Inflation is often described by economists as the “silent thief.” It is a persistent rise in the general level of prices for goods and services over a period of time, which subsequently erodes the purchasing power of your money. For the individual investor, the business owner, or the household budgeter, understanding how to calculate inflation is not merely an academic exercise; it is a fundamental pillar of financial literacy. When you know how to measure the rate at which your money is losing value, you can make more informed decisions regarding your savings, your investments, and your long-term financial security.

To navigate the complexities of a modern economy, one must look beyond the headlines and understand the mechanics of the Consumer Price Index (CPI) and the mathematical formulas used to derive inflation rates. This guide will walk you through the essential steps of calculating inflation, the various metrics used by financial institutions, and how these figures directly impact your personal wealth.

Understanding the Foundation: The Consumer Price Index (CPI)

Before you can calculate the rate of inflation, you must understand the data source that serves as the primary benchmark for price changes: the Consumer Price Index (CPI). Produced by government agencies—such as the Bureau of Labor Statistics (BLS) in the United States—the CPI tracks the change in prices paid by urban consumers for a representative “market basket” of goods and services.

The Market Basket Concept

The “market basket” is a theoretical collection of items that represent the average spending habits of a typical household. This includes thousands of items categorized into groups such as food and beverages, housing, apparel, transportation, medical care, recreation, and education. To calculate inflation accurately, economists track the prices of these specific items across various locations and retailers over time. By keeping the “basket” relatively consistent, they can isolate price changes from changes in consumer behavior.

Weighting and Index Points

Not every item in the basket carries the same weight. For instance, a 10% increase in the price of housing has a much more significant impact on the average consumer’s budget than a 10% increase in the price of postage stamps. Therefore, the CPI is a weighted index. Each category is assigned a percentage of the total index based on how much the average consumer spends on it. These prices are then converted into “index points” relative to a base period. For example, if the base period (usually a specific year or range of years) is set at 100, and the current index is 280, it indicates that prices have risen 180% since that base period.

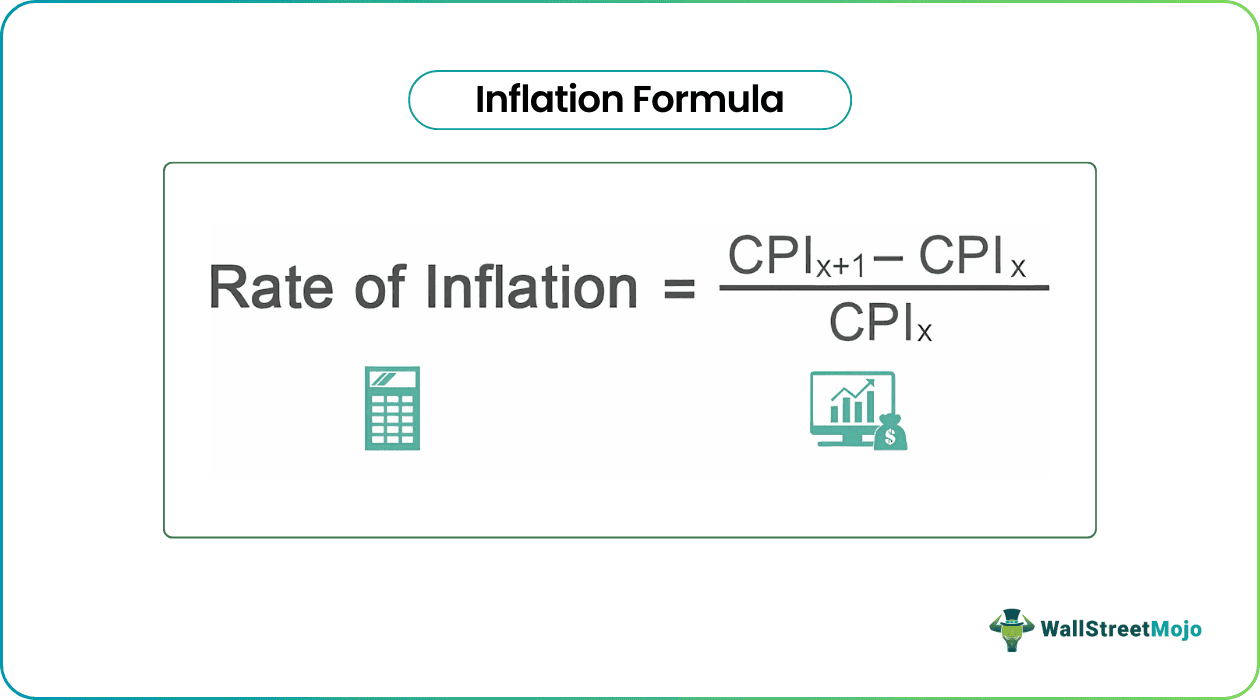

The Mathematical Formula: How to Calculate Inflation Manually

Calculating the inflation rate is a straightforward process once you have the relevant CPI data. The most common measurement is the “year-over-year” inflation rate, which compares the price level of a specific month to the same month in the previous year.

The Percentage Change Equation

The formula for calculating the inflation rate is the standard percentage change formula:

Inflation Rate = ((CPI x + 1 – CPI x) / CPI x) * 100

In this formula:

- CPI x + 1 is the CPI for the current period (the later date).

- CPI x is the CPI for the prior period (the earlier date).

By subtracting the old index from the new index, you find the “point change.” You then divide that change by the original index and multiply by 100 to express the result as a percentage.

A Practical Walkthrough

Let’s look at a hypothetical example. Suppose you want to calculate the annual inflation rate for a specific year.

- Identify the Data: Imagine the CPI in January of Year 1 was 250.

- Identify the Current Data: Imagine the CPI in January of Year 2 was 265.

- Subtract: 265 – 250 = 15. This is the point increase in the cost of living.

- Divide: 15 / 250 = 0.06.

- Multiply: 0.06 * 100 = 6%.

In this scenario, the annual inflation rate is 6%. This means that, on average, a basket of goods that cost $100 in Year 1 would cost $106 in Year 2. While 6% might seem small in isolation, when compounded over several years, it can drastically alter your financial landscape.

Variations of Inflation Measurement

While the standard CPI is the most widely cited figure, it is not the only way to measure inflation. Depending on your financial goals—whether you are a day trader, a long-term bond investor, or a corporate strategist—different metrics may provide more relevant insights.

Core Inflation vs. Headline Inflation

When you hear inflation numbers on the news, they are often referring to “Headline Inflation.” This includes every item in the CPI basket. However, economists and the Federal Reserve often focus on “Core Inflation.” Core inflation removes two highly volatile categories: food and energy. Because gas prices and grocery costs can fluctuate wildly due to geopolitical events or weather patterns, stripping them away allows analysts to see the underlying, long-term trend of price increases in the broader economy. For personal financial planning, Headline Inflation is what you “feel” at the pump, but Core Inflation is often a better predictor of where interest rates are headed.

The Personal Consumption Expenditures (PCE) Price Index

While the CPI is the most famous, the Federal Reserve actually prefers the PCE Price Index when making decisions about interest rates. The PCE is slightly different from the CPI because it tracks what businesses are selling rather than just what consumers say they are buying. It also accounts for “substitution bias”—the idea that if the price of beef goes up, consumers will naturally buy more chicken. Because the PCE adjusts for these shifts in consumer behavior, it is often considered a more dynamic and accurate reflection of the true cost of living.

The Producer Price Index (PPI)

For those involved in business finance or equity investing, the Producer Price Index (PPI) is a critical “leading indicator.” While the CPI measures inflation from the consumer’s perspective, the PPI measures inflation from the perspective of the industries that produce goods. When the costs of raw materials like steel, lumber, or fuel rise for manufacturers, those costs are eventually passed down to the consumer. Therefore, a spike in the PPI often signals that a spike in the CPI is only a few months away.

The Financial Impact: Why These Calculations Matter for Your Money

Understanding how to calculate inflation is the first step; understanding how to apply that knowledge to your wealth management is the second. Inflation is the primary benchmark against which all investment returns must be measured.

Calculating Real vs. Nominal Returns

In the world of personal finance, there is a massive difference between “nominal” returns and “real” returns.

- Nominal Return: The actual percentage increase in your account balance.

- Real Return: The nominal return minus the inflation rate.

If you have a high-yield savings account earning 4% interest, but inflation is running at 5%, your “real” return is -1%. Even though your bank balance is growing, your purchasing power is actually shrinking. To build true wealth, your investment portfolio must consistently generate returns that exceed the rate of inflation. This is why “parking” all your cash in a standard savings account is often a losing strategy over the long term.

Inflation and Fixed-Income Investments

Inflation is the natural enemy of the bond market. When you buy a bond, you are essentially lending money in exchange for fixed interest payments. If inflation rises significantly after you buy the bond, those fixed payments become less valuable. This is why, when inflation expectations rise, bond prices typically fall. For retirees living on a fixed income, calculating inflation is vital for determining whether their current draw-down rate is sustainable or if they are at risk of outliving their money.

Practical Tools and Strategies for Navigating Inflation

Living in an inflationary environment requires a proactive approach to money management. You cannot control the national inflation rate, but you can control how you calculate its impact on your specific lifestyle and how you position your assets to mitigate the damage.

Using Inflation Calculators for Long-Term Planning

Most major financial websites and government portals (like the BLS) offer “Inflation Calculators.” These tools allow you to see what a dollar amount from a past year is worth in today’s currency. This is incredibly useful for retirement planning. If you believe you need $5,000 a month to live comfortably today, and you plan to retire in 20 years, an inflation calculator (assuming a 3% average inflation rate) will show you that you actually need nearly $9,000 a month in 2044 to maintain that same standard of living.

Hedging Your Portfolio Against Inflation

Once you have mastered the calculation of inflation, you can begin to choose assets that serve as “hedges.” Traditionally, these include:

- Treasury Inflation-Protected Securities (TIPS): These are government bonds where the principal increases with inflation (measured by the CPI).

- Real Estate: Property values and rents often rise in tandem with inflation.

- Equities: While volatile, many companies have “pricing power,” meaning they can raise their prices to keep up with rising costs, protecting their profit margins and your dividends.

- Commodities: Gold, oil, and agricultural products often see price appreciation when the value of fiat currency declines.

In conclusion, calculating inflation is more than just a mathematical formula; it is a lens through which you must view your entire financial life. By understanding the CPI, mastering the percentage change formula, and distinguishing between nominal and real returns, you empower yourself to make financial decisions that preserve your hard-earned wealth. In an era of economic uncertainty, the ability to quantify the “silent thief” is your best defense in maintaining your purchasing power and ensuring your future financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.