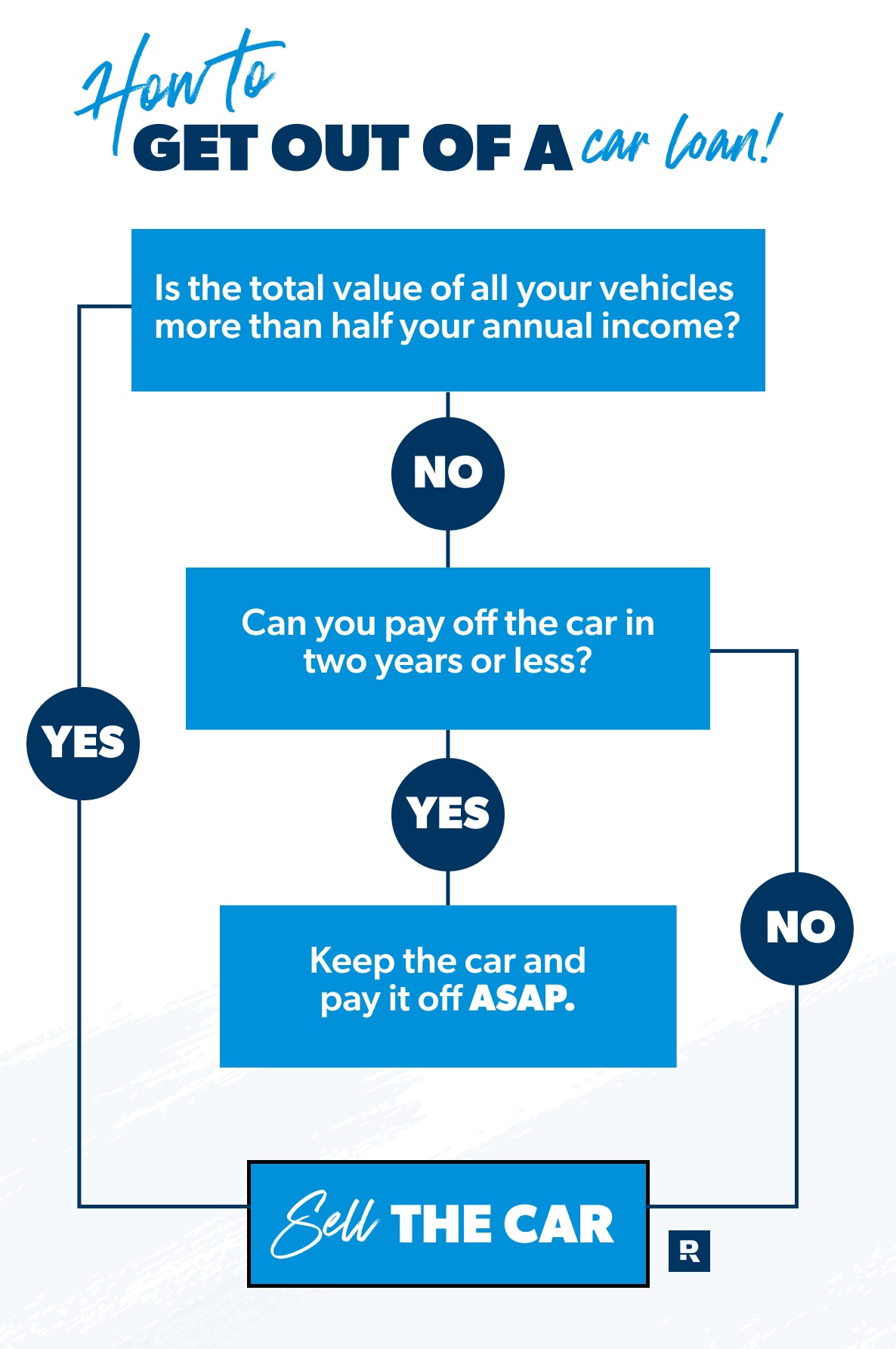

For many households, the monthly auto loan payment is the second-largest line item in the budget, trailing only housing costs. While a reliable vehicle is often a necessity for employment and daily life, the financial burden of a high-interest or long-term car loan can severely hamper your ability to save, invest, or achieve liquidity. Whether you are facing a sudden financial hardship, looking to aggressively pay down debt, or simply realizing that your “dream car” has become a “budget nightmare,” there are several strategic pathways to exit a car payment.

Getting out of a car payment requires a blend of market timing, credit management, and occasionally, a hard look at one’s lifestyle. This guide explores the professional financial strategies available to consumers looking to liberate their cash flow from the constraints of auto debt.

1. Liquidation Strategies: Selling Your Way to Solvency

The most direct way to eliminate a car payment is to remove the debt by selling the underlying asset. However, the success of this strategy depends entirely on the “equity” you hold in the vehicle—the difference between the car’s current market value and your remaining loan balance.

Selling to a Private Party for Maximum Return

If your goal is to cover the entirety of your loan balance, selling to a private party is almost always more lucrative than a dealership trade-in. Dealerships must account for overhead and profit margins, meaning they will offer “wholesale” value. By selling privately, you can often command a “retail” price.

To execute this, you must first obtain a payoff quote from your lender. If the private sale price exceeds the loan balance, the buyer’s funds will pay off the bank, the lien will be released, and you keep the remaining profit. Note that this process requires coordination with your lender to ensure a smooth title transfer, which may involve meeting the buyer at a local bank branch.

Utilizing Instant Cash Offers and Tech-Enabled Dealers

In recent years, the rise of digital automotive platforms has simplified the exit strategy. Companies that provide instant cash offers allow you to bypass the hassle of private listings. While these offers might be slightly lower than a private sale, they provide a guaranteed “out” and often handle the payoff paperwork directly with your lender. This is an ideal route for those who prioritize time-efficiency and professional handling of the lien release.

Navigating the Challenge of Negative Equity

“Being underwater” or having “negative equity” occurs when you owe more on the loan than the car is worth. This is the most common barrier to getting out of a car payment. To sell a vehicle in this situation, you must bridge the gap out of pocket. If you do not have the cash on hand, you might consider taking out a low-interest personal loan to cover the “equity gap.” While this replaces one debt with another, an unsecured personal loan for $3,000 to $5,000 is significantly more manageable than a $30,000 car loan with associated insurance and maintenance costs.

2. Structural Adjustments: Refinancing and Loan Modification

If selling the vehicle isn’t an option because you need the transportation, the next logical step is to change the terms of the debt itself. Financial restructuring can lower your monthly obligation, even if it doesn’t eliminate the debt entirely in the short term.

Refinancing for a Lower Interest Rate

Interest rates fluctuate based on market conditions and your personal credit score. If your credit has improved since you first signed your auto loan, or if you originally accepted a high-interest “dealer-arranged” loan, you are likely overpaying.

By refinancing through a credit union or an online lender, you can secure a lower Annual Percentage Rate (APR). A reduction of just 3% or 4% can save dozens, if not hundreds, of dollars per month. This strategy keeps you in the car but frees up immediate cash flow for other financial goals, such as building an emergency fund or investing in a diversified portfolio.

Extending the Loan Term: Use with Caution

Extending your loan term (e.g., moving from 36 months remaining to 60 months) will drastically lower your monthly payment. From a strict personal finance perspective, this is a “defensive” move. While it provides immediate breathing room in your monthly budget, it increases the total interest paid over the life of the loan and keeps you in debt longer. Professional financial advisors typically recommend this only as a temporary measure to avoid default during a period of reduced income.

Seeking Formal Hardship Programs

If your inability to make payments is due to a temporary setback, such as a job loss or medical emergency, many lenders offer “forbearance” or “deferment” programs. These allow you to skip one or two payments, which are then tacked onto the end of the loan. While this doesn’t “get you out” of the payment permanently, it prevents repossession and credit damage while you reorganize your finances.

3. Specialized Exit Paths: Leases and Legal Recourse

Not every car payment stems from a traditional loan. Leasing presents its own set of challenges, and some vehicles carry inherent defects that provide a legal path to exit the contract.

Executing a Lease Transfer

Leases are notoriously difficult to break, often requiring the payment of all remaining monthly installments as a penalty. However, many lease contracts allow for a “lease assumption” or “transfer.” Platforms such as Swapalease or LeaseTrader connect people looking to exit their leases with individuals looking for a short-term vehicle commitment. By transferring the lease to a new person, you are legally absolved of the monthly payment and the eventual return of the vehicle, usually for a small administrative fee.

Investigating Lemon Laws and Rescission Rights

If you are trying to get out of a car payment because the vehicle is constantly in the shop, you may have legal recourse. “Lemon Laws” vary by state but generally apply to new vehicles that have a recurring, significant defect that the manufacturer cannot fix after a reasonable number of attempts. If a vehicle qualifies as a lemon, the manufacturer may be required to buy back the vehicle and cancel the loan.

Similarly, some states have “cooling-off periods” or specific rescission rights, though these are rare in the automotive industry and usually only apply if there was documented fraud during the sales process.

The Last Resort: Voluntary Surrender

A voluntary surrender (often called voluntary repossession) is when you give the car back to the lender because you can no longer afford the payments. While this stops the monthly billing, it is a catastrophic financial move. The lender will sell the car at auction—usually for a fraction of its value—and sue you for the “deficiency balance.” Furthermore, it will severely damage your credit score for seven years. This should only be considered when all other options, including bankruptcy consultation, have been exhausted.

4. Preventing the Debt Trap: Long-term Financial Planning

Once you have successfully exited a car payment, the goal shifts to ensuring you never find yourself in a similar position of financial strain. Professional wealth management emphasizes the importance of viewing vehicles as depreciating assets rather than investments.

Adhering to the 20/4/10 Rule

To maintain a healthy financial profile, many experts suggest the 20/4/10 rule for future purchases:

- 20% Down: Put at least 20% down to avoid falling into a negative equity position immediately.

- 4 Years: Finance the vehicle for no more than four years (48 months) to limit interest expenses.

- 10% Income: Ensure that your total transportation costs (loan, insurance, fuel, maintenance) do not exceed 10% of your gross monthly income.

The Power of the Sinking Fund

The most effective way to “get out” of car payments forever is to become your own lender. By redirecting the money you used to spend on a car payment into a dedicated “sinking fund” (a high-yield savings account), you can earn interest rather than paying it. When it comes time for your next vehicle, you can pay in cash. This not only eliminates the monthly payment but also provides significant leverage when negotiating the purchase price at a dealership.

Prioritizing Utility Over Status

In the realm of personal finance, the “opportunity cost” of a $600 monthly car payment is staggering. If that same $600 were invested in a low-cost index fund with an average 7% annual return, it would grow to over $100,000 in a decade. Choosing a reliable, used vehicle over a luxury model is often the difference between struggling with “lifestyle creep” and achieving genuine financial independence.

Conclusion

Getting out of a car payment is rarely a simple one-click process, but it is one of the most impactful moves you can make for your financial health. By assessing your equity, exploring refinancing options, or utilizing lease transfer markets, you can remove the weight of auto debt from your shoulders.

The ultimate goal of managing car debt is to move from a position of “owing” to a position of “owning.” Whether you sell your vehicle to downsize or refinance to accelerate your path to a zero balance, the result is the same: more of your hard-earned income stays in your pocket, where it can be put to work building your future instead of paying for your past.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.