Tax season is often viewed with a mixture of trepidation and administrative fatigue. However, for the financially savvy individual, filing taxes is not merely a legal obligation; it is a critical component of annual financial planning. It is an opportunity to audit your earnings, evaluate the efficiency of your investments, and reclaim overpaid capital through strategic deductions and credits.

The secret to a stress-free tax season lies in “document readiness.” By gathering the necessary information well before the deadline, you minimize the risk of errors that could lead to audits or delayed refunds. This guide outlines everything you need to file your taxes with precision, focusing on the intersection of personal finance management and regulatory compliance.

1. The Foundation of Filing: Personal Identification and Status Documentation

Before you can calculate a single cent of tax liability, you must establish the legal and structural framework of your tax return. This involves gathering basic identification for yourself, your spouse, and any dependents.

Social Security Numbers and Taxpayer Identification

The IRS uses Social Security Numbers (SSNs) as the primary tracking mechanism for individual taxpayers. You will need the exact SSNs for every person listed on your return. If you are a resident alien or do not have an SSN, you must provide your Individual Taxpayer Identification Number (ITIN). Ensuring these numbers are accurate is vital, as a single transposed digit can lead to the immediate rejection of an e-filed return.

Determining Your Filing Status

Your filing status—Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Surviving Spouse—determines your standard deduction amount and your tax brackets. If your personal situation changed during the year (e.g., a marriage, divorce, or the birth of a child), you must have the legal documentation to support your status. For those filing as Head of Household, you should maintain records that prove you paid more than half the cost of keeping up a home for a qualifying person.

Banking Information for Direct Deposits

In the modern financial landscape, paper checks are inefficient. To receive your refund as quickly as possible, you will need your bank’s routing number and your specific account number. This is an essential step in personal cash flow management, ensuring that your capital is returned to your control and can be redirected toward investments or high-yield savings accounts without delay.

2. Tracking Your Income: Organizing W-2s, 1099s, and Investment Statements

The core of your tax return is the reporting of “Total Income.” In the eyes of the IRS, almost all income is taxable unless specifically excluded. Organizing these documents is the most labor-intensive part of the process.

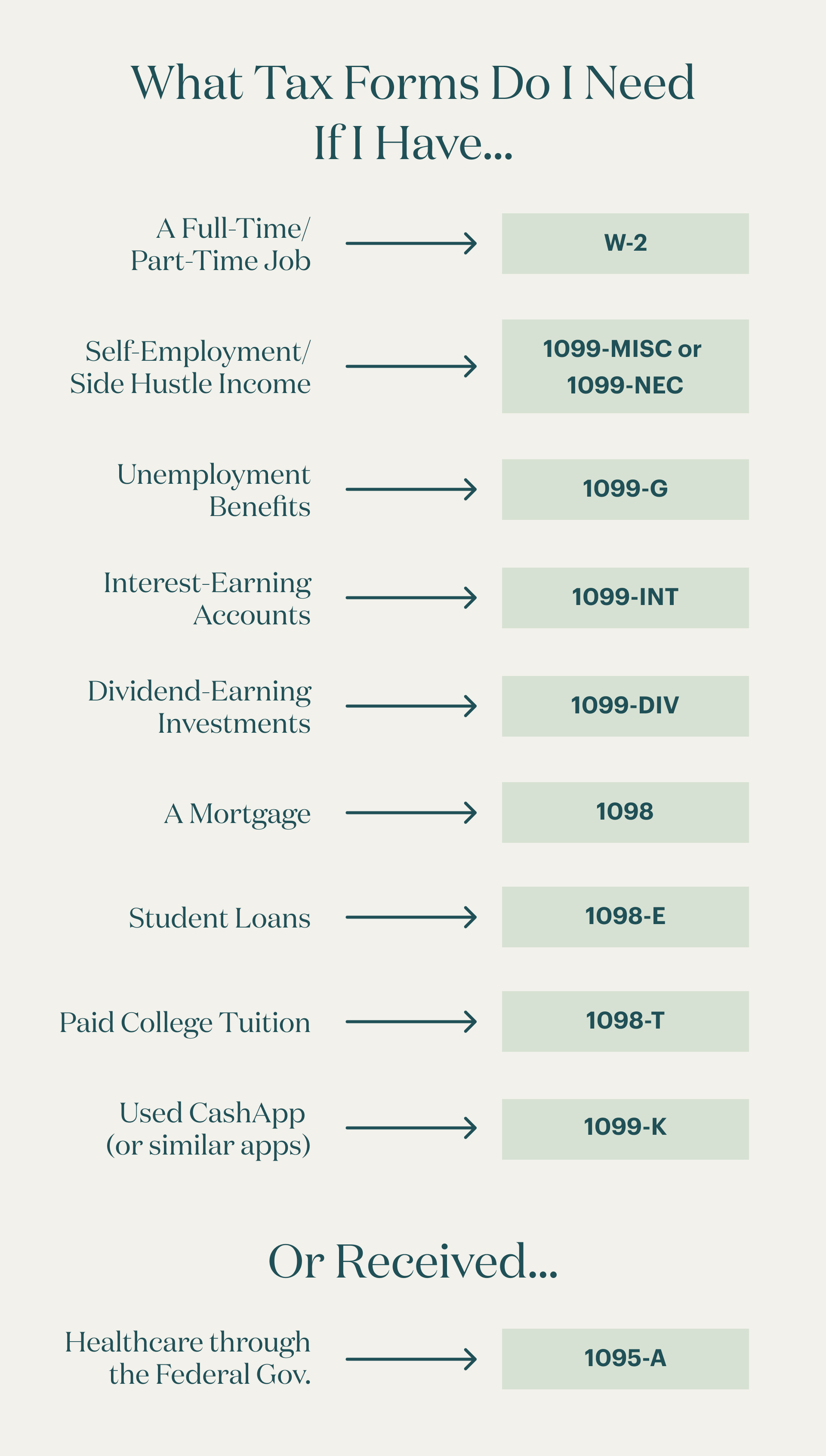

Employment Income (Form W-2)

If you are traditionally employed, your employer is required to provide Form W-2. This document summarizes your total earnings, as well as the federal, state, and local taxes already withheld. It also includes critical data on retirement contributions (like 401(k) deferrals) and health insurance premiums, which are often paid with pre-tax dollars.

The Gig Economy and Freelance Income (Form 1099-NEC and 1099-K)

With the rise of side hustles and digital entrepreneurship, many taxpayers now receive income from multiple sources. If you performed contract work and earned more than $600 from a single client, you should receive a 1099-NEC. Furthermore, if you sell goods or services through third-party payment processors (like PayPal or Stripe), you may receive a 1099-K. For the “Money” conscious individual, tracking these throughout the year using accounting software is preferable to a last-minute scramble.

Investment and Passive Income (1099-INT, 1099-DIV, and 1099-B)

Wealth building requires investment, and investments generate taxable events. You will need:

- 1099-INT: For interest earned on savings accounts or certificates of deposit (CDs).

- 1099-DIV: For dividends and distributions from stocks or mutual funds.

- 1099-B: For the proceeds from broker and barter exchange transactions. This is crucial for calculating capital gains or losses. If you sold assets at a loss, you can use those losses to “harvest” and offset your gains, a sophisticated financial strategy that reduces your overall tax burden.

3. Maximizing Returns: Navigating Deductions and Tax Credits

Once your income is established, the goal is to arrive at your “Adjusted Gross Income” (AGI) and then your “Taxable Income.” This is achieved through deductions and credits—the two most powerful tools in personal finance for preserving wealth.

Choosing Between the Standard Deduction and Itemizing

For the majority of taxpayers, the standard deduction is the most beneficial route due to its simplicity and increased value under recent tax laws. However, if your specific expenses—such as mortgage interest, state and local taxes (SALT), and significant medical expenses—exceed the standard deduction threshold, you should itemize using Schedule A. You will need receipts and statements to back up these claims.

Education and Student Loan Interest

Investing in human capital through education often comes with tax perks. If you paid tuition for higher education, look for Form 1098-T. This allows you to claim the American Opportunity Tax Credit (AOTC) or the Lifetime Learning Credit (LLC). Additionally, if you are paying off student loans, your lender will provide Form 1098-E, showing the interest you paid, which may be deductible even if you don’t itemize.

Healthcare and HSA Contributions

Health Savings Accounts (HSAs) are one of the few “triple-tax-advantaged” financial tools available. Contributions are tax-deductible, growth is tax-deferred, and withdrawals for qualified medical expenses are tax-free. You will need Form 5498-SA to report contributions and Form 1099-SA if you used HSA funds during the year.

Charitable Contributions and Business Expenses

If you itemize, keep a detailed log of charitable donations, including cash receipts and “fair market value” assessments for donated goods. For those with business income (Schedule C), you must have a rigorous record of expenses, including home office square footage, travel logs, and equipment purchases. These deductions lower your business’s net profit, directly reducing the amount of self-employment tax you owe.

4. The Financial Toolkit: Choosing Between DIY Software and Professional Assistance

How you file is just as important as what you file. The tools you choose can impact the accuracy of your return and the optimization of your financial strategy.

The Rise of Tax Preparation Software

For individuals with straightforward financial lives—a W-2 and perhaps some basic interest income—modern tax software is highly efficient. These platforms use interview-style interfaces to ensure you don’t miss common credits. From a financial perspective, these are cost-effective, often costing less than $100, which preserves your capital compared to expensive manual filing.

When to Consult a Certified Public Accountant (CPA)

If your financial situation involves rental properties, K-1s from partnerships, complex stock options (like ISOs or RSU vesting), or international assets, the ROI on a professional CPA is high. A tax professional doesn’t just “fill out forms”; they provide tax planning advice that can save you thousands of dollars in future liabilities. They are a strategic partner in your long-term wealth management.

5. Post-Filing Best Practices: Record Keeping and Future Planning

Filing the return is not the final step. To maintain a healthy financial life, you must look forward and secure your past.

The Three-Year Rule for Record Retention

The IRS generally has three years to audit a return. Therefore, you should keep digital or physical copies of all your tax documents, receipts, and the final return for at least three to seven years. In the digital age, scanning these into an encrypted cloud storage folder is the most efficient way to ensure they are available if needed while protecting your sensitive financial data.

Adjusting Withholdings for the Coming Year

A massive tax refund is not necessarily a “win”; it is essentially an interest-free loan you gave to the government. Conversely, a large tax bill suggests you underpaid throughout the year, potentially incurring penalties. Use the information from your completed return to adjust your W-4 with your employer. Aim for “tax neutrality,” where you owe nothing and receive nothing, allowing you to invest that money in real-time throughout the year to benefit from compound interest.

Strategic Contributions to Retirement Accounts

If you find that your taxable income was higher than expected, consider maximizing your contributions to a traditional IRA or 401(k). Depending on the timing, you may still have until the tax deadline to contribute to certain accounts for the previous tax year, providing a last-minute lever to lower your tax bill and increase your retirement security.

Conclusion

Filing your taxes is a yearly audit of your financial health. By approaching it with a organized mindset and a complete set of documents—from identity verification to complex investment statements—you transform a chore into a strategic financial exercise. Whether you are aiming to maximize a refund or minimize a liability, the key to success is preparation. Treat your tax documents as the vital financial assets they are, and you will navigate tax season with the confidence of a seasoned investor.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.