The United States tax system operates on a “pay-as-you-go” principle. While traditional W-2 employees have their taxes automatically withheld from every paycheck, the landscape is significantly different for entrepreneurs, freelancers, investors, and those with diversified income streams. For these individuals, the responsibility of calculating and remitting taxes falls squarely on their own shoulders through estimated tax payments.

Understanding how to pay estimated taxes is not merely a matter of compliance; it is a fundamental pillar of sound financial management. Failing to navigate this process correctly can lead to unexpected liquidity crises, underpayment penalties, and unnecessary stress during the annual filing season. This guide provides a deep dive into the mechanics of estimated taxes, offering a roadmap for managing your fiscal obligations with professional precision.

Understanding the Fundamentals of Estimated Tax Payments

Estimated tax is the method used to pay tax on income that is not subject to withholding. This includes income from self-employment, interest, dividends, rent, alimony, and gains from the sale of assets. If you expect to owe at least $1,000 in tax after subtracting your withholding and credits, the IRS generally requires you to make quarterly payments.

Who is Required to Pay?

The requirement to pay estimated taxes applies to several categories of taxpayers. Primarily, it impacts sole proprietors, partners, and S corporation shareholders. If you are a freelancer or a “gig economy” worker, you are essentially a small business owner in the eyes of the IRS. Additionally, even if you have a full-time job with withholding, you might need to pay estimated taxes if you receive significant “unearned” income, such as dividends from a brokerage account or income from a rental property, which exceeds the amount your employer is already sending to the government.

The 1099 and Self-Employed Reality

For those receiving 1099 forms instead of W-2s, the gross amount received is not your “take-home” pay. Because no taxes are deducted at the source, you are responsible for both the employer and employee portions of Social Security and Medicare taxes, collectively known as self-employment tax. Understanding this distinction is vital for personal budgeting. Without a systematic approach to estimated payments, a successful year of business can quickly turn into a financial nightmare when the tax bill arrives in April.

The Safe Harbor Rules

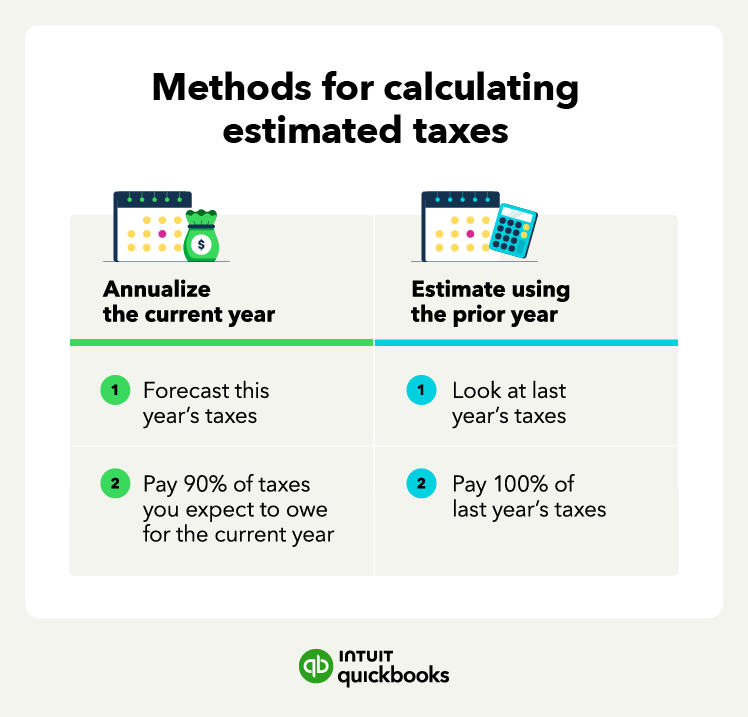

To avoid underpayment penalties, the IRS provides “Safe Harbor” guidelines. Generally, you will not face a penalty if you pay at least 90% of the tax shown on your current year’s return or 100% of the tax shown on your return for the prior year—whichever is smaller. For high-income earners (those with an adjusted gross income over $150,000), the prior-year safe harbor requirement increases to 110%. Leveraging these rules is a common strategy for financial stability, as it allows you to plan your payments based on known historical data rather than volatile future projections.

Calculating Your Estimated Tax Liability

Accurately calculating your estimated tax is the most challenging aspect of the process, particularly if your income fluctuates throughout the year. The goal is to get as close to your actual liability as possible to avoid over-leveraging your cash flow or falling short and incurring penalties.

Using Form 1040-ES

The IRS provides Form 1040-ES, “Estimated Tax for Individuals,” which includes a worksheet to help you estimate your taxes. This worksheet guides you through your expected adjusted gross income, taxable income, taxes, deductions, and credits. To fill this out accurately, you should have your tax return from the previous year handy to use as a baseline. If your financial situation has changed significantly—for instance, if you’ve scaled your business or started a new side hustle—you will need to adjust these figures to reflect your new reality.

Factoring in Self-Employment Tax

One of the most common mistakes made by those new to the “Money” niche of self-employment is forgetting the self-employment tax. This tax rate is 15.3%, consisting of 12.4% for social security and 2.9% for Medicare. When calculating your estimated payments, you must include this amount in addition to your standard income tax. However, you are allowed to deduct the employer-equivalent portion of your self-employment tax (7.65%) in figuring your adjusted gross income, which provides a slight buffer.

Deductions and Credits: Reducing the Burden

Effective tax management involves more than just paying; it involves optimizing. When calculating your quarterly payments, don’t forget to account for potential deductions and credits. If you work from a home office, use your vehicle for business, or have significant health insurance premiums as a self-employed individual, these deductions reduce your taxable income. Similarly, if you are eligible for the Child Tax Credit or the Earned Income Tax Credit, these should be factored into your worksheet to ensure you aren’t overpaying the government and losing out on the opportunity to invest that capital elsewhere.

Important Deadlines and the Payment Calendar

The IRS does not wait until the end of the year to collect. They expect payments in four distinct installments. It is a common misconception that these are exactly three months apart; in reality, the windows vary slightly.

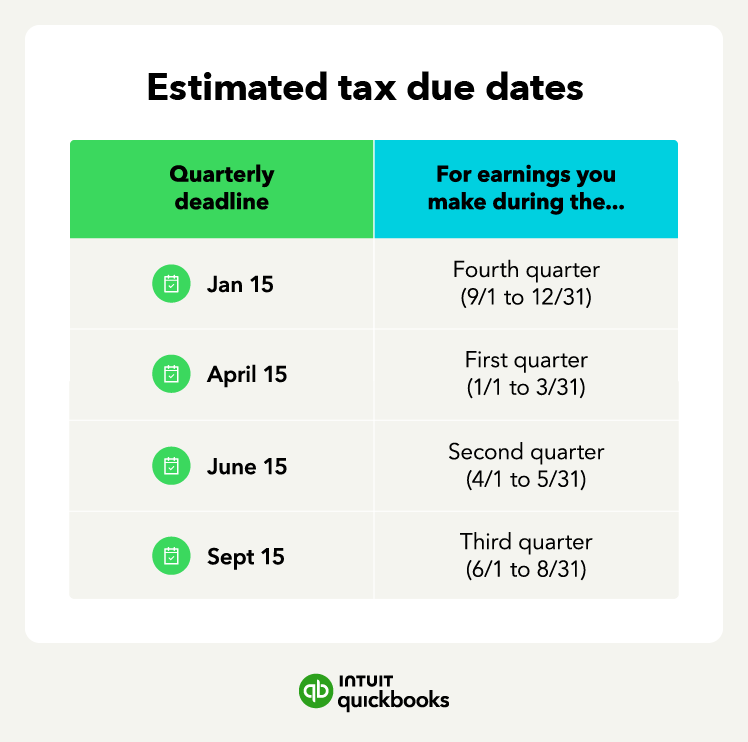

The Four Critical Dates

For a standard calendar-year taxpayer, the deadlines are:

- April 15: Covers income earned from January 1 to March 31.

- June 15: Covers income earned from April 1 to May 31.

- September 15: Covers income earned from June 1 to August 31.

- January 15 (of the following year): Covers income earned from September 1 to December 31.

If these dates fall on a weekend or a legal holiday, the deadline is pushed to the next business day. Marking these dates on your financial calendar is non-negotiable for anyone serious about managing their business finance.

Consequences of Missing a Deadline

Missing a deadline or underpaying can result in an underpayment penalty. The IRS calculates this penalty based on the amount of the underpayment and how long it remained unpaid. Even if you are due a refund when you finally file your annual return, you can still be hit with a penalty for not paying enough during a specific quarter. This is why “lumping” all your payments into the final January deadline is rarely a sound strategy; the IRS wants the money as you earn it.

How to Submit Your Payments: Methods and Platforms

The modern financial landscape has made remitting taxes significantly easier than it was in the era of paper checks and snail mail. There are several secure digital platforms designed to handle these transactions efficiently.

IRS Direct Pay and EFTPS

The most straightforward method for individuals is IRS Direct Pay. This service allows you to pay directly from your checking or savings account with no associated fees. You receive an immediate confirmation number, which is essential for your records. For business owners or those with more complex needs, the Electronic Federal Tax Payment System (EFTPS) is a more robust option. While it requires a prior registration process and a PIN, it allows you to schedule payments up to 365 days in advance, ensuring you never miss a deadline due to forgetfulness.

Payment via Mail or Mobile App

For those who prefer traditional methods, you can still mail a check or money order along with the payment voucher found in Form 1040-ES. However, this is generally discouraged due to the potential for mail delays or loss. Alternatively, the IRS2Go mobile app provides a convenient way to make payments from a smartphone, linking directly to the Direct Pay or credit/debit card payment processors. Note that paying via credit card will incur processing fees from the third-party providers, which can eat into your margins.

Keeping Meticulous Records

Regardless of the method you choose, record-keeping is vital. Create a dedicated folder (digital or physical) for each tax year. Save your confirmation numbers, bank statements showing the withdrawal, and the worksheets you used to calculate the payment. When you sit down with your CPA or use tax software in April, having an organized list of exactly how much you paid and when will save hours of frustration and ensure you receive proper credit for the taxes you’ve already remitted.

Strategies for Managing Cash Flow for Taxes

For many, the struggle isn’t knowing how to pay, but having the money available when the deadline arrives. Integrating tax savings into your daily financial habits is the hallmark of a savvy investor or business owner.

The “Percentage” Method

The most effective way to manage estimated taxes is to treat the government as a silent partner who takes a cut of every dollar you earn. A common strategy is to set aside a fixed percentage of every payment you receive—typically between 25% and 30%—into a separate bank account. By doing this the moment the money hits your business account, you ensure that you never “feel” like that money was yours to spend in the first place.

High-Yield Savings Accounts for Tax Reserves

Don’t let your tax reserves sit in a zero-interest checking account. Since you will be holding this money for three to twelve months, place it in a high-yield savings account (HYSA). While it won’t make you wealthy, earning 4% or 5% APY on your tax money allows you to offset some of your eventual tax liability. It turns a liability into a small, temporary asset.

Adjusting as Your Income Fluctuates

The “Money” world is rarely static. If you have a breakthrough quarter where your income doubles, your previous estimates will be insufficient. Conversely, if you lose a major client or face an economic downturn, you shouldn’t continue paying high estimates that drain your necessary operating capital. Review your year-to-date income at least two weeks before every quarterly deadline. This proactive adjustment ensures your payments remain aligned with your actual earnings, protecting your cash flow and maintaining your financial health throughout the year.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.