In an increasingly digital world, the ability to transfer funds seamlessly and securely is no longer a luxury but a fundamental expectation. Google Wallet stands as a testament to this evolution, transforming the complex mechanics of financial transactions into an intuitive, accessible application residing on our mobile devices. More than just a tool for sending money, Google Wallet represents a sophisticated convergence of software design, robust security protocols, and an integrated digital ecosystem, redefining how individuals interact with their finances. This article delves into the technological underpinnings and operational mechanics that make Google Wallet a cornerstone of modern digital payments, focusing on its features, security, and user experience from a purely technological perspective.

The Technological Foundation of Google Wallet

Google Wallet isn’t merely an app; it’s a dynamic platform built upon years of innovation in digital finance. Its design philosophy emphasizes integration, security, and user-centricity, leveraging advanced software engineering to deliver a streamlined payment experience.

Evolution from Google Pay to an Integrated Digital Wallet

The journey of Google Wallet is a prime example of feature consolidation and user experience refinement in software development. Initially, Google’s payment solutions were somewhat fragmented, with Android Pay focusing on NFC-based tap-to-pay and Google Wallet (in its earlier iteration) handling peer-to-peer (P2P) transfers and loyalty cards. The re-branding and unification under “Google Pay” aimed to streamline this, creating a single interface for various payment functionalities. However, the current iteration, simply named “Google Wallet,” represents a strategic pivot towards an even broader digital wallet concept. This evolution wasn’t just a name change; it involved significant architectural restructuring. Google Wallet now acts as a comprehensive digital repository for not only payment cards but also loyalty cards, transit passes, event tickets, digital keys, and even digital IDs in some regions. This expanded scope demands a more robust and flexible backend infrastructure, capable of securely storing and instantly retrieving diverse types of sensitive data while maintaining high performance. The technical challenge lay in integrating these disparate functionalities into a single, cohesive user interface without compromising on security or ease of use.

Core Components and User Interface Design

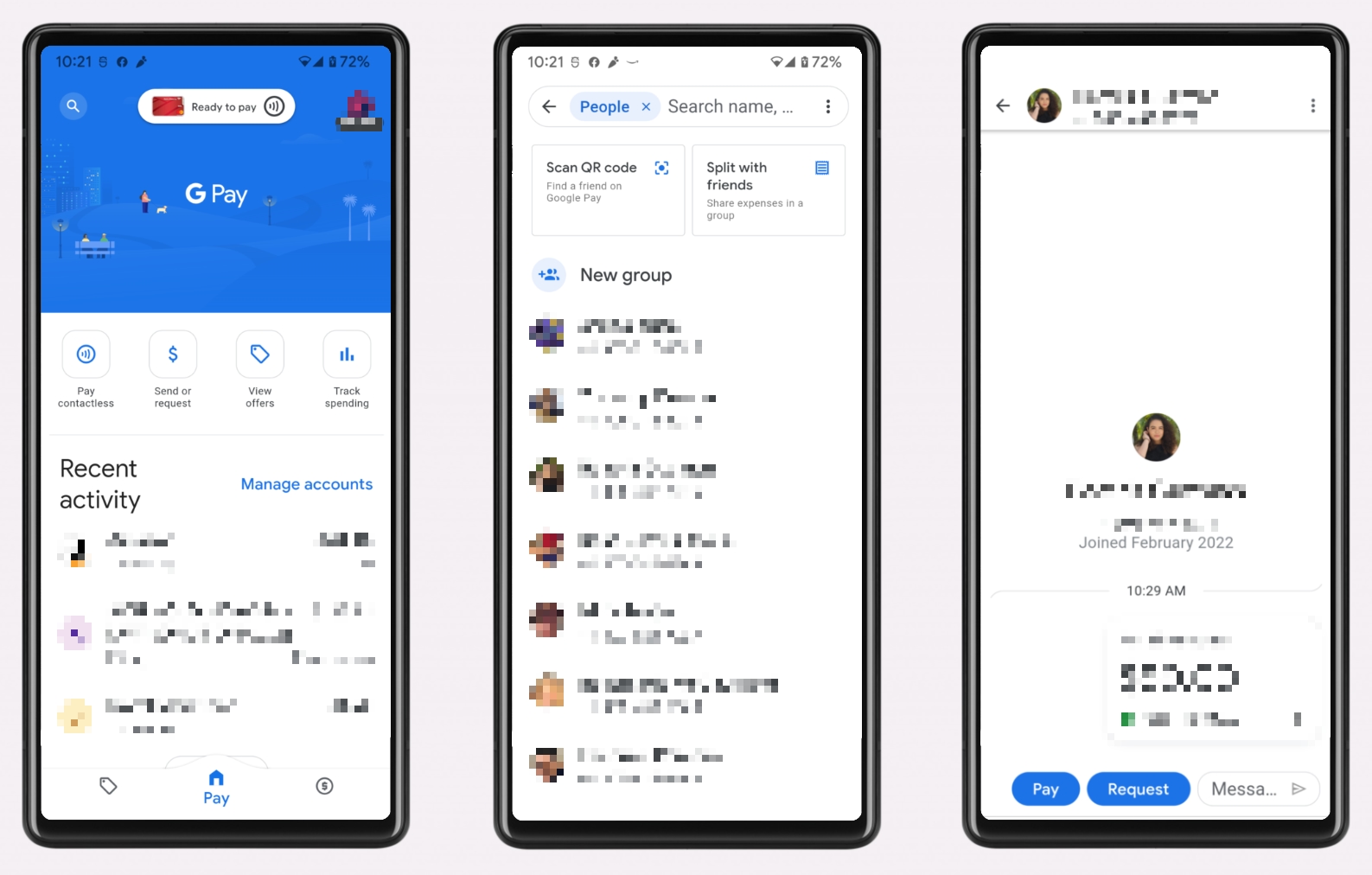

At its heart, Google Wallet is a marvel of software design, characterized by an intuitive user interface (UI) and a sophisticated underlying architecture. The application’s front end is meticulously crafted to be visually clear and easy to navigate, employing Google’s Material Design principles to ensure consistency and accessibility across various Android devices. Key UI elements, such as card carousels, quick action buttons for sending/requesting money, and categorized displays for passes, are designed for maximum discoverability and minimal cognitive load.

Beneath this polished surface lies a complex array of software modules. These include:

- Payment Gateway Integration: Secure APIs connect Google Wallet to various financial institutions and payment networks (Visa, MasterCard, American Express, etc.), enabling the tokenization and transmission of transaction data.

- Secure Element Management: For NFC-based payments, Google Wallet interacts with the device’s secure element (either a hardware chip or a software-based trusted execution environment) to store sensitive payment credentials and perform cryptographic operations.

- Data Synchronization Services: Cloud-based services ensure that user data (payment methods, passes) is synchronized across devices and remains accessible, while adhering to strict data privacy regulations.

- Push Notification System: A robust system provides real-time alerts for transactions, security events, and promotional offers, relying on Google’s Firebase Cloud Messaging or similar technologies.

The seamless interaction between these components allows users to add a new card with a simple camera scan, use biometrics to authenticate transactions, and view detailed transaction histories, all within a few taps.

Underlying Data Security Protocols

Security is paramount for any financial application, and Google Wallet employs multi-layered cryptographic and access control mechanisms to protect user data. When a payment card is added, it undergoes a process called tokenization. Instead of storing the actual 16-digit card number (Primary Account Number or PAN) on the device or transmitting it during a transaction, Google Wallet creates a unique, encrypted digital token or “virtual account number.” This token is tied to the specific device and transaction, making it useless if intercepted by unauthorized parties.

Furthermore, sensitive data is protected using industry-standard encryption protocols (e.g., AES-256) both at rest (when stored on Google’s servers and on the device) and in transit (during communication between the app, Google’s servers, and payment networks). Google’s secure infrastructure, built on years of experience with massive data centers, ensures that access to this encrypted data is heavily restricted and continuously monitored. The use of Secure Element technology (either hardware or software-based) on compatible devices isolates cryptographic keys and payment credentials from the main operating system, providing an additional layer of hardware-level security against malware and tampering.

Navigating the Google Wallet Interface: Sending Funds Step-by-Step

The primary utility of Google Wallet for many users is its facility for peer-to-peer money transfers. The process, while appearing straightforward to the end-user, involves sophisticated interactions between the app, the device’s operating system, and Google’s backend financial services.

Prerequisites for Digital Transactions

Before a user can send money, certain technical prerequisites must be met, ensuring both functionality and security.

- Device Compatibility: The user’s smartphone must be running a compatible version of Android (or iOS, though the feature set might vary slightly). This ensures the underlying operating system can support Google Wallet’s security features and APIs.

- Google Account: A valid Google Account is essential, acting as the primary identifier and authentication mechanism. This account is linked to Google’s broader ecosystem, allowing for seamless integration with other services.

- App Installation and Setup: The Google Wallet application must be downloaded from the Google Play Store (or Apple App Store). During initial setup, the app requests necessary permissions (e.g., contacts for recipient selection) and guides the user through linking at least one payment method.

- Linked Payment Method: To send money, a user must have a debit card or bank account linked to Google Wallet. The process of linking typically involves entering card details or bank login credentials, which are then securely verified by Google and the respective financial institution. This often leverages API connections with banks for instant verification and authorization.

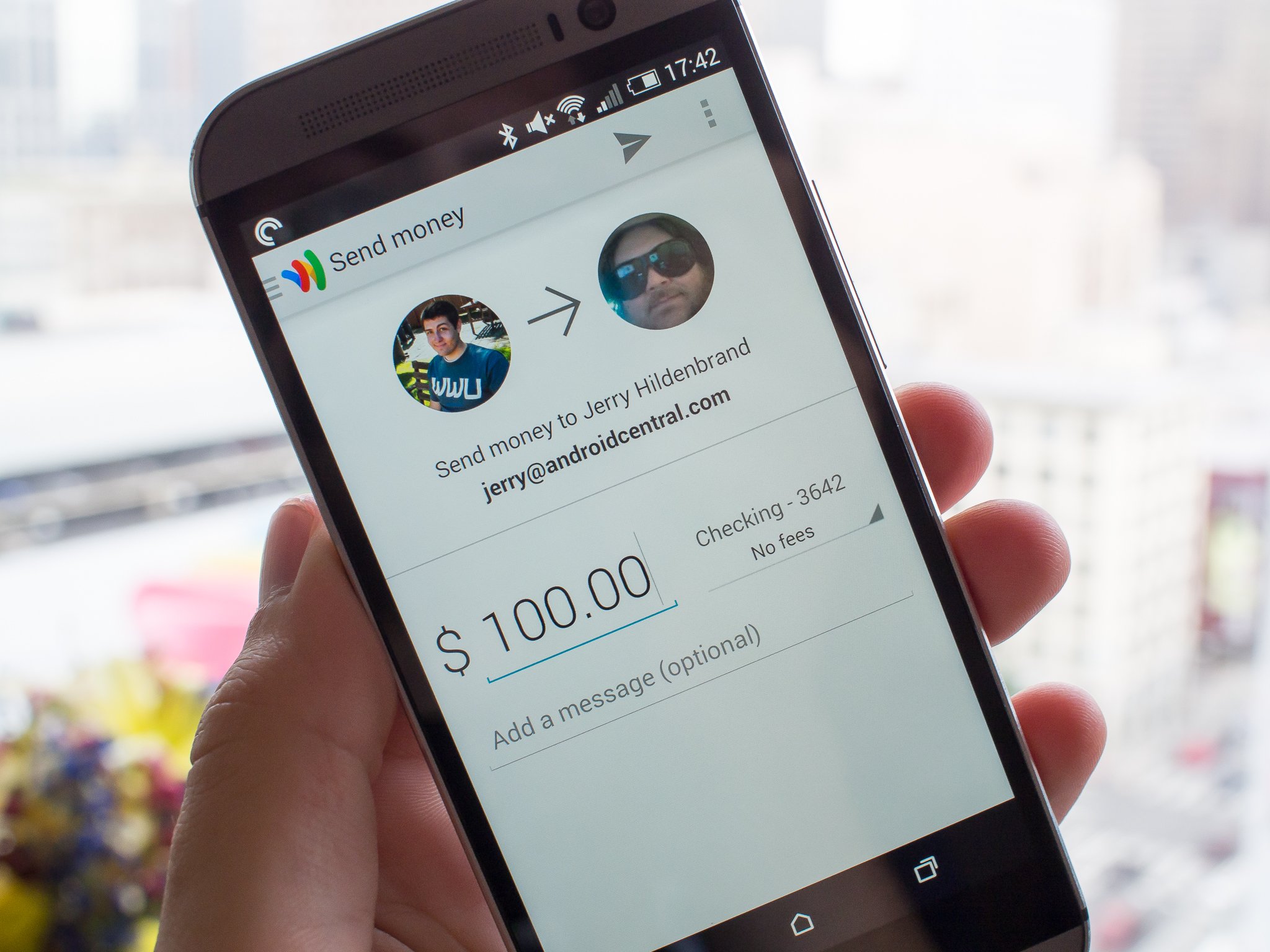

The “Send Money” Workflow: A User Experience Analysis

The process of sending money via Google Wallet is a prime example of effective user experience (UX) design streamlining complex backend operations.

- Initiating the Transfer: From the main Google Wallet interface, the user typically taps a prominent “Send” or “Send money” button. This action triggers the app to access the device’s contact list, enabling the user to select a recipient. This contact integration relies on operating system APIs for secure access to user data.

- Recipient Selection and Amount Entry: The user can select a recipient from their contacts or manually enter an email address or phone number. Once a recipient is chosen, the app presents a clear input field for the amount to be sent. The UI often includes a numerical keypad for easy entry.

- Payment Method Selection (if multiple are linked): If the user has multiple payment methods linked (e.g., several debit cards), the app allows them to select which one to use for the transaction. This choice instantly updates the transaction details, providing transparency.

- Adding a Note and Review: An optional field for a note or memo allows users to contextualize the payment. Finally, a review screen summarizes the transaction details – recipient, amount, payment method, and any fees (which are typically none for P2P transfers in Google Wallet when using a linked bank account or debit card). This screen is crucial for preventing errors before final confirmation.

- Authentication and Confirmation: The critical final step involves authenticating the transaction. This usually requires a PIN, fingerprint, or facial recognition, leveraging the device’s built-in biometric sensors or software-based authentication mechanisms. Upon successful authentication, the transaction request is securely sent to Google’s servers.

Real-time Transaction Processing and Notifications

Once authenticated, the transaction enters Google’s processing pipeline. Leveraging high-speed network infrastructure and sophisticated transaction processing systems, Google aims for near-instantaneous transfers.

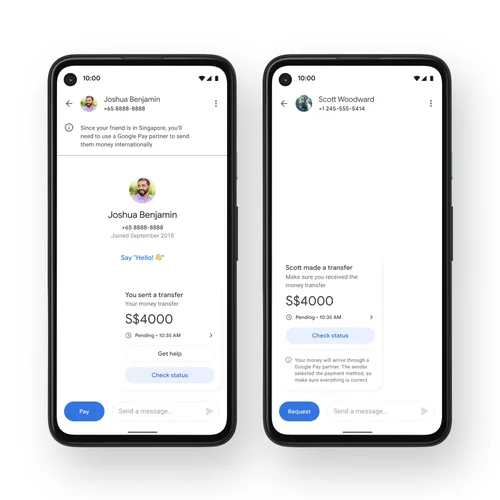

- Backend Processing: Google’s servers receive the tokenized transaction request, de-tokenize it (using secure keys), and communicate with the sending bank to debit the funds. Simultaneously, they notify the recipient’s Google Wallet account and initiate the credit to their linked payment method.

- Asynchronous Operations: While the user sees “money sent,” the actual bank transfers might involve asynchronous operations between different financial institutions, which Google manages on the backend.

- Real-time Notifications: Both the sender and receiver receive push notifications confirming the transaction status. These notifications, delivered via Google’s messaging services, provide immediate feedback, enhancing the user’s sense of control and security. Email confirmations are often sent as a secondary verification.

Ensuring Secure Digital Payments with Google Wallet’s Tech

The convenience of digital payments must be balanced with uncompromised security. Google Wallet employs a suite of advanced technologies to protect users’ financial information and prevent fraud.

Advanced Encryption and Tokenization for Transactions

As previously mentioned, tokenization is fundamental. When a user taps to pay or sends money, the actual card number is never shared with the merchant or the recipient. Instead, a unique, dynamically generated token is used. This token is tied to a specific device and can only be used for Google Pay transactions. If a malicious actor intercepts this token, it’s useless outside the Google payment ecosystem, significantly reducing the risk of card fraud. This process extends beyond NFC payments to online transactions where Google Wallet acts as the payment method. Encryption, specifically end-to-end encryption where possible, secures data in transit, making it unreadable to anyone without the correct decryption keys. Google’s cloud infrastructure itself is protected by multiple layers of physical and digital security, exceeding industry standards.

Multi-Factor Authentication and Biometric Security

Google Wallet significantly enhances security by integrating multi-factor authentication (MFA). While accessing the app typically requires unlocking the phone, authorizing actual transactions (especially for higher amounts or after a period of inactivity) demands an additional verification step. This most commonly involves:

- Biometrics: Fingerprint recognition (via capacitive or in-display sensors) and facial recognition (via dedicated hardware like Face ID on iPhones or sophisticated software on Android) leverage unique physiological attributes for authentication. These biometric data are typically stored securely within the device’s hardware and never leave it, meaning Google Wallet only receives a “yes” or “no” from the device regarding the match.

- PIN/Pattern: For devices without reliable biometrics or as a fallback, a user-defined PIN or screen unlock pattern provides a strong software-based authentication layer.

- Device-level Security: The fundamental security of Google Wallet also relies heavily on the overall security posture of the user’s mobile device, including strong screen lock mechanisms and regular operating system updates.

These layers ensure that even if a device is lost or stolen, unauthorized access to financial transactions within Google Wallet remains exceptionally difficult.

Fraud Detection and Prevention Algorithms

Google invests heavily in sophisticated AI and machine learning algorithms to continuously monitor transactions for suspicious activity. These systems analyze vast datasets of transaction patterns, user behavior, and device characteristics to identify anomalies that could indicate fraud.

- Behavioral Biometrics: Algorithms learn a user’s typical spending habits, locations, and transaction frequencies. Deviations from these patterns (e.g., a large transaction from a new location) can trigger additional security checks or flag a transaction for manual review.

- Real-time Risk Scoring: Every transaction is assigned a risk score in real-time. If a score exceeds a certain threshold, the transaction might be declined, require additional verification from the user, or even temporarily suspend the account to prevent further unauthorized activity.

- Network Analysis: Google also leverages its extensive network data to identify known fraudulent accounts, devices, or IP addresses, blocking transactions originating from these sources. This proactive approach significantly reduces financial losses for both users and financial institutions. Regular security audits and penetration testing further ensure the robustness of these systems.

Beyond Peer-to-Peer: Google Wallet’s Broader Digital Ecosystem

Google Wallet’s ambition extends beyond simple money transfers, aiming to be a universal digital repository for various aspects of a user’s life, powered by cutting-edge integration technologies.

NFC, QR, and Online Payment Integrations

Google Wallet acts as a versatile payment instrument, capable of facilitating transactions across multiple physical and digital touchpoints.

- Near Field Communication (NFC): For in-store purchases, Google Wallet leverages NFC technology. When a user taps their phone on a compatible payment terminal, the NFC chip within the device securely transmits the tokenized payment information. This technology relies on short-range wireless communication, enhancing security as the device must be in close proximity to the terminal.

- QR Code Payments: In some markets, particularly in Asia, QR code payments are prevalent. Google Wallet can generate QR codes for recipients to scan or scan merchant-generated QR codes to initiate payments. This method is particularly useful in environments where NFC terminals are not widespread.

- Online Payment Gateway: Beyond physical transactions, Google Wallet serves as a powerful online payment gateway. When shopping on e-commerce sites or within other apps, users can select “Pay with Google Wallet” (or “Google Pay”). This securely transmits payment details without requiring users to manually enter card numbers, streamlining the checkout process and leveraging the same tokenization security. This integration relies on robust API connections with online merchants and payment processors.

Future Trends in Digital Wallets: AI and Personalization

The trajectory of digital wallets, including Google Wallet, points towards even deeper integration with artificial intelligence (AI) and hyper-personalization.

- AI-Driven Financial Insights: Future iterations could leverage AI to provide more personalized financial insights, analyzing spending patterns, identifying subscription services, suggesting budget optimizations, or even predicting future expenses based on historical data. This moves beyond simple transaction viewing to proactive financial management.

- Contextual Payments: Imagine Google Wallet intelligently suggesting the most appropriate payment method based on your location, time of day, or past behavior. For instance, automatically selecting your transit pass when near a subway station or suggesting a specific loyalty card at a coffee shop.

- Voice and Gesture Integration: As AI assistants become more sophisticated, voice commands or even gesture controls could initiate payments, further reducing friction in the transaction process.

- Deeper Smart Device Integration: Seamless payments could extend to wearables, smart home devices, and connected cars, turning everyday objects into payment terminals or authentication points.

Interoperability and the Open Banking Movement

Google Wallet’s role within the broader financial ecosystem is also evolving. The global “Open Banking” movement, which advocates for secure data sharing between banks and third-party financial service providers with customer consent, presents a significant opportunity. Google Wallet, with its robust infrastructure and user base, is well-positioned to become a central hub for managing various financial accounts and services. This could involve direct API integrations with multiple banks, allowing users to view balances, transfer funds between accounts, and access tailored financial products from within the Wallet app, all while maintaining stringent security and privacy standards. This shift towards greater interoperability promises to empower users with more control and flexibility over their financial lives, solidifying Google Wallet’s position as a pivotal piece of the digital finance puzzle.

Conclusion

Google Wallet transcends the simple definition of a payment application; it is a sophisticated piece of digital infrastructure that skillfully blends technological innovation with user-centric design. From its robust multi-layered security protocols, including advanced encryption and tokenization, to its intuitive user interface and reliance on cutting-edge AI for fraud detection, every aspect is engineered to deliver a seamless and secure financial experience. As digital payments continue to evolve, Google Wallet remains at the forefront, continually integrating new features, embracing emerging technologies like AI and open banking, and adapting to the dynamic needs of a globally connected populace. It embodies the future of personal finance, making sending and managing money not just a task, but an integrated and effortless part of our digital lives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.