The dream of financial independence, flexibility, and a life built on one’s own terms often begins with the vision of an at-home business. In an increasingly digital world, the barriers to entry have significantly lowered, making it more accessible than ever to transform a skill, passion, or idea into a legitimate income stream. However, the path to success is not merely about having a great idea; it is fundamentally about astute financial planning, rigorous money management, and a clear understanding of the economic landscape. This guide delves into the financial underpinnings of launching and sustaining a thriving at-home business, ensuring your venture is not just a dream but a financially sound reality.

I. Understanding the Financial Landscape of At-Home Businesses

Starting any business requires a strategic approach, but an at-home business presents unique financial advantages and considerations. Grasping these nuances from the outset is crucial for setting a robust foundation.

The Allure of Low Overhead and High Flexibility

One of the most compelling financial benefits of an at-home business is the significantly reduced overhead. Without the need for commercial office space, utilities, or extensive office equipment, initial capital outlay can be dramatically minimized. This directly translates into a lower break-even point and a faster path to profitability. Furthermore, the inherent flexibility often means you can start small, test the waters, and scale operations as revenue permits, mitigating large upfront financial risks. This financial agility allows aspiring entrepreneurs to bootstrap their ventures more effectively, reinvesting early profits rather than relying heavily on external funding. For many, an at-home business begins as a side hustle, providing supplementary income without demanding a full financial commitment until it demonstrates viability.

Initial Investment vs. Potential Returns

While overhead might be low, an “at-home” business is rarely “no-cost.” There will invariably be some initial investment required, whether for a domain name and website hosting, specialized software, marketing materials, specific tools, or inventory. It’s imperative to meticulously categorize and estimate these startup costs. More importantly, entrepreneurs must project potential returns, not just in terms of revenue, but also profit margins after accounting for all operational expenses. A critical financial exercise is to determine the Return on Investment (ROI) for various startup expenditures. For instance, investing in professional branding or a high-quality website might seem like a significant upfront cost, but if it translates into higher conversion rates and customer trust, the long-term ROI can be substantial. Understanding this dynamic helps prioritize spending and avoid unnecessary financial drains.

Differentiating Between Side Hustle and Full-Time Venture

The journey of an at-home business often begins as a side hustle, allowing individuals to test their business idea without relinquishing the security of a primary income. Financially, this means careful segregation of personal and business funds from day one. As the business grows, the decision to transition from a side hustle to a full-time venture is a profound financial one. It involves assessing whether the business can reliably replace or exceed your current income, cover all personal living expenses, and provide for future financial security (e.g., retirement contributions, health insurance). A critical indicator for this transition is consistent, predictable cash flow and a clear financial runway – typically 6-12 months of living expenses saved – to absorb any initial dips in income. This distinction is not just about time commitment but a complete re-evaluation of your personal and business financial interconnectedness.

II. Crafting Your Financial Foundation: Planning and Budgeting

Success in any business, especially one starting from home, hinges on meticulous financial planning and budgeting. This isn’t just about tracking money; it’s about strategizing its allocation for optimal growth and stability.

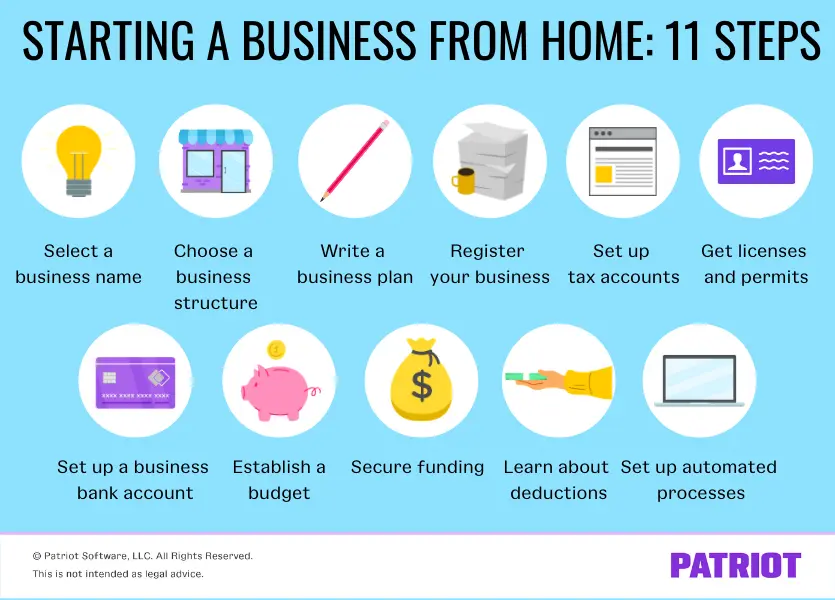

Developing a Robust Business Plan (with Financial Projections)

A business plan serves as your financial roadmap. While it might seem overly formal for an at-home venture, its financial sections are non-negotiable. This includes detailed sales forecasts, a profit and loss statement, a cash flow projection, and a balance sheet. These projections force you to confront the financial realities of your business idea: How much will you realistically sell? What are your fixed and variable costs? How much cash will be flowing in and out each month? These numbers are not just speculative; they inform pricing strategies, marketing budgets, and hiring decisions. Even if you’re not seeking external funding, a well-structured financial plan provides clarity, sets measurable goals, and acts as a benchmark against which to track actual performance, allowing for timely adjustments.

Estimating Startup Costs and Operating Expenses

Before you even make your first sale, money will likely go out. Startup costs might include business registration fees, initial product development, website creation, marketing collateral, and essential equipment. Operating expenses, on the other hand, are the recurring costs of keeping your business running: software subscriptions, raw materials (if applicable), advertising spend, utilities (a portion of your home utilities might be deductible), and potentially professional services (accountant, lawyer). Create a comprehensive spreadsheet detailing every anticipated expense, distinguishing between one-time startup costs and ongoing operational expenses. Overestimating these costs slightly is often a safer approach than underestimating, as it builds in a buffer for unforeseen expenditures.

Creating a Realistic Revenue Model and Pricing Strategy

How will your at-home business generate income? This is your revenue model. Will it be through direct product sales, service fees, subscriptions, advertising, or a combination? Once the model is clear, developing a sound pricing strategy is paramount. Pricing is not merely a reflection of your costs; it reflects your value proposition, market positioning, and desired profit margins. Research competitor pricing, understand your target customer’s willingness to pay, and factor in all your costs (including your own time/labor). Test different pricing tiers if possible. A common mistake is underpricing services or products, which can make your business unsustainable, even with high sales volume. Conversely, overpricing can deter customers. Find the “sweet spot” that ensures profitability while remaining competitive.

Importance of a Separate Business Bank Account

This is a foundational financial principle: never co-mingle personal and business funds. Open a dedicated business checking account as soon as your business is legally established (or even before, if you’re operating as a sole proprietor). This separation is critical for several reasons:

- Clarity: It makes tracking income and expenses infinitely easier, streamlining financial reporting and tax preparation.

- Professionalism: It establishes your business as a distinct entity, especially if you plan to accept payments through merchant services.

- Legal Protection: If your business is structured as an LLC or corporation, maintaining separate accounts is crucial for preserving the limited liability protection.

- Audit Preparedness: In the event of an audit, clearly segregated accounts make demonstrating legitimate business expenses straightforward.

III. Securing Funding and Managing Cash Flow

Even with low overhead, most at-home businesses require some form of funding, and all require diligent cash flow management to survive and thrive.

Bootstrapping Your Business: Self-Funding Strategies

Bootstrapping, or self-funding, is the most common and often recommended approach for at-home businesses. It involves leveraging personal savings, reinvesting early profits, and minimizing expenses to grow organically. Financially, this means starting lean, prioritizing essential expenditures, and deferring non-critical investments. It encourages resourcefulness and forces a strong focus on profitability from day one. Strategies include starting with a minimum viable product (MVP), leveraging free or low-cost tools, and personally handling tasks that might otherwise be outsourced. While slower, bootstrapping fosters financial discipline and ensures that growth is driven by actual market demand rather than external capital.

Exploring Microloans, Grants, and Small Business Loans

While bootstrapping is ideal, sometimes external capital is necessary for growth, inventory, or larger marketing pushes.

- Microloans: These are small loans, typically under $50,000, often provided by non-profit organizations or community development financial institutions (CDFIs) to small businesses, especially those in underserved communities. They can be a great option for at-home businesses needing a moderate cash injection.

- Grants: Though often competitive and specific to certain industries or demographics, grants offer non-repayable funds. Research local, state, and federal grant programs, as well as private foundations that support small businesses or particular entrepreneurial endeavors.

- Small Business Loans: Traditional banks and online lenders offer various loan products for small businesses. These typically require a solid business plan, financial projections, and sometimes collateral or a personal guarantee. SBA (Small Business Administration) loans, for instance, offer government-backed guarantees, making it easier for banks to lend to small businesses. Understand the interest rates, repayment terms, and eligibility criteria thoroughly before committing.

Mastering Cash Flow Management for Sustained Growth

Cash flow is the lifeblood of any business. It’s the movement of money in and out of your business, and it needs to be managed proactively. Even profitable businesses can fail due to poor cash flow.

- Invoice Promptly and Follow Up: For service-based businesses, ensure invoices are sent immediately upon completion of work and have clear payment terms. Don’t hesitate to follow up professionally on overdue payments.

- Manage Receivables and Payables: Try to collect money owed to you faster and pay your own bills strategically. If you can negotiate longer payment terms with suppliers without incurring penalties, do so.

- Maintain a Cash Flow Buffer: Always aim to have several months of operating expenses saved in your business bank account. This provides a safety net during lean periods or unexpected expenses.

- Forecast Cash Flow Regularly: Use your financial projections to anticipate periods of surplus or deficit and plan accordingly.

Setting Aside an Emergency Fund for Your Business

Just as individuals need personal emergency funds, businesses need their own. Unexpected events – a sudden dip in sales, a critical piece of equipment breaking down, an unforeseen legal expense – can derail an at-home business without a financial buffer. Aim to save at least 3-6 months’ worth of essential operating expenses in an easily accessible, separate savings account for your business. This fund provides peace of mind and allows your business to weather financial storms without resorting to high-interest debt or compromising crucial operations.

IV. Navigating Taxation and Financial Compliance

One of the most intimidating aspects of entrepreneurship for many is navigating the complex world of taxes and financial compliance. However, proactive understanding and meticulous record-keeping can make this manageable.

Understanding Business Structures and Their Tax Implications

The legal structure you choose for your at-home business (sole proprietorship, partnership, LLC, S-Corp, C-Corp) has significant financial and tax implications.

- Sole Proprietorship: Simplest, no distinction between you and your business. Profits and losses are reported on your personal tax return (Schedule C). You’re personally liable for business debts.

- LLC (Limited Liability Company): Offers personal liability protection (separates personal assets from business debts). Profits and losses can “pass-through” to your personal tax return, avoiding double taxation, or you can elect to be taxed as an S-Corp or C-Corp.

- S-Corp/C-Corp: More complex structures with stricter compliance requirements. C-Corps are subject to double taxation (corporate level and shareholder level), while S-Corps offer pass-through taxation similar to LLCs but with specific rules for owner compensation.

Consult with an accountant or business attorney to determine the best structure for your specific business goals, risk tolerance, and tax situation.

Tracking Income and Expenses Meticulously

Good bookkeeping is not optional; it’s essential for financial health and tax compliance.

- Use Accounting Software: Invest in user-friendly accounting software (e.g., QuickBooks Self-Employed, FreshBooks, Wave) from the start. These tools automate expense tracking, generate invoices, reconcile bank accounts, and produce financial reports.

- Categorize Everything: Properly categorize all income and expenses according to IRS guidelines. This makes it easier to identify deductible expenses and prepare accurate tax returns.

- Keep Receipts: Digitize and store all receipts for business purchases. While software can pull transactions, having original receipts (or digital copies) is crucial for substantiating deductions in case of an audit.

Estimating and Paying Quarterly Taxes

As an at-home business owner (especially a sole proprietor or LLC member), you are likely responsible for paying estimated taxes quarterly. The IRS requires you to pay income tax and self-employment tax (Social Security and Medicare) as you earn income throughout the year, rather than in one lump sum at tax time. Failure to pay enough estimated tax can result in penalties. Work with your accountant to estimate your quarterly tax liability and set up a system to ensure these payments are made on time. Many choose to set aside a percentage of every dollar earned into a separate savings account specifically for taxes.

Leveraging Deductions and Tax Credits for At-Home Businesses

One of the financial advantages of an at-home business is the potential for numerous tax deductions that can significantly reduce your taxable income.

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you may be able to deduct a percentage of your rent/mortgage, utilities, homeowners insurance, and repairs.

- Business Expenses: Deduct legitimate business expenses such as supplies, software, professional development, advertising, business travel, and a portion of internet/phone bills.

- Self-Employment Tax Deductions: You can deduct one-half of your self-employment taxes.

- Health Insurance Premiums: In certain situations, self-employed individuals can deduct health insurance premiums.

- Retirement Contributions: Contributions to self-employed retirement plans (like a SEP IRA or Solo 401(k)) are typically tax-deductible.

Staying informed about eligible deductions and credits, ideally with the guidance of a qualified tax professional, is paramount to optimizing your business’s financial performance.

V. Scaling and Long-Term Financial Growth

Starting is just the first step. For your at-home business to truly flourish and provide sustained financial security, you must strategically plan for growth and long-term financial health.

Reinvesting Profits for Expansion

Once your business consistently generates profit, a key financial decision arises: how much to take out for personal use versus how much to reinvest. Strategically reinvesting profits back into the business fuels growth. This could mean investing in better equipment, expanding your product line, hiring a virtual assistant, increasing your marketing budget, or developing new skills. The principle here is to use your business’s earnings to create more earning potential. However, this must be balanced with your personal financial needs. A common approach is to allocate a fixed percentage of profits for reinvestment, ensuring both business growth and personal remuneration.

Monitoring Key Financial Metrics (KPIs)

To make informed financial decisions about scaling, you must regularly monitor key performance indicators (KPIs). These metrics provide insights into your business’s financial health and trajectory.

- Revenue Growth: Is your income steadily increasing?

- Profit Margins: Are your gross and net profit margins healthy and stable?

- Customer Acquisition Cost (CAC): How much does it cost to acquire a new customer?

- Customer Lifetime Value (CLTV): How much revenue does a typical customer generate over their relationship with your business? A high CLTV relative to CAC indicates a sustainable business model.

- Cash Burn Rate: How quickly are you spending cash, especially if not yet profitable?

- Break-Even Point: At what sales volume do your revenues equal your costs?

Regularly reviewing these KPIs allows you to identify trends, pinpoint areas for improvement, and make data-driven financial adjustments.

Planning for Retirement and Personal Financial Security as a Business Owner

As an at-home business owner, you don’t have an employer contributing to your 401(k) or offering health insurance. Therefore, you must proactively manage your own personal financial security.

- Retirement Planning: Open a self-employed retirement account like a SEP IRA, Solo 401(k), or SIMPLE IRA. These offer tax advantages and allow for significant contributions, enabling you to build a substantial retirement nest egg.

- Health Insurance: Research options through your state’s marketplace (Affordable Care Act), professional organizations, or private insurers. Factor this cost into your business and personal budget.

- Disability and Life Insurance: Consider purchasing disability insurance to protect your income if you’re unable to work, and life insurance to protect your family.

- Personal Savings: Ensure you maintain a robust personal emergency fund separate from your business’s, covering at least 6-12 months of living expenses.

Your business should ultimately serve your personal financial goals, so integrating business and personal financial planning is non-negotiable.

Exit Strategies and Valuation (Briefly Touched Upon)

While it might seem premature when just starting, thinking about an eventual exit strategy can influence financial decisions from the outset. Do you envision selling the business? Passing it down? Or simply winding it down when you retire? Understanding potential valuation metrics (e.g., multiples of revenue or profit) can guide your growth strategies, ensuring you build a business that is not just profitable but also valuable. Building strong financial records, a clear customer base, and diversified revenue streams will all contribute to a higher valuation should you ever decide to sell.

Starting an at-home business is an exciting journey brimming with potential. By grounding your entrepreneurial spirit in rigorous financial planning, prudent money management, and a continuous commitment to understanding your business’s economic pulse, you can transform your vision into a sustainable, profitable, and truly fulfilling venture. The financial mastery of your at-home business isn’t just about managing numbers; it’s about securing your freedom and building the life you envision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.