Understanding the cost of healthcare insurance can often feel like deciphering a complex financial puzzle. When considering a provider like Kaiser Permanente, which operates on a unique integrated healthcare model, the question of “how much” becomes even more nuanced than simply looking at a monthly premium. This comprehensive guide will delve into the various factors that influence Kaiser Permanente insurance costs, dissecting the components beyond just premiums, and offering insights to help you make an informed financial decision about your healthcare coverage.

Kaiser Permanente stands out in the healthcare landscape. It is not just an insurance provider; it’s an integrated managed care organization that functions as both the insurer and the provider. This means that Kaiser Permanente members typically receive their medical care from Kaiser Permanente doctors, hospitals, and medical facilities. This model, while offering numerous benefits in terms of coordinated care, also shapes how costs are structured and perceived.

Understanding Kaiser Permanente’s Unique Model

Before diving into the numbers, it’s crucial to grasp the fundamental operational philosophy of Kaiser Permanente. This understanding provides context for why their pricing structure might differ from traditional fee-for-service insurance plans.

The Integrated Healthcare System Explained

Kaiser Permanente operates as a closed system. Members receive care predominantly within Kaiser’s network of hospitals, clinics, and physicians. This integration aims to streamline communication between doctors, optimize treatment plans, and reduce administrative overhead. For patients, this often translates into a more seamless experience, with electronic health records easily accessible across different departments and a focus on preventive care to manage health proactively.

This vertical integration means that Kaiser Permanente manages both the financing (insurance arm) and the delivery (provider arm) of care. They are responsible for your health outcomes and the costs associated with them, which incentivizes efficiency and preventative medicine. This model can lead to more predictable costs for the organization, which can, in turn, influence the premiums offered to members.

Key Benefits of Choosing Kaiser Permanente

Beyond cost, the integrated model offers several advantages that can contribute to overall value. Coordinated care is a significant benefit; your primary care physician, specialists, and even pharmacists are all part of the same system, often sharing the same electronic health records. This can lead to fewer redundant tests, better communication, and a more holistic approach to your health.

Many members also appreciate the convenience of having most services — from primary care to specialty visits, labs, and pharmacies — located within the same medical centers. This can save time and reduce logistical challenges often associated with navigating fragmented healthcare systems. Moreover, Kaiser Permanente often emphasizes preventive care and wellness programs, which can lead to better long-term health outcomes and potentially lower future healthcare expenditures.

Potential Considerations and Trade-offs

While the integrated model offers benefits, it also comes with potential trade-offs, primarily concerning choice. Members typically must choose providers within the Kaiser Permanente network. If you have established relationships with doctors outside this system, or prefer the flexibility to choose any specialist, Kaiser Permanente’s model might feel restrictive. This lack of out-of-network coverage (except in emergencies) is a critical factor to weigh when assessing its suitability for your financial and healthcare needs. The value of an integrated system often comes with the trade-off of less flexibility in choosing individual providers outside the system.

Factors Influencing Your Kaiser Permanente Premium

Like all health insurance, the cost of a Kaiser Permanente plan is not a fixed figure. It’s a dynamic calculation influenced by a variety of factors. Understanding these elements is crucial for projecting your potential expenses.

Plan Type and Coverage Levels

Kaiser Permanente offers a range of plans, primarily focusing on Health Maintenance Organization (HMO) structures, which align perfectly with their integrated model. Within HMOs, you might find different tiers of coverage:

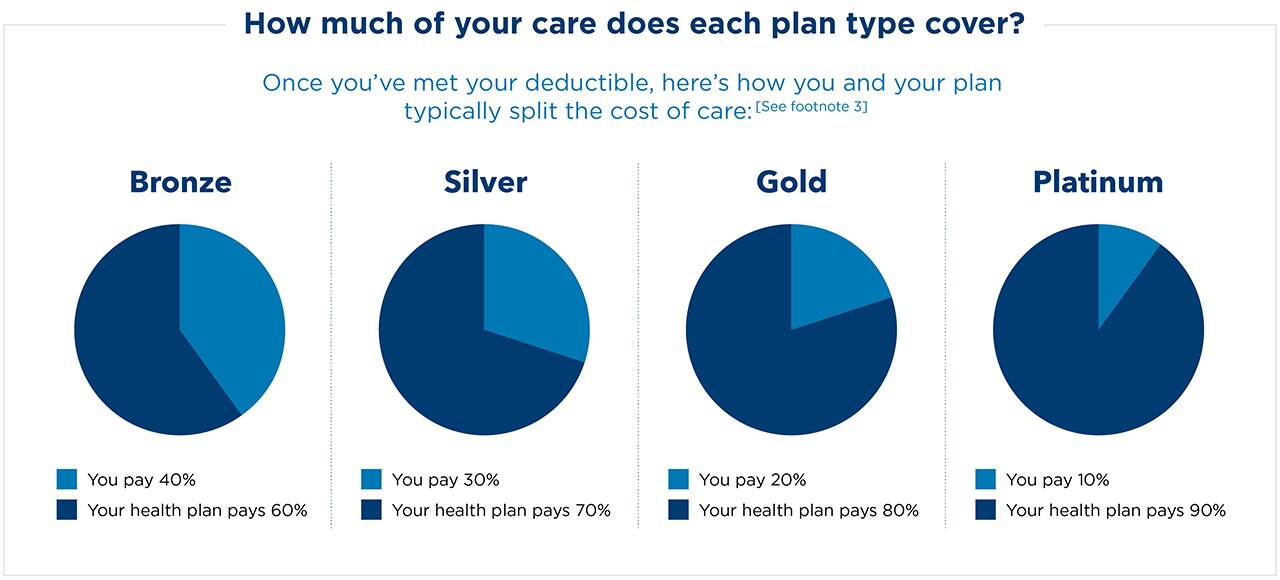

- Bronze Plans: Typically have the lowest monthly premiums but the highest deductibles and out-of-pocket costs when you receive care.

- Silver Plans: Offer a balance between monthly premiums and out-of-pocket costs, often with moderate deductibles. They are also the only plans eligible for cost-sharing reductions if you qualify based on income.

- Gold Plans: Come with higher monthly premiums but lower deductibles and out-of-pocket costs for medical services.

- Platinum Plans: Feature the highest premiums but the lowest deductibles and out-of-pocket costs, offering comprehensive coverage from the start.

The type of plan you select – and its associated actuarial value – will be the most significant determinant of your monthly premium. Kaiser Permanente also offers High Deductible Health Plans (HDHPs) that can be paired with Health Savings Accounts (HSAs), which we’ll discuss later.

Your Age, Location, and Household Size

These demographic factors play a direct role in premium calculation:

- Age: Generally, premiums increase with age. Older individuals typically pay more than younger individuals for the same plan, reflecting the higher average healthcare utilization associated with older age groups.

- Location: Healthcare costs vary significantly by region, city, and even ZIP code. Kaiser Permanente operates in specific regions (e.g., California, Colorado, Georgia, Hawaii, Maryland, Oregon, Virginia, Washington, and Washington D.C.). Premiums are tailored to the cost of healthcare delivery and market competition within each specific service area.

- Household Size: If you’re insuring multiple family members, the premium will be higher than for an individual plan. Each additional dependent (up to a certain number of children) will add to the total cost.

Income-Based Subsidies and Financial Assistance

For individuals and families purchasing plans through the Affordable Care Act (ACA) marketplace (also known as the exchange), significant financial assistance may be available.

- Premium Tax Credits: These subsidies reduce your monthly premium, making coverage more affordable. Eligibility is based on household income relative to the federal poverty level. The lower your income, the larger the tax credit you might receive.

- Cost-Sharing Reductions (CSRs): These subsidies lower your out-of-pocket costs like deductibles, copayments, and coinsurance. CSRs are only available for Silver plans and are also income-dependent.

Many people find that these subsidies make comprehensive Kaiser Permanente plans surprisingly affordable, sometimes even cheaper than less robust options from other providers. It’s crucial to check your eligibility on your state’s health insurance marketplace.

Tobacco Use and Other Demographic Factors

While the ACA largely eliminated factors like gender and health status from premium calculations, tobacco use can still impact your premium in some states. Insurers are permitted to charge tobacco users up to 50% more than non-tobacco users, although many states have chosen to limit or eliminate this surcharge. It’s a factor to be aware of, though less impactful than plan type or age.

Decoding the Cost Components Beyond Premiums

A low monthly premium can be attractive, but it only tells part of the financial story. True healthcare costs include what you pay out-of-pocket when you actually use medical services.

Deductibles: What They Are and How They Impact Out-of-Pocket Spending

A deductible is the amount you must pay for covered healthcare services before your insurance plan starts to pay. For example, if your plan has a $3,000 deductible, you’d pay the first $3,000 of covered medical expenses yourself before Kaiser Permanente begins to contribute.

- Impact: Plans with lower monthly premiums typically have higher deductibles, meaning you’ll bear more of the initial costs of care. Plans with higher premiums usually have lower deductibles or even $0 deductibles, offering coverage sooner. It’s vital to consider your expected healthcare usage. If you anticipate needing frequent care, a lower deductible plan, despite a higher premium, might save you money in the long run.

Copayments and Coinsurance: Your Share of Service Costs

Once you’ve met your deductible (if applicable), you’ll typically still have to pay a portion of the cost for services:

- Copayment (Copay): A fixed amount you pay for a covered healthcare service after you’ve paid your deductible. For example, you might have a $20 copay for a doctor’s visit or a $50 copay for an urgent care visit. Many plans, especially HMOs, offer certain services like primary care visits with just a copay, even before the deductible is met.

- Coinsurance: This is a percentage of the cost of a covered service you pay after you’ve met your deductible. For example, if your plan’s coinsurance is 20%, Kaiser Permanente pays 80% of the cost, and you pay the remaining 20%.

These “point-of-service” costs can add up, especially for expensive procedures or frequent visits.

Out-of-Pocket Maximums: Your Financial Safety Net

The out-of-pocket maximum (OOPM) is a crucial safety net. It’s the most you’ll have to pay for covered services in a plan year. Once you hit this limit, your insurance plan pays 100% of the costs for covered benefits for the remainder of the year.

- What Counts Towards the OOPM: Deductibles, copayments, and coinsurance usually count towards your out-of-pocket maximum. Monthly premiums, however, do not.

- Importance: Understanding your OOPM is vital for financial planning, especially if you anticipate a year with significant medical expenses. It caps your financial risk, providing peace of mind that you won’t face unlimited healthcare bills, even in the event of a catastrophic illness or injury.

Ways to Access Kaiser Permanente Coverage and Manage Costs

Kaiser Permanente coverage can be obtained through several avenues, each with distinct cost implications and benefits.

Employer-Sponsored Plans: The Most Common Route

A substantial portion of Kaiser Permanente members receive their coverage through their employer. Many employers subsidize a significant portion of the premium, making these plans very attractive. The specific plans and their costs will vary based on the employer’s negotiations with Kaiser Permanente. If your employer offers Kaiser Permanente, this is often the most cost-effective way to get coverage.

Individual & Family Plans (Marketplace & Direct Purchase)

If you don’t have access to employer-sponsored insurance, you can purchase Kaiser Permanente plans directly through your state’s health insurance marketplace (e.g., Covered California, Connect for Health Colorado) or sometimes directly from Kaiser Permanente outside the marketplace (though marketplace plans are necessary to receive subsidies). These are typically ACA-compliant plans. As discussed, individuals and families may be eligible for significant premium tax credits and cost-sharing reductions, which can dramatically lower the net cost of coverage.

Medicare Advantage Plans (Part C)

For individuals aged 65 and older, or those with certain disabilities, Kaiser Permanente offers Medicare Advantage plans. These plans replace original Medicare and provide comprehensive health and drug coverage through Kaiser Permanente’s integrated system. The costs for these plans can vary, often including a monthly premium (in addition to your Part B premium), but frequently come with low or $0 deductibles and predictable copays. Many offer extra benefits not covered by original Medicare, such as dental, vision, and hearing aid coverage.

Medicaid and CHIP Programs (if applicable in Kaiser service areas)

In some states where Kaiser Permanente operates, individuals and families with very low incomes may be eligible for Medicaid or the Children’s Health Insurance Program (CHIP). In certain regions, Kaiser Permanente contracts with state Medicaid agencies to provide care to eligible enrollees. These programs offer very low-cost or no-cost health insurance.

Utilizing Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

If you choose a Kaiser Permanente High Deductible Health Plan (HDHP), you may be eligible to open a Health Savings Account (HSA). HSAs are powerful financial tools:

- Tax-Deductible Contributions: Money you contribute reduces your taxable income.

- Tax-Free Growth: The money in the account grows tax-free.

- Tax-Free Withdrawals for Qualified Medical Expenses: You can withdraw funds tax-free for a wide range of medical expenses, including deductibles, copayments, and prescriptions.

- Portability: HSAs are owned by you, not your employer, meaning they go with you if you change jobs.

Flexible Spending Accounts (FSAs) are another option, often offered through employers, allowing you to set aside pre-tax money for healthcare expenses. While not as flexible as HSAs (they are “use-it-or-lose-it” generally), they can still provide significant tax savings on out-of-pocket medical costs.

Making an Informed Decision: Is Kaiser Permanente Right for Your Wallet?

Ultimately, determining “how much is Kaiser Permanente insurance” involves more than just looking at a price tag. It requires a holistic assessment of value, needs, and financial capacity.

Comparing Plans and Providers: Beyond Just the Premium

Don’t let the monthly premium be your sole decision-maker. Always compare plans based on:

- Total Expected Costs: Consider deductibles, copayments, coinsurance, and the out-of-pocket maximum.

- Network: Does Kaiser Permanente have facilities and providers conveniently located near you? Are you comfortable with their integrated model?

- Formulary: Check if your prescription drugs are covered and at what cost tier.

- Specific Benefits: Does the plan cover services important to you, like mental health, physical therapy, or maternity care, at an affordable rate?

Assessing Your Healthcare Needs and Usage Patterns

Your personal health profile is a critical factor.

- Healthy Individuals: If you rarely visit the doctor and primarily need coverage for emergencies, a plan with a lower premium and higher deductible (like a Bronze or HDHP plan) might be more financially prudent.

- Individuals with Chronic Conditions/Frequent Users: If you have ongoing health issues, take multiple prescriptions, or anticipate regular doctor visits, a plan with a higher premium but lower deductible and predictable copays (like Gold or Platinum) could save you money in the long run.

The Value Proposition of Integrated Care vs. Cost

Kaiser Permanente’s integrated model offers a unique value proposition: coordinated care, convenience, and a focus on preventive health. For many, the streamlined experience and belief in the system’s efficiency justify the costs. For others, the perceived lack of choice in providers might diminish that value, regardless of the price.

By carefully considering your financial situation, health needs, and comfort with Kaiser Permanente’s unique approach, you can accurately answer “how much is Kaiser Permanente insurance for me” and make a financially sound decision for your healthcare future. Researching specific plans in your region, utilizing marketplace calculators for subsidies, and understanding all cost components are the essential steps to navigating this significant financial commitment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.