For many Americans, the transition into retirement is no longer a definitive “off-switch” for their careers. Whether driven by a passion for their craft, the need to combat inflation, or the desire to bolster a nest egg, an increasing number of retirees are choosing to work while simultaneously collecting Social Security benefits. However, this dual-income strategy comes with a complex set of rules known as the Social Security Earnings Test.

Understanding how much you can earn without triggering a reduction in your benefits is critical for effective financial planning. If you earn over a certain threshold before reaching your Full Retirement Age (FRA), the Social Security Administration (SSA) will temporarily withhold a portion of your benefits. This guide explores the mechanics of these limits, the tax implications of working in retirement, and the strategic considerations for maximizing your lifetime wealth.

Understanding the Social Security Earnings Test

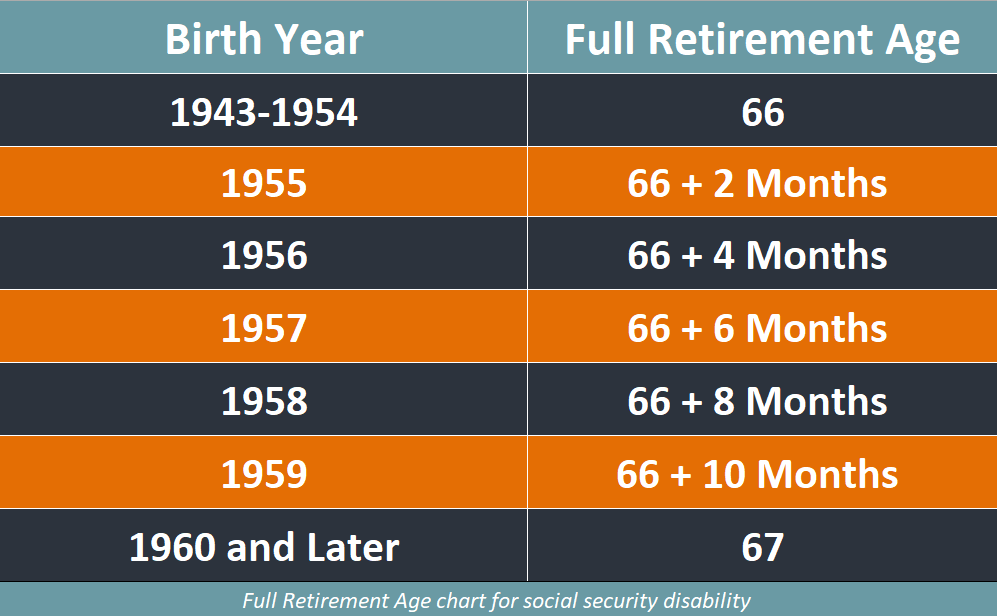

The Earnings Test is essentially a mechanism used by the SSA to determine if an individual is “retired enough” to receive full benefits. These rules only apply to those who have not yet reached their Full Retirement Age—which, for most people currently entering retirement, is between 66 and 67.

Working Below Full Retirement Age

If you are younger than your FRA for the entire year, the SSA applies a strict earnings limit. For 2024, that limit is $22,320. If your gross wages or net self-employment income exceeds this amount, the SSA will deduct $1 from your benefit payments for every $2 you earn above the limit.

For example, if you earn $32,320 (which is $10,000 over the limit), the SSA will withhold $5,000 of your Social Security benefits for that year. It is important to note that these limits are adjusted annually based on national wage trends.

The Year You Reach Full Retirement Age

The rules become significantly more lenient during the calendar year in which you actually reach your FRA. During this year, a higher earnings limit applies ($59,520 in 2024), and the reduction ratio improves. The SSA will only deduct $1 for every $3 you earn above the limit. Furthermore, the SSA only counts the money you earn in the months prior to your birthday month. Once you hit your birthday and officially reach FRA, the earnings test vanishes entirely.

Reaching Full Retirement Age: The No-Limit Zone

Once you reach your Full Retirement Age, the handcuffs are removed. You can earn any amount of money—whether it is $50,000 or $5,000,000—and still receive your full Social Security monthly benefit. At this stage, Social Security is treated as earned insurance rather than a needs-based or work-status-based benefit.

What Counts as “Earnings” (And What Doesn’t)

A common point of confusion for retirees is the definition of “income.” Not all money flowing into your bank account is considered “earnings” by the Social Security Administration.

Wages and Self-Employment Income

The SSA focuses strictly on “earned income.” This includes gross wages from an employer (the amount before taxes are taken out) and net earnings from self-employment. If you are a W-2 employee, they look at your pay stubs. If you are a freelancer or business owner, they look at your net profit as reported on your tax returns. Bonuses, commissions, and vacation pay also typically count toward the limit.

Passive Income and “Non-Earned” Wealth

Crucially, many forms of financial inflow do not count toward the earnings limit. This is excellent news for investors and those with diverse portfolios. The following do NOT trigger a reduction in Social Security benefits:

- Pensions and Annuities: Regular payments from a former employer or a private insurance contract.

- Investment Income: Interest, dividends, and capital gains from stocks, bonds, or mutual funds.

- IRA and 401(k) Distributions: Withdrawals from retirement accounts are considered deferred compensation, not current earnings.

- Rental Income: Unless you are a real estate professional whose primary business is managing properties, rental checks are generally considered passive.

- Inheritances and Gifts: One-time windfalls have no impact on the earnings test.

The Financial Impact of Exceeding the Limit: Loss or Deferral?

One of the greatest misconceptions regarding the earnings test is that the withheld money is “gone forever.” In reality, the Social Security Administration views this as a forced deferral rather than a permanent forfeiture.

The Benefit Recalculation

When you reach your Full Retirement Age, the SSA performs a recalculation of your benefits. They look back at all the months your benefits were withheld because of your earnings. They then increase your monthly benefit amount for the rest of your life to account for those withheld months.

In effect, by working and “losing” benefits now, you are essentially buying a higher monthly check for your later years. While this doesn’t help with immediate cash flow, it acts as a form of longevity insurance, providing a larger inflation-adjusted payment in your 80s and 90s.

The Special Monthly Rule

In the first year of retirement, many people retire mid-year after having already earned a significant salary. To prevent these people from being penalized for money earned before they retired, the SSA applies a “special monthly rule.” This allows you to receive a full benefit check for any whole month you are considered retired, regardless of your total yearly earnings.

Tax Implications of Working and Collecting Social Security

While the Earnings Test is about the amount of your check, taxes are about how much of that check you actually get to keep. When you combine wages with Social Security, you may find yourself in a “tax torpedo” where a high percentage of your benefits becomes taxable.

The Combined Income Formula

The IRS uses a specific formula to determine if your Social Security benefits are taxable. They look at your “Combined Income,” which is:

Adjusted Gross Income (AGI) + Tax-Exempt Interest + 1/2 of your Social Security Benefits.

Federal Tax Thresholds

- Individuals: If your combined income is between $25,000 and $34,000, you may have to pay income tax on up to 50% of your benefits. If it’s more than $34,000, up to 85% of your benefits may be taxable.

- Married Couples (Joint): If you and your spouse have a combined income between $32,000 and $44,000, you may pay tax on up to 50% of your benefits. Above $44,000, up to 85% of your benefits may be taxable.

When you work while collecting Social Security, your wages push your AGI higher, which often pushes your combined income into the 85% taxable bracket. It is vital to consult with a tax professional to model how an extra $10,000 in earnings might impact your total tax liability.

Strategic Planning for Working Retirees

Navigating the intersection of work and Social Security requires a proactive strategy. Depending on your health, lifestyle, and financial goals, you may choose to pivot your approach.

Delaying Benefits While Working

If you plan to earn significantly more than the annual limit, it often makes sense to delay claiming Social Security. For every year you delay past your FRA (up until age 70), your benefit increases by approximately 8% through Delayed Retirement Credits. By working now and waiting to claim, you avoid the earnings test entirely, reduce your current tax burden, and lock in a much higher permanent benefit for the future.

Leveraging Side Hustles

For those who want to stay active without triggering the earnings test, “micro-earning” or side hustles can be an effective middle ground. By keeping your earned income just below the $22,320 threshold (for 2024), you can enjoy the “best of both worlds”: a full Social Security check and a supplemental stream of income to fund travel or hobbies.

Reinvesting the Excess

If you choose to work and your benefits are reduced, consider the “forced savings” aspect of the recalculation mentioned earlier. If you don’t need the Social Security money to survive because your salary covers your expenses, the reduction isn’t a crisis. Instead, use your working years to maximize contributions to a Roth IRA or other tax-advantaged vehicles, further diversifying your future tax-free income.

Conclusion

The decision to work while collecting Social Security is a personal one, but it must be informed by the hard math of the SSA’s regulations. While the earnings test may seem like a penalty for productivity, it is ultimately a timing mechanism. By understanding the thresholds, knowing which types of income count, and preparing for the tax consequences, you can turn these rules to your advantage. Whether you choose to stay under the limit to maximize current cash flow or work through the limit to secure a higher future benefit, a well-mapped financial strategy will ensure that your “second act” is as prosperous as your first.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.