and interpreted correctly across the diverse participants in the payment chain.

Key Benefits for Merchants and Consumers

The implementation of 3D Secure, particularly its advanced EMV 3D Secure 2.0 iteration, offers substantial benefits that extend across the entire e-commerce ecosystem. These advantages primarily revolve around enhanced security, reduced financial risk, and an improved overall transaction experience for all parties involved. For merchants, it means more secure sales and less liability; for consumers, greater peace of mind when shopping online.

Enhanced Fraud Protection

The most direct and significant benefit of 3D Secure is its capability to provide robust protection against card-not-present fraud. By adding an essential layer of authentication, it significantly reduces the risk of unauthorized transactions made using stolen card details. For consumers, this translates into greater security for their financial accounts and a reduced likelihood of becoming a victim of online fraud. Should a fraudulent transaction occur, the clear authentication trail provided by 3D Secure facilitates quicker resolution and dispute handling. For merchants, the protocol acts as a powerful deterrent against fraudsters, protecting their revenue and reputation from the damage caused by illegitimate purchases.

Liability Shift: A Merchant’s Advantage

One of the most compelling reasons for merchants to implement 3D Secure is the “liability shift.” In the absence of 3D Secure, if a customer disputes a transaction claiming it was fraudulent (a chargeback), the merchant typically bears the financial loss, even if they acted in good faith. However, when a transaction is successfully authenticated through 3D Secure, and a fraud-related chargeback occurs, the liability for that chargeback often shifts from the merchant to the card issuer. This is a crucial financial benefit for merchants, as it dramatically mitigates their risk exposure to CNP fraud. The card issuer, having authenticated the cardholder, assumes responsibility, thereby protecting the merchant’s bottom line from fraudulent disputes. This liability shift encourages broader adoption of the protocol.

Improved Customer Trust and Experience (especially with 2.0)

While 3D Secure 1.0 sometimes created friction that could deter customers, EMV 3D Secure 2.0 is specifically designed to enhance customer trust without sacrificing user experience. By leveraging sophisticated risk-based authentication, 3DS2 allows a significant proportion of transactions to proceed seamlessly through a “frictionless flow,” where authentication occurs in the background without any customer interaction. This means fewer interruptions and a quicker checkout process for legitimate customers. When a challenge is necessary, 3DS2 offers more user-friendly authentication methods like biometric verification or one-time passcodes, often integrated directly within the merchant’s website or the customer’s banking app, avoiding disruptive pop-ups. This balance of security and convenience builds greater customer confidence in online shopping, fostering a more positive and secure environment for digital commerce.

Implementing and Navigating 3D Secure

Integrating and navigating 3D Secure verification is a multifaceted process that involves technical integration for merchants and an understanding of the authentication steps for consumers. As digital security protocols continue to evolve, staying informed about best practices and future developments is key to maximizing the benefits of 3D Secure.

Merchant Integration Considerations

For merchants, implementing 3D Secure involves technical integration with their payment gateway or payment service provider (PSP). This typically requires updating existing payment processing systems to support the EMV 3D Secure 2.0 specification. Key considerations include:

- API Integration: Merchants need to integrate APIs provided by their PSP to send the required transaction data to the card issuer and receive authentication responses.

- Data Collection: Ensuring that the merchant’s checkout process collects and passes the extensive data points required for 3DS2’s risk-based authentication (e.g., device information, customer address, past transaction history).

- User Interface (UI) Handling: Designing the checkout flow to gracefully handle both frictionless and challenge authentication scenarios, providing clear instructions to customers if a challenge is required.

- Compliance: Adhering to the latest 3D Secure protocols and regional mandates (like Strong Customer Authentication in Europe) to maintain compliance and qualify for liability shift benefits.

Choosing a PSP that offers robust and up-to-date 3D Secure 2.0 solutions can significantly streamline the integration process and optimize the authentication flow.

The Consumer Experience: What to Expect

For consumers, the 3D Secure experience with 2.0 is designed to be as unobtrusive as possible. In many cases, particularly for routine or low-value purchases, they may not notice any additional steps as authentication happens behind the scenes. However, if their bank’s risk engine flags a transaction as potentially high-risk, they will be prompted to verify their identity. This “challenge” typically appears as a secure overlay or redirection within the merchant’s checkout page, asking for:

- A one-time passcode sent to their phone or email.

- Biometric verification (fingerprint or face ID) via their banking app.

- Approval via a push notification to their banking app.

- Answering security questions.

It is important for consumers to recognize these legitimate verification requests as part of a secure transaction and to ensure their contact information with their bank is up-to-date to receive authentication codes. Always verify the legitimacy of any such request and be wary of phishing attempts that mimic 3D Secure prompts.

Challenges and Future Outlook

Despite its advancements, 3D Secure still faces challenges. While 3DS2 significantly reduces friction, some customers may still abandon carts if they encounter an unexpected challenge, especially if they are unfamiliar with the process or if their authentication method is cumbersome. Technical complexities in integration can also be a hurdle for some merchants. However, the future of 3D Secure is optimistic. EMVCo continues to refine the protocol, focusing on even more seamless authentication methods, broader data utilization for risk assessment, and stronger integration with emerging payment technologies. As digital commerce evolves, 3D Secure will likely continue to adapt, integrating with new forms of identity verification and leveraging artificial intelligence to further enhance its ability to secure transactions while minimizing user disruption, remaining a cornerstone of digital security in the card-not-present environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.