For millions of students across the United States, the Free Application for Federal Student Aid (FAFSA) isn’t just a form; it’s a gateway. It’s the critical document that unlocks access to federal grants, scholarships, work-study programs, and low-interest federal student loans, making higher education an attainable dream rather than an insurmountable financial burden. However, the journey doesn’t end with a single submission. Financial aid, much like academic progress, requires an annual commitment. Renewing your FAFSA each year is as vital as the initial application, ensuring a continuous flow of support for your educational pursuits.

In the complex landscape of personal finance, education costs represent one of the most significant investments an individual or family can make. Navigating this terrain without the aid of federal programs can lead to substantial debt or, worse, the abandonment of educational goals. This guide delves into the crucial process of FAFSA renewal, framing it within a broader understanding of sound financial planning for your academic career. It aims to demystify the steps, highlight key considerations, and empower you with the knowledge to secure your financial aid year after year.

The Lifeline of Financial Aid: Why Renewing FAFSA is Crucial

The FAFSA serves as the cornerstone of financial assistance for post-secondary education. Without an annual submission, students risk losing eligibility for vital funding that can significantly reduce the out-of-pocket cost of college. Understanding its perpetual requirement and its profound impact on personal finance is the first step towards a financially secure academic journey.

Understanding the FAFSA’s Annual Requirement

Many first-time applicants might mistakenly believe that a single FAFSA submission covers their entire degree program. In reality, the FAFSA is an annual application. This yearly requirement stems from the need to assess a student’s and their family’s financial situation accurately, as circumstances can change dramatically from one year to the next. Income levels, family size, assets, and even the number of family members attending college can fluctuate, all of which directly influence financial aid eligibility. By renewing the FAFSA annually, the Department of Education can tailor aid packages to reflect a current and fair assessment of financial need, ensuring that resources are allocated effectively to those who need them most. From a personal finance perspective, this means consistent vigilance and proactive engagement with the process, treating it as an integral part of your yearly financial review.

The Impact of Financial Aid on Education Costs

The direct correlation between federal financial aid and the affordability of higher education cannot be overstated. Grants like the Pell Grant, for example, are a direct reduction of educational expenses, effectively “free money” that doesn’t need to be repaid. Federal student loans, distinct from private loans, often come with lower fixed interest rates, income-driven repayment options, and borrower protections that offer significant financial flexibility compared to their private counterparts.

Without these mechanisms, students would be forced to rely more heavily on personal savings, high-interest private loans, or forego education altogether. Renewing your FAFSA protects your personal balance sheet, reduces the necessity for high-cost debt, and allows you to focus more on your studies and less on the immediate financial strain of tuition and living expenses. It’s a strategic financial move that directly impacts your long-term economic well-being, influencing everything from future debt burden to career choices.

Common Misconceptions About Renewal

Several myths can deter students from timely FAFSA renewal. One common misconception is that if you didn’t qualify for aid in a previous year, you won’t qualify in subsequent years. This overlooks potential changes in financial circumstances—a parent losing a job, a sibling entering college, or a significant medical expense—all of which could alter your Expected Family Contribution (EFC) and make you eligible for aid. Another myth is that only “poor” students qualify. While need-based aid is central, federal student loans are often available regardless of income, making the FAFSA relevant for almost everyone. Understanding that FAFSA is a holistic financial assessment tool, not just for the most disadvantaged, is crucial for comprehensive financial planning around education.

Navigating the Renewal Process: Step-by-Step Guide

The FAFSA renewal process is designed to be streamlined, often simpler than the initial application. However, precision and attention to detail remain paramount to ensure accuracy and timely processing. Approaching it methodically can save time and prevent costly errors.

Gathering Your Documentation: What You’ll Need

Before you even log in, prepare your financial documents. This includes:

- Your Federal Student Aid (FSA) ID and password.

- Your Social Security number.

- Your driver’s license number (if you have one).

- For dependent students, your parents’ Social Security numbers and dates of birth.

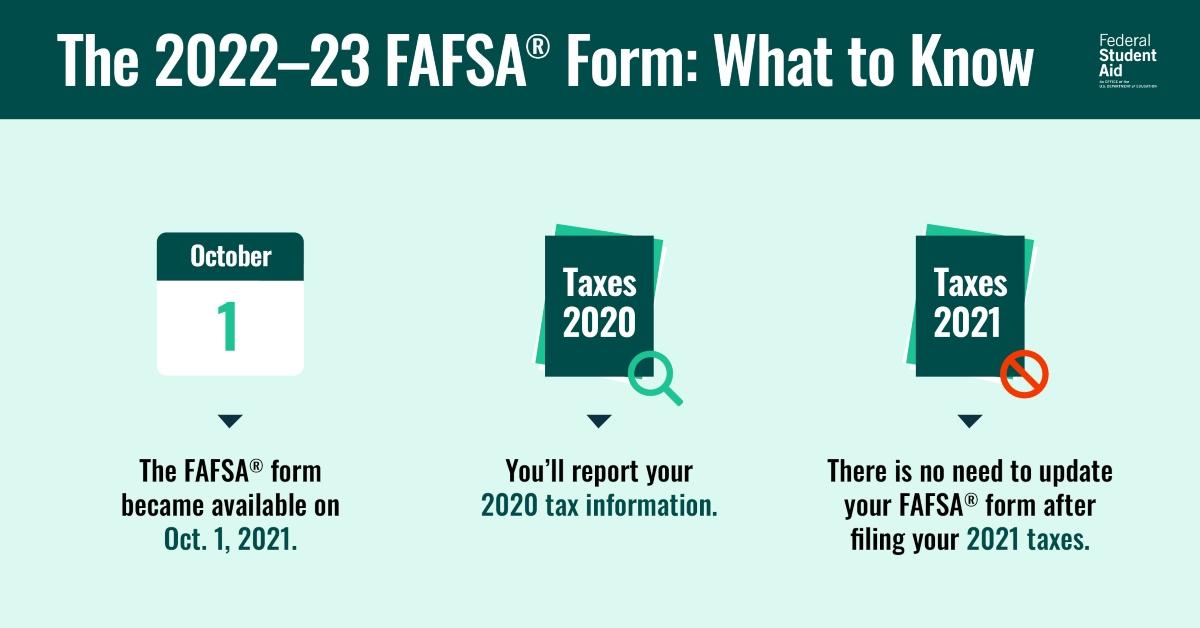

- Your and your parents’ (if dependent) federal income tax returns (for the relevant tax year—e.g., for the 2024-2025 FAFSA, you’ll need 2022 tax information).

- Records of other income received (e.g., child support received, untaxed income).

- Records of investments, savings, and checking account balances.

- Records of untaxed income.

Having these documents organized beforehand significantly expedites the online application process and minimizes the chance of errors. From a financial management perspective, this reinforces the importance of meticulous record-keeping.

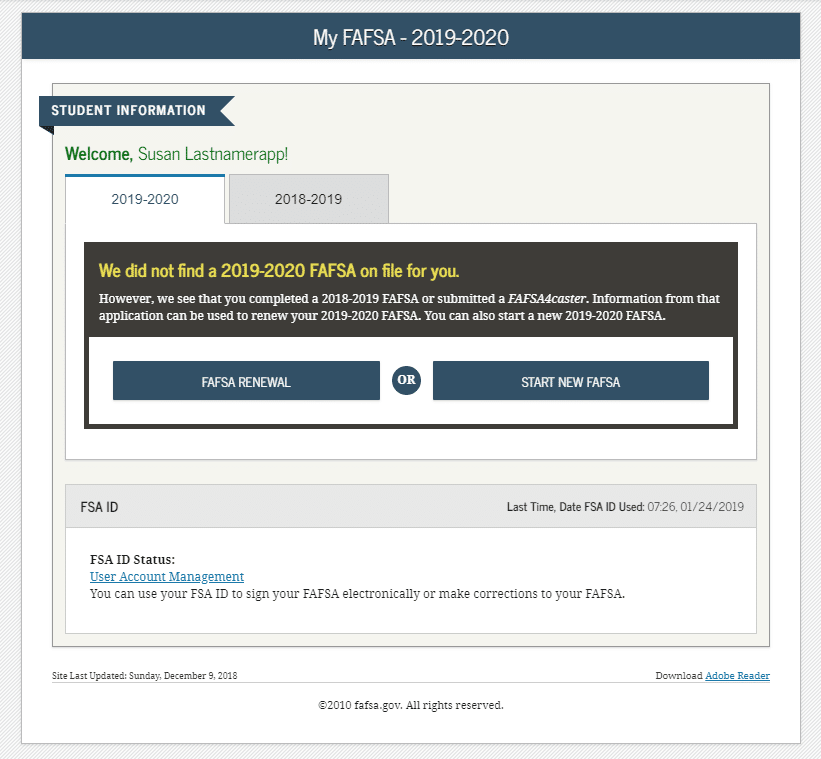

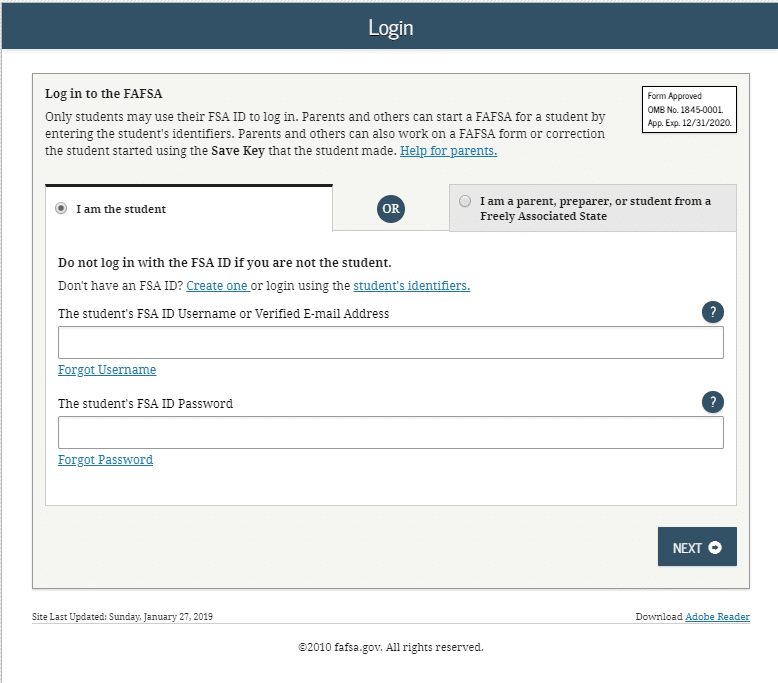

The Online Renewal Platform: FSA ID and Logging In

The primary method for FAFSA renewal is online at StudentAid.gov. You’ll need your FSA ID—a unique username and password that serves as your electronic signature and identifier. If you’ve forgotten it, there are recovery options, but it’s best to keep it secure and accessible. Once logged in, you’ll typically see an option to “Start a new FAFSA” or “Renew your FAFSA.” Selecting the renewal option will pre-fill much of your demographic information from the previous year, saving considerable time. Carefully review all pre-filled data for accuracy, making updates where necessary.

Utilizing the IRS Data Retrieval Tool (DRT)

One of the most powerful features for FAFSA renewal is the IRS Data Retrieval Tool (DRT). This tool allows applicants (and their parents, if dependent) to securely transfer tax information directly from the IRS into the FAFSA form. Not only does this save time and reduce manual data entry, but it also significantly minimizes the potential for errors, which can lead to delays or even necessitate corrections. Using the DRT is highly recommended as it provides the most accurate financial data, crucial for determining eligibility. It’s a prime example of technology enhancing financial accuracy and efficiency in government processes.

Reviewing and Submitting Your Application

Before hitting “submit,” thoroughly review every section of your renewed FAFSA. Pay close attention to sections that are prone to change year-to-year, such as income, assets, and household size. Ensure that all figures are accurate and that all required questions have been answered. An incomplete or inaccurate FAFSA can lead to delays in receiving your aid or a lower-than-expected aid package. Both you and your parents (if dependent) will need to sign the application electronically using your respective FSA IDs. Once submitted, make a note of your confirmation number. This step is the culmination of your annual financial aid planning.

Key Considerations for a Smooth Renewal

While the steps are straightforward, several key factors can influence the efficiency and outcome of your FAFSA renewal. Being aware of these elements can significantly improve your experience and ensure you receive the aid you’re eligible for.

Deadlines: Federal, State, and Institutional

Perhaps the most critical consideration for FAFSA renewal is deadlines. There are three types: federal, state, and institutional.

- Federal Deadlines: These determine eligibility for federal aid programs.

- State Deadlines: Many states have their own deadlines for state-specific financial aid programs, which can often be earlier than federal deadlines.

- Institutional Deadlines: Individual colleges and universities may have priority deadlines for their own institutional grants and scholarships.

Missing any of these deadlines, particularly state and institutional ones, can mean forfeiting access to significant “free money.” Always research and mark down all relevant deadlines, prioritizing the earliest ones. Early submission is almost always advantageous.

Changes in Financial Circumstances

Life happens, and financial situations can change unexpectedly. A job loss, a significant medical expense, separation or divorce, or a death in the family can dramatically impact a family’s ability to pay for college. If your or your family’s financial situation has changed substantially since the tax year used on your FAFSA (e.g., 2022 income for the 2024-2025 FAFSA), contact your college’s financial aid office immediately. They have the discretion to make professional judgments and adjust your aid eligibility based on current circumstances. This is a vital safety net in personal financial planning for education.

Understanding Your Student Aid Report (SAR)

After your FAFSA is processed, you’ll receive a Student Aid Report (SAR). This document summarizes the information you provided on your FAFSA and, most importantly, includes your Expected Family Contribution (EFC). The EFC is an index number that colleges use to determine how much financial aid you’re eligible to receive. Carefully review your SAR for any errors. If you find mistakes, you can make corrections online. Your SAR is your first glimpse into your aid potential, a key financial document that needs careful scrutiny.

The Verification Process: What to Expect

A percentage of FAFSA applications are selected for “verification.” This means the financial aid office at your college will request additional documentation to confirm the information provided on your FAFSA. This might include tax transcripts, W-2 forms, or proof of household size. While it can feel like an extra hurdle, it’s a routine process designed to maintain the integrity of federal aid programs. Respond promptly and accurately to all requests to avoid delays in aid disbursement. Proper financial record-keeping will make this process much smoother.

Maximizing Your Aid: Tips for FAFSA Renewal Success

Securing the maximum possible financial aid isn’t just about completing the form; it’s about strategic planning and informed decision-making. These tips can help optimize your FAFSA outcome.

Early Submission: The First-Come, First-Served Principle

The adage “the early bird gets the worm” often applies to financial aid. Many state and institutional aid programs operate on a first-come, first-served basis, meaning funds are limited and allocated until they run out. Submitting your FAFSA as soon as it becomes available (typically October 1st for the following academic year) dramatically increases your chances of accessing these time-sensitive funds. Procrastination can literally cost you thousands of dollars in grants and scholarships.

Accuracy is Paramount: Avoiding Errors

Even minor errors on your FAFSA can lead to processing delays or incorrect aid calculations. Double-check every numerical entry, especially income, asset values, and family size. Using the IRS DRT helps immensely, but manual entries still require careful review. Inaccuracies can necessitate corrections, prolonging the wait for your aid package and potentially impacting your college enrollment plans. Treat your FAFSA like a tax return—precision is critical.

Exploring Other Aid Opportunities

While FAFSA is the foundation, it’s not the only source of aid. Actively seek out scholarships from private organizations, local community groups, and the colleges themselves. Many scholarships are not need-based and can significantly supplement federal aid. Similarly, investigate work-study options available through your institution. A comprehensive approach to funding your education involves diversifying your aid sources.

Seeking Professional Guidance

Don’t hesitate to leverage the expertise of financial aid professionals. High school counselors, college financial aid officers, and even non-profit organizations often provide free assistance with FAFSA completion and financial planning. Their knowledge of complex aid formulas, specific deadlines, and available programs can be invaluable. Considering the financial stakes, seeking expert advice is a wise investment of your time.

Beyond the FAFSA: A Holistic Approach to Funding Your Education

While FAFSA is indispensable, it’s just one piece of a larger financial puzzle. A truly robust financial strategy for education involves exploring all avenues of funding and integrating them into a comprehensive personal finance plan.

Scholarships and Grants: The “Free Money” Hunt

Beyond federal grants, a vast ecosystem of scholarships and grants exists. These are funds that do not need to be repaid and are offered by a multitude of sources—from universities themselves to private foundations, corporations, and community groups. Dedicate time to searching for scholarships based on merit, need, academic interests, extracurricular activities, ethnicity, or even unique hobbies. Websites like Fastweb, College Board, and Scholarship.com are excellent starting points. Integrating a scholarship search into your annual financial planning is a smart move.

Student Loans: Understanding Your Options

Even with grants and scholarships, many students will need to utilize student loans. The FAFSA determines your eligibility for federal student loans, which are generally preferable to private loans due to their favorable terms (fixed interest rates, income-driven repayment plans, potential for forgiveness in certain public service roles, etc.). Understand the difference between subsidized (government pays interest while you’re in school) and unsubsidized loans. Borrow only what you need, as every dollar borrowed accumulates interest and will need to be repaid, impacting your future financial freedom. Carefully analyze the long-term cost and repayment obligations before committing to any loan.

Budgeting for College: A Financial Planning Essential

Finally, managing college costs effectively requires robust personal budgeting. Tuition and fees are just part of the equation. Factor in living expenses (rent, utilities, food), books and supplies, transportation, and personal expenses. Create a realistic budget, track your spending, and adjust as needed. Financial aid helps cover costs, but responsible spending and diligent budgeting are paramount to avoid unnecessary debt and ensure your aid stretches as far as possible. This ongoing financial discipline during your academic career lays the groundwork for sound financial habits post-graduation.

Renewing your FAFSA is more than just an annual task; it’s a cornerstone of effective personal finance for students. By understanding its importance, meticulously navigating the process, and integrating it into a broader financial strategy, you can unlock the educational opportunities you seek without compromising your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.