Student loans represent a significant financial commitment for millions of individuals worldwide, often serving as the gateway to higher education and career opportunities. Yet, the path to repaying these loans can feel daunting, fraught with complex terms, varying interest rates, and a multitude of repayment options. Navigating this landscape effectively is not merely about making monthly payments; it’s about strategically managing your debt to achieve financial freedom and build a secure future. This comprehensive guide aims to demystify the process, offering insights and actionable strategies to help you conquer your student loan debt with confidence and clarity.

Understanding Your Student Loan Landscape

Before devising a repayment strategy, it’s crucial to thoroughly understand the nature of your student loans. Not all loans are created equal, and their terms significantly impact your repayment journey.

Federal vs. Private Loans: Key Differences

The primary distinction lies between federal and private student loans. Federal loans, issued by the U.S. government, often come with more borrower-friendly features. These include fixed interest rates, income-driven repayment (IDR) plans, deferment and forbearance options for financial hardship, and access to various loan forgiveness programs. Examples include Direct Subsidized, Unsubsidized, PLUS, and Perkins Loans.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions. They typically have variable interest rates (though fixed-rate options exist) that can fluctuate over time, potentially increasing your monthly payments. Private loans also offer fewer borrower protections and lack the extensive repayment flexibility and forgiveness programs found with federal loans. Understanding which type of loans you hold is the foundational step in planning your repayment.

Knowing Your Loan Terms and Interest Rates

Digging into the specifics of each loan is paramount. For every loan you possess, identify:

- The principal amount: The original sum borrowed.

- The interest rate: This determines how much extra you pay over time. A higher interest rate means a more expensive loan.

- The loan servicer: This is the company that handles your billing and other loan-related services. You’ll make payments to them.

- Repayment start date and term: When payments begin and how long you have to repay the loan.

- Loan type: Subsidized, unsubsidized, fixed-rate, variable-rate.

Federal loan interest rates are set annually by Congress and are typically fixed for the life of the loan. Private loan rates are often based on your creditworthiness and market conditions, meaning they can vary significantly. Compiling this information in a spreadsheet can provide a clear overview of your total debt burden and help you prioritize which loans to tackle first.

The Impact of Accrued Interest

Interest is the cost of borrowing money, and it accrues on your loan principal. For unsubsidized federal loans and all private loans, interest begins accruing immediately, even while you’re in school or during grace periods. If this interest is not paid, it can be capitalized (added to your principal balance), leading to a larger loan balance and meaning you’re paying interest on interest. Understanding how interest accrues and capitalizes is vital, as it highlights the financial benefit of paying down your loans faster and, if possible, making interest-only payments while still in school or during grace periods.

Navigating Repayment Plans and Options

Once you understand your loans, the next step is to explore the various repayment plans available. The right plan can significantly impact your monthly budget, total interest paid, and the overall duration of your repayment.

Standard and Graduated Repayment Plans

The Standard Repayment Plan is the default for most federal loans. It features fixed monthly payments over a 10-year term (or up to 30 years for consolidated loans). This plan results in the lowest total interest paid over the life of the loan because you pay it off fastest.

The Graduated Repayment Plan also pays off your loan in 10 years, but your payments start lower and gradually increase every two years. This can be beneficial if your income is expected to rise over time, but you’ll pay more interest overall compared to the Standard Plan. While these plans offer predictable payment structures, they may not be suitable for everyone, especially those with high debt-to-income ratios immediately after graduation.

Income-Driven Repayment (IDR) Strategies

For federal student loan borrowers facing financial challenges, Income-Driven Repayment (IDR) plans offer a vital safety net. These plans adjust your monthly payment based on your income and family size, typically capping payments at 10-20% of your discretionary income. Any remaining balance after 20 or 25 years of payments (depending on the plan) may be forgiven, though the forgiven amount could be taxable.

There are several IDR plans, including:

- REPAYE (Revised Pay As You Earn): Generally caps payments at 10% of discretionary income.

- PAYE (Pay As You Earn): Also 10% of discretionary income, but often with stricter eligibility requirements.

- IBR (Income-Based Repayment): Caps payments at 10% or 15% of discretionary income.

- ICR (Income-Contingent Repayment): Caps payments at 20% of discretionary income or what you’d pay on a fixed 12-year plan, whichever is less.

IDR plans can significantly lower your monthly burden, making student loan repayment more manageable. However, they often extend the repayment period, leading to more interest paid over time and potential tax implications on forgiven balances. Regularly recertifying your income and family size is crucial to keep your payments accurate.

Exploring Deferment and Forbearance

If you encounter unexpected financial hardship, federal student loans offer options for temporary relief: deferment and forbearance.

- Deferment allows you to temporarily postpone your loan payments. For certain federal loans (subsidized loans, Perkins loans), the government may pay the interest that accrues during the deferment period. Common reasons for deferment include unemployment, active duty military service, or enrollment in school.

- Forbearance also allows you to temporarily stop or reduce your loan payments. However, interest typically accrues on all loan types (including subsidized) during forbearance and may be capitalized. Forbearance is usually granted for shorter periods and for reasons not covered by deferment, such as medical expenses or other financial difficulties.

While these options provide temporary relief, they should be used judiciously, as they can increase the total cost of your loan due to accruing interest. Always explore IDR plans first, as they often offer a more sustainable long-term solution by adjusting payments rather than merely postponing them.

Strategies for Accelerated Repayment

Beyond simply making your minimum payments, several strategies can help you pay off your student loans faster, saving you a significant amount in interest over the long run.

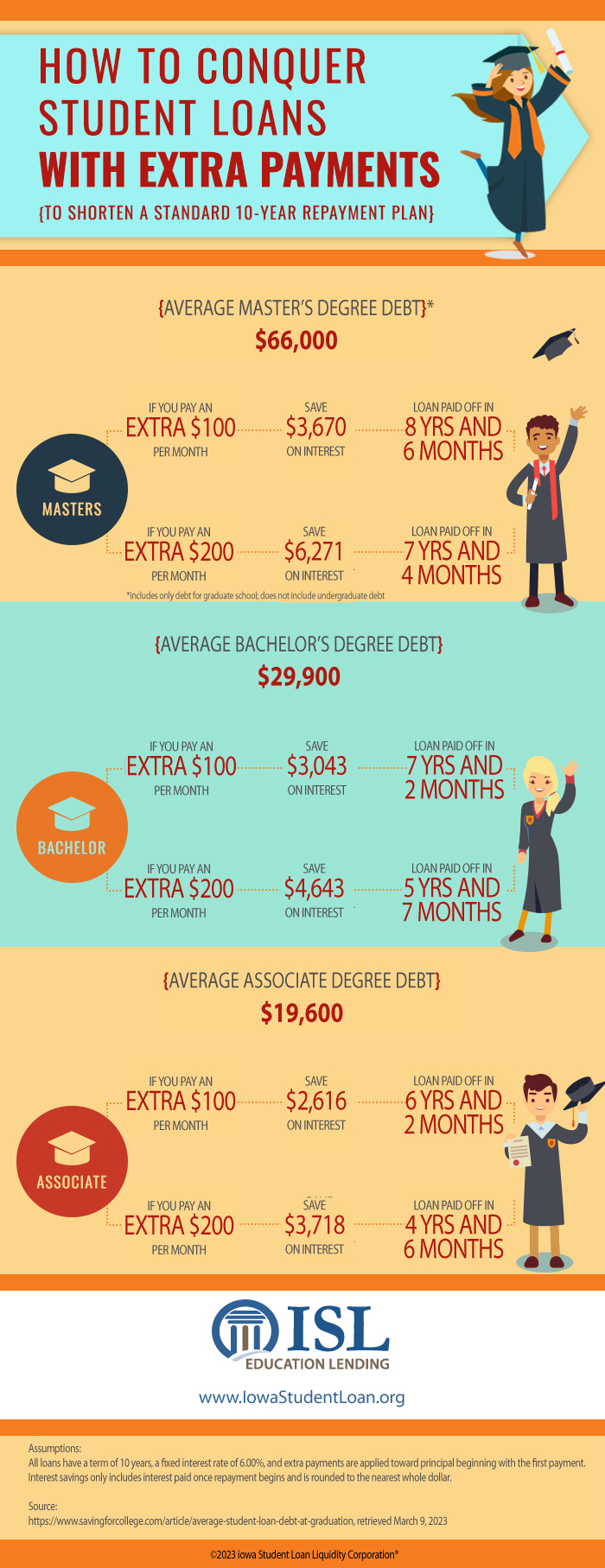

Making Extra Payments: The Power of Principal

One of the most effective ways to accelerate repayment is to pay more than your minimum monthly payment whenever possible. Even small extra contributions can make a substantial difference. When you make an extra payment, ensure you instruct your loan servicer to apply the additional amount directly to the principal balance of the loan with the highest interest rate. This reduces the principal on which interest accrues, leading to lower overall interest costs and a faster payoff date.

Consider implementing a “round up” strategy, where you pay an extra few dollars each month, or dedicating windfalls like tax refunds, bonuses, or gifts toward your student loan principal. The earlier you start making extra payments, the greater the impact due to the power of compounding.

Refinancing and Consolidation: When Do They Make Sense?

Loan consolidation is a federal program that allows you to combine multiple federal student loans into a single Direct Consolidation Loan. This results in one monthly payment and potentially access to additional repayment plans (like PSLF or some IDR plans). However, it does not typically lower your interest rate; instead, it uses a weighted average of your existing rates, rounded up to the nearest eighth of a percentage.

Refinancing, offered by private lenders, involves taking out a new private loan to pay off your existing federal and/or private student loans. The primary goal of refinancing is to secure a lower interest rate, which can significantly reduce your monthly payments and/or the total cost of your loan. This is most beneficial for borrowers with stable income, excellent credit, and a low debt-to-income ratio. However, refinancing federal loans into a private loan means forfeiting federal borrower protections, such as IDR plans, deferment options, and access to federal forgiveness programs. This trade-off must be carefully considered based on your financial stability and future career plans.

The Debt Snowball vs. Debt Avalanche Method

Two popular strategies for tackling multiple debts are the debt snowball and debt avalanche methods:

- Debt Snowball: You focus on paying off your smallest loan first while making minimum payments on all others. Once the smallest loan is paid off, you take the money you were paying on that loan and add it to the payment of your next smallest loan. This method builds psychological momentum as you quickly knock out smaller debts.

- Debt Avalanche: You prioritize paying off the loan with the highest interest rate first, while making minimum payments on all other loans. Once the highest-interest loan is paid off, you move on to the next highest. This method saves you the most money in interest over time.

While the debt avalanche is mathematically superior, the debt snowball can be more motivating for some individuals. Choose the method that best aligns with your personality and financial discipline.

Leveraging Forgiveness and Assistance Programs

For certain professions or situations, specific programs can offer partial or full student loan forgiveness, significantly alleviating your debt burden.

Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is designed to forgive the remaining balance on Direct Loans after you’ve made 120 qualifying monthly payments while working full-time for a qualifying employer. Qualifying employers include government organizations (federal, state, local, or tribal) and eligible non-profit organizations. Payments must be made under a qualifying IDR plan. PSLF can be a life-changing benefit for those committed to public service, but strict requirements must be met, and it’s essential to track your eligibility carefully from the outset.

Teacher Loan Forgiveness and Other Specific Programs

Beyond PSLF, other loan forgiveness programs cater to specific professions:

- Teacher Loan Forgiveness: Forgives up to $17,500 of Direct Subsidized and Unsubsidized Loans for eligible teachers who work full-time for five consecutive years in low-income schools or educational service agencies.

- Perkins Loan Cancellation/Discharge: Available for various public service occupations, including teachers, nurses, law enforcement officers, and others, with the percentage of the loan discharged increasing over time.

- Loan Repayment Assistance Programs (LRAPs): Many states and specific organizations offer LRAPs for professionals in high-need areas like healthcare (doctors, nurses), law (public defenders), and certain scientific fields. These programs often provide funds to help cover a portion of your student loan payments in exchange for a service commitment.

Researching these niche programs is crucial if your career path aligns with their criteria, as they can offer substantial relief.

Employer-Assisted Repayment Benefits

An increasing number of companies are recognizing the burden of student loan debt and offering employer-assisted repayment benefits as part of their compensation packages. These benefits can range from direct contributions to your loan principal, matching programs, or even access to financial wellness tools and advice. When job searching, inquire about such benefits, especially if you have significant student loan debt. For current employees, it might be worth discussing with your HR department whether such programs are under consideration.

Building a Sustainable Financial Future

Paying off student loans is not a singular event but an ongoing process that integrates into your broader financial life. Strategic planning ensures you not only conquer your debt but also build a strong foundation for future financial goals.

Budgeting for Student Loan Payments

A robust budget is the cornerstone of effective debt management. It helps you understand where your money is going and identify areas where you can optimize spending to free up funds for extra loan payments.

- Track Your Income and Expenses: Use budgeting apps, spreadsheets, or pen and paper to meticulously record all money coming in and going out.

- Categorize Spending: Identify fixed expenses (rent, utilities, loan payments) and variable expenses (groceries, entertainment).

- Identify Opportunities for Savings: Look for areas to cut back, even temporarily, such as reducing dining out, canceling unused subscriptions, or finding cheaper alternatives for daily necessities.

- Allocate Funds: Intentionally dedicate a portion of your budget towards your student loans, beyond the minimum payment.

A well-structured budget provides clarity and empowers you to make intentional financial decisions, turning abstract goals into actionable steps.

Balancing Debt Repayment with Other Financial Goals

While aggressively paying down student loans is often a wise move, it’s important not to do so at the expense of other critical financial goals. A balanced approach typically involves:

- Building an Emergency Fund: Aim for 3-6 months’ worth of essential living expenses in an easily accessible savings account. This safety net prevents you from going into further debt if unexpected costs arise.

- Saving for Retirement: Don’t delay saving for retirement, especially if your employer offers a 401(k) match. The power of compound interest works best over long periods, and missing out on an employer match is like leaving free money on the table.

- High-Interest Debt: Prioritize paying off any other high-interest debt (e.g., credit card debt) before accelerating student loan payments, as their interest rates are often significantly higher.

The optimal balance will depend on your individual circumstances, interest rates, and risk tolerance. It’s a continuous calibration between present debt relief and future financial security.

Seeking Professional Financial Guidance

Sometimes, the complexity of student loan repayment, combined with other financial decisions, warrants professional assistance. A certified financial planner (CFP) or a non-profit credit counselor can provide personalized advice tailored to your unique situation. They can help you:

- Analyze your entire financial picture, not just your student loans.

- Develop a comprehensive budget and debt repayment strategy.

- Understand the nuances of different loan programs and their implications.

- Balance student loan repayment with other financial goals like homeownership, retirement, and investing.

While there may be a cost associated with professional guidance, the long-term benefits of a clear, expert-backed financial plan can far outweigh the initial investment, potentially saving you thousands in interest and steering you towards financial success.

Paying for student loans is a marathon, not a sprint. By thoroughly understanding your loans, strategically choosing repayment plans, actively pursuing accelerated repayment methods, leveraging available assistance programs, and integrating debt management into a holistic financial plan, you can confidently navigate this significant financial hurdle and pave the way for a brighter financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.