In the vast landscape of financial instruments, mortgage bonds often appear as a slightly opaque but intriguing option for investors. While the title “what are mortgage bonds” might sound specific to the real estate market, their implications ripple outwards, touching upon principles of Money (investing, personal finance, business finance), and even subtly hinting at the technological advancements that underpin their creation and management within the Tech sector, alongside the branding and trust associated with financial institutions in the Brand domain. This article aims to demystify mortgage bonds, exploring their nature, how they function, and their relevance in today’s investment climate, viewed through the lens of these broader website themes.

The Foundation: Understanding Mortgage-Backed Securities

At its core, a mortgage bond, more formally known as a Mortgage-Backed Security (MBS), represents a debt security that is collateralized by a pool of mortgages. Imagine a group of homeowners, each with their own mortgage on their property. Instead of individual investors directly holding each of these mortgages, a financial institution bundles a large number of these individual loans together. This collective pool then serves as the asset that backs the mortgage bond.

Investors who purchase these mortgage bonds are essentially buying a claim on the future principal and interest payments made by the homeowners whose mortgages are included in the pool. This concept is fundamentally rooted in the Money pillar of our website, directly addressing personal and business finance through investment vehicles. It allows for the securitization of what would otherwise be illiquid individual loans, transforming them into tradable securities.

How Does the Securitization Process Work?

The process of creating an MBS is a sophisticated financial engineering feat. A mortgage lender, such as a bank or a credit union, originates a large volume of mortgages. These mortgages, with their varying interest rates, loan terms, and borrower profiles, are then sold to a special purpose entity (SPE). The SPE is a legal construct, often established by an investment bank, designed to isolate the assets (the mortgages) from the originating entity. This isolation is crucial for bankruptcy remoteness, meaning that if the original lender faces financial difficulties, the mortgages within the SPE are protected.

The SPE then pools these mortgages and issues bonds against them. These bonds are then sold to investors in the capital markets. The payments received from the homeowners’ monthly mortgage payments (principal and interest) are then passed through to the bondholders, typically after deducting fees for servicing the loans. This entire process highlights a sophisticated application of financial structures, underpinned by robust legal frameworks and often facilitated by advanced technological systems for data management and transaction processing, a nod to the Tech domain. The credibility and transparency of the SPE and the issuing entity are paramount, linking back to Brand and reputation management in the financial sector.

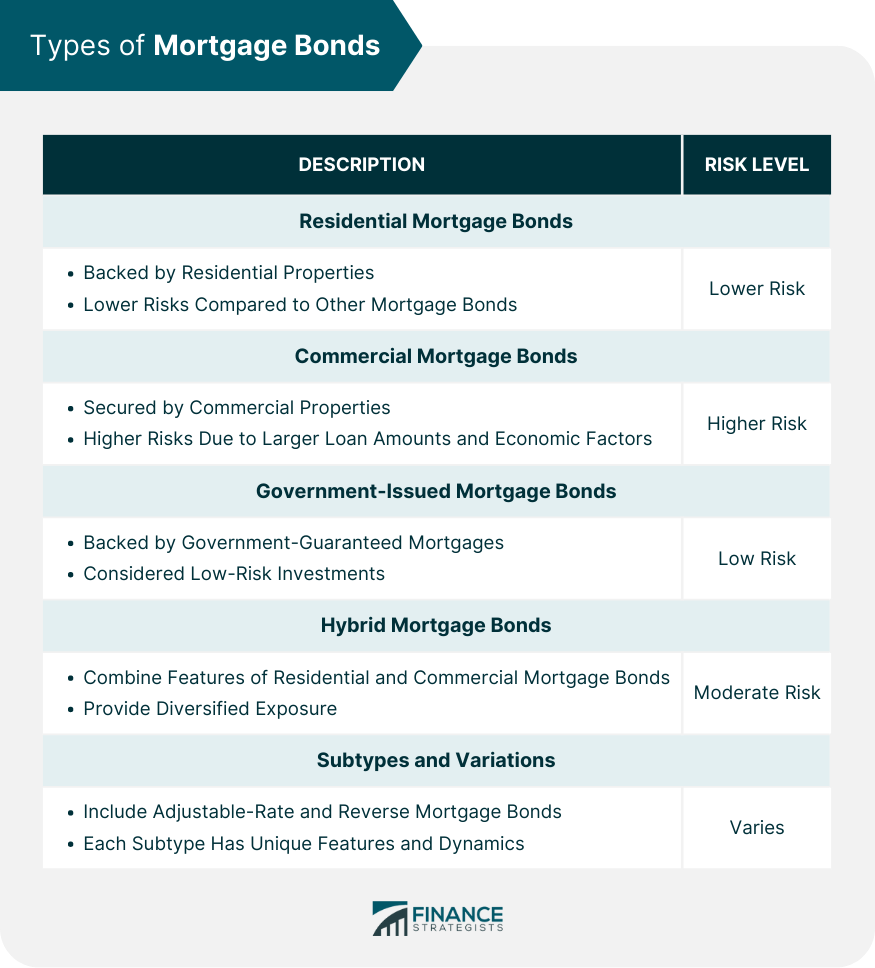

Types of Mortgage Bonds and Their Mechanics

Not all mortgage bonds are created equal. The structure and risk profile can vary significantly, leading to different classifications and investment considerations. Understanding these distinctions is key for any investor delving into this asset class.

Passthrough Securities: The Direct Conduit

The simplest form of MBS is a “passthrough” security. In this structure, the principal and interest payments collected from the underlying mortgages are directly passed through to the bondholders. If homeowners make their payments on time, those payments are distributed to the investors. Conversely, if homeowners default, the investors bear the brunt of that loss, although various forms of guarantees can mitigate this risk.

Passthrough securities can be further categorized based on the type of mortgage loans they contain:

- Agency Passthroughs: These are issued by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, or by Ginnie Mae, which guarantees securities backed by FHA and VA loans. These securities carry a very low credit risk because of the implicit or explicit guarantee from these government-backed entities. This guarantee is a crucial element that enhances investor confidence and is a testament to the Brand of these agencies.

- Non-Agency Passthroughs (or Private-Label MBS): These are issued by private financial institutions and are not guaranteed by government entities. They typically pool “jumbo” loans (loans exceeding conforming limits) or ” Alt-A” loans (loans made to borrowers with less-than-perfect credit history). These carry higher credit risk than agency passthroughs and consequently offer higher yields. The due diligence and credit assessment processes for these are often technologically advanced, utilizing sophisticated algorithms and data analytics, fitting within the Tech domain.

CMOs: Tailoring Risk and Return

Collateralized Mortgage Obligations (CMOs) represent a more complex evolution of MBS. Instead of simply passing through payments, CMOs are structured into different classes, or “tranches,” each with its own priority for receiving principal and interest payments. This tranching mechanism allows for the creation of securities with different risk and return characteristics, catering to a wider range of investor preferences.

Here’s a simplified look at how tranching works:

- Senior Tranches: These tranches have the highest priority and receive principal and interest payments first. They are generally considered the safest and offer the lowest yields.

- Mezzanine Tranches: These tranches are next in line and absorb payments after the senior tranches have been satisfied. They offer higher yields than senior tranches but carry more risk.

- Subordinate (or Junior) Tranches: These tranches are at the bottom of the payment waterfall. They receive payments only after all senior and mezzanine tranches have been paid in full. They carry the highest risk but also offer the highest potential yields.

This structuring allows investors to choose their desired level of exposure to prepayment risk (the risk that homeowners will pay off their mortgages early, leading to less interest income) and default risk. The ability to segment and customize these investment products is a prime example of financial innovation, often enabled by sophisticated analytical tools and platforms within the Tech sector. The success and demand for these complex instruments are also dependent on the reputation and perceived reliability of the issuing entities, highlighting the importance of Brand in financial markets.

The Role of Technology and Data in Mortgage Bonds

While the concept of mortgage bonds is financial, their modern existence is inextricably linked to technology. The entire lifecycle, from loan origination and securitization to trading and servicing, relies heavily on advanced digital infrastructure.

Data Management and Analytics

The creation of MBS involves aggregating and analyzing vast amounts of data from individual mortgages. This includes borrower credit scores, loan-to-value ratios, property valuations, interest rates, and payment histories. Sophisticated software and AI tools are employed to:

- Pool Mortgages: Algorithms help identify suitable mortgages for inclusion in a pool, ensuring diversification and adherence to specific investment criteria.

- Model Risk: Advanced statistical models, often powered by AI, are used to assess the prepayment and default risk of the underlying mortgages, which is crucial for pricing and structuring CMOs.

- Track Performance: Real-time data analytics allow for the continuous monitoring of the performance of the MBS, including payment streams and potential defaults.

This reliance on data and analytical prowess firmly places the mortgage bond market within the Tech landscape. The development of efficient, secure, and transparent platforms for managing these complex financial products is an ongoing area of innovation.

Digital Security and Blockchain

As with any financial transaction, security is paramount. The systems managing mortgage bond data must be robust and protected against cyber threats. Furthermore, emerging technologies like blockchain are being explored for their potential to enhance transparency, reduce transaction costs, and streamline the settlement process for MBS. The inherent immutability and distributed ledger nature of blockchain could revolutionize how ownership and transaction records are maintained, building further trust in the Brand of financial institutions adopting such technologies.

Investing in Mortgage Bonds: Risks and Rewards

For investors, mortgage bonds offer a unique blend of potential returns and inherent risks. Understanding these factors is essential for making informed investment decisions, aligning with the Money pillar of our website.

Potential Rewards

- Income Generation: MBS can provide a steady stream of income through regular interest payments, making them attractive for income-focused investors.

- Diversification: They can offer diversification benefits within a broader investment portfolio, as their performance may not always correlate directly with other asset classes.

- Potentially Higher Yields: Compared to traditional government bonds, MBS, especially non-agency ones, can offer higher yields due to the added credit and prepayment risks.

- Liquidity: Agency MBS, in particular, are highly liquid and actively traded in secondary markets, allowing for relatively easy buying and selling.

Key Risks

- Prepayment Risk: This is the risk that homeowners will pay off their mortgages earlier than expected, often when interest rates fall. For MBS investors, this means receiving their principal back sooner, which can be reinvested at lower prevailing rates, reducing future income. This is a unique risk associated with mortgage debt.

- Default Risk: While agency MBS are generally well-guaranteed, non-agency MBS carry a higher risk that borrowers will default on their loans, leading to potential losses for bondholders.

- Interest Rate Risk: Like all fixed-income securities, MBS are sensitive to changes in interest rates. When interest rates rise, the market value of existing MBS with lower coupon rates tends to fall.

- Liquidity Risk (for Non-Agency MBS): While agency MBS are very liquid, the market for some non-agency MBS can be less liquid, making them harder to sell quickly without a significant price concession.

The perception of risk and the trust placed in the issuer are heavily influenced by the Brand of the financial institution. A strong, reputable brand can instill confidence, even in complex financial products.

In conclusion, mortgage bonds are a significant component of the fixed-income market, representing a securitized form of real estate debt. Their existence and evolution are a testament to financial innovation, leveraging technological advancements for data management, risk assessment, and transaction processing. For investors, they offer opportunities for income generation and diversification, but these rewards come with inherent risks that must be carefully understood and managed. By dissecting the mechanics, types, and underlying technological and branding considerations, investors can gain a clearer perspective on what mortgage bonds truly are and their place in a diversified investment strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.