Navigating the complexities of tax obligations can be a daunting task for individuals and businesses alike. The thought of owing the Internal Revenue Service (IRS) can trigger anxiety, but ignorance is not bliss when it comes to tax matters. Proactively understanding your financial standing with the IRS is crucial for maintaining fiscal health, avoiding penalties, and ensuring peace of mind. This comprehensive guide will illuminate the most effective and official pathways to determine if you owe the IRS, equipping you with the knowledge to address any potential liabilities responsibly and strategically.

Understanding Your Potential Tax Liabilities

Before diving into the methods of verification, it’s insightful to understand why an individual or entity might unexpectedly find themselves owing the IRS. Recognizing these common scenarios can help you contextualize your situation and inform your approach to resolution.

Common Reasons for Owing the IRS

Several factors can lead to an unexpected tax bill from the IRS. One of the most frequent culprits is under-withholding or underpaying estimated taxes. If you’re an employee, your W-4 form dictates how much tax is withheld from your paycheck. If this is not updated to reflect significant life changes (marriage, dependents, new income sources), you might not be paying enough throughout the year. For self-employed individuals, freelancers, or those with substantial investment income, estimated taxes are paid quarterly. Failing to accurately estimate and pay these can result in a significant tax liability at year-end.

Another common reason is missed deductions or credits. While less about owing the IRS and more about not getting money back, incorrect filing can lead to a higher tax burden than necessary. More directly, filing errors or failure to report all income can flag your return for review and ultimately lead to an assessment of additional taxes, interest, and penalties. The IRS receives income information from various sources (W-2s, 1099s, K-1s) and cross-references this with your filed return. Discrepancies often result in an IRS notice. Lastly, audit adjustments can significantly alter your tax picture, leading to new liabilities if the IRS finds unreported income or disallowed deductions during an examination.

The Importance of Proactive Monitoring

Waiting for an IRS notice to arrive in the mail is a reactive and potentially costly approach. Proactive monitoring of your tax situation throughout the year can prevent surprises and allow you to make adjustments as needed. This involves reviewing your pay stubs, tracking your income and expenses diligently, and periodically checking your tax withholding or estimated tax payments. Regular engagement with your financial records empowers you to anticipate potential shortfalls and take corrective action before the tax filing deadline, or certainly before the IRS sends you a bill. A proactive stance not only minimizes stress but also offers the opportunity to adjust your financial strategy to mitigate any emerging tax debt.

Official IRS Channels to Verify Your Tax Status

When suspicion arises or you simply wish to confirm your tax standing, the IRS provides several official, secure, and reliable methods to ascertain if you owe them money. Utilizing these channels ensures you receive accurate information directly from the source.

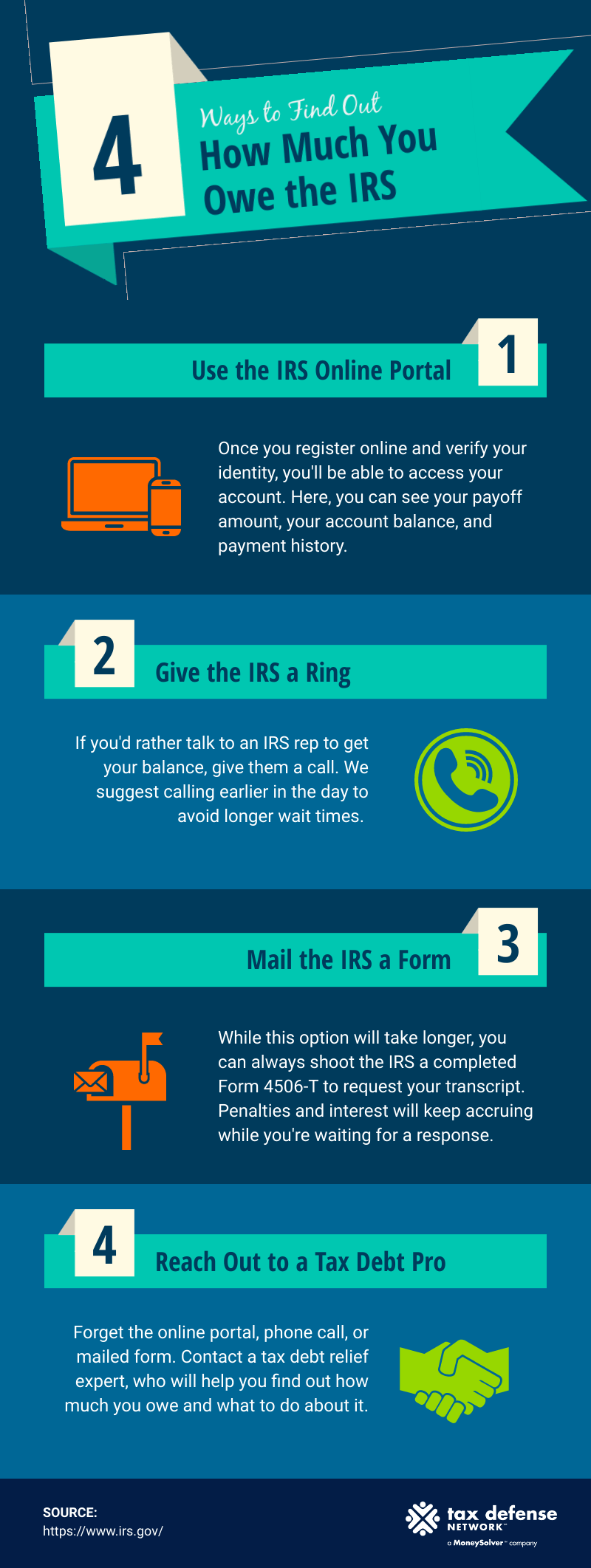

Utilizing Your IRS Online Account

One of the most convenient and immediate ways to check your tax account is through the IRS Online Account service. This secure portal provides taxpayers with direct access to a wealth of personal tax information. By creating or logging into your account, you can:

- View your balance: This shows the total amount you owe, including tax, penalties, and interest, for each tax year.

- Access payment history: See what payments you’ve made, including any estimated tax payments.

- Review tax records: Get access to various tax records, including adjusted gross income (AGI), which can be useful for verification purposes.

- Make payments: If you do owe, you can directly set up a payment plan or make a one-time payment through this portal.

Setting up an IRS Online Account requires a robust identity verification process to protect your sensitive financial information, but once established, it offers unparalleled convenience and transparency into your tax obligations.

Requesting Tax Transcripts

For a detailed breakdown of your tax filings and any associated liabilities, ordering your tax transcripts is an excellent option. An IRS tax transcript summarizes your tax return information and is often required for various financial applications, such as student loans or mortgages. Crucially, it also details any balance due or adjustments made to your account. There are several types of transcripts, including:

- Tax Return Transcript: Shows most line items from your original tax return (Form 1040, 1040A, or 1040EZ) as it was originally filed, along with any forms and schedules. It does not show changes made after you filed your original return.

- Tax Account Transcript: Provides basic data such as marital status, type of return filed, and payment history. It also shows changes made to your account after you filed your original return, including any balance due or overpayment. This is often the most relevant transcript for determining if you owe.

- Record of Account Transcript: Combines the tax return and tax account transcripts into one comprehensive document.

You can request transcripts online, by mail using Form 4506-T, or by phone. The online option, through the “Get Transcript Online” tool, typically allows immediate access for registered users.

Direct Communication with the IRS

Sometimes, the most direct approach is the best. If you have questions about a specific notice or believe there’s an error in your account, contacting the IRS directly via phone can provide clarification. The IRS offers dedicated phone lines for individuals and businesses, staffed by representatives who can access your account details and discuss any outstanding balances. Be prepared for potentially long wait times, especially during tax season. When you call, ensure you have your Social Security number or Employer Identification Number (EIN), previous tax returns, and any relevant notices handy for verification purposes. While less efficient than online tools for a simple balance check, direct communication is invaluable for resolving complex issues or understanding specific discrepancies.

Deciphering IRS Notices and Letters

Perhaps the most explicit way to find out if you owe the IRS is to receive an IRS notice or letter in the mail. The IRS uses a variety of notice numbers (e.g., CP2000, CP14, LT11) to communicate different issues, from proposed changes to your tax return based on income discrepancies (CP2000) to demand for payment (CP14). It is paramount to open and read these letters carefully. They are not spam; they contain critical information about your tax account, including:

- The reason for the notice.

- The tax year it pertains to.

- The amount you owe or the proposed adjustment.

- Instructions on what actions you need to take.

- A deadline for response.

Ignoring these notices can lead to increased penalties, interest, and eventually, enforced collection actions such as liens or levies. If you receive a notice and are unsure what it means, the IRS website has a tool to help you understand common notices, or you can consult with a tax professional.

What to Do When You Discover You Owe

Finding out you owe the IRS can be unsettling, but it’s a manageable situation with the right strategy. The key is to act promptly and understand your options rather than panicking or ignoring the problem.

Exploring Payment Options

The IRS prefers taxpayers pay their balances in full as soon as possible. If you can afford to pay the full amount due, doing so will prevent the accumulation of further penalties and interest. The IRS offers several convenient payment methods:

- Direct Pay: Make a payment directly from your checking or savings account for free.

- Debit Card, Credit Card, or Digital Wallet: Pay through a third-party payment processor, though a processing fee typically applies.

- Electronic Federal Tax Payment System (EFTPS): A free service for individuals and businesses to make federal tax payments electronically.

- Check or Money Order: Mail a payment with a payment voucher (Form 1040-V) to the IRS.

Always choose the method that best suits your financial situation and ensure you meet any deadlines specified in your IRS notice or on your tax return.

Setting Up Payment Plans and Agreements

If paying your tax debt in full immediately is not feasible, the IRS offers various payment arrangements to help taxpayers meet their obligations. These options include:

- Short-Term Payment Plan: You may be granted up to 180 days to pay your tax liability in full, although interest and penalties still apply.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This option is generally available when taxpayers are experiencing significant financial difficulties and cannot pay their full tax debt. The IRS assesses your ability to pay, income, expenses, and asset equity to determine if an OIC is appropriate.

- Installment Agreement: This allows you to make monthly payments for up to 72 months (6 years). An installment agreement is a more formal arrangement, and you will still accrue interest and potentially some penalties, though the failure-to-pay penalty may be reduced. Setting up an installment agreement is often an excellent way to avoid more severe collection actions. You can typically apply for an installment agreement online, by phone, or by mail.

Understanding which option is best for you depends on the amount you owe, your current financial situation, and your ability to commit to a payment schedule.

Seeking Professional Tax Assistance

For complex tax situations, significant tax debt, or if you feel overwhelmed by the process, seeking assistance from a qualified tax professional is highly recommended. Tax attorneys, Certified Public Accountants (CPAs), or Enrolled Agents (EAs) possess the expertise to:

- Accurately assess your tax situation.

- Help you understand IRS notices.

- Negotiate with the IRS on your behalf.

- Determine the best payment strategy (e.g., which payment plan is most appropriate, or if you qualify for an OIC).

- Represent you during an audit or appeal.

Their professional guidance can save you time, money, and stress, ensuring that your tax debt is handled in the most advantageous way possible within IRS guidelines.

Proactive Strategies to Avoid Future Debt

Preventing tax debt is always more desirable than resolving it. By implementing sound financial practices and staying vigilant, you can significantly reduce the likelihood of owing the IRS in the future.

Adjusting Withholding or Estimated Payments

One of the most effective preventive measures is to regularly review and adjust your tax withholding (for employees) or estimated tax payments (for the self-employed or those with other income sources).

- For employees: Use the IRS Tax Withholding Estimator tool on IRS.gov or complete a new Form W-4 to ensure the correct amount of tax is being withheld from your paycheck. Life events like marriage, divorce, having a child, or a change in income can significantly impact your tax liability, necessitating an adjustment to your W-4.

- For self-employed individuals and those with significant unearned income: Periodically review your income and expenses throughout the year. If your income projections change, adjust your quarterly estimated tax payments (Form 1040-ES) accordingly. This helps prevent a large tax bill at the end of the year and avoids potential underpayment penalties.

Meticulous Record-Keeping

Maintaining meticulous records of all income, expenses, deductions, and credits is fundamental to accurate tax reporting. Keep copies of W-2s, 1099s, bank statements, receipts for deductible expenses, investment statements, and any other financial documents relevant to your tax situation. Good record-keeping not only simplifies the tax filing process but also provides robust documentation if the IRS ever questions your return. Digital record-keeping solutions, cloud storage, and tax software can streamline this process, making it easier to track and organize your financial data year-round.

![]()

Annual Tax Review

Make it a habit to conduct an annual tax review, ideally before the end of the calendar year or early in the new year. This involves:

- Gathering all your financial documents.

- Reviewing your income and expenses.

- Identifying any potential changes in your tax situation (e.g., new investments, sale of property, major medical expenses).

- Consulting with a tax professional if your situation is complex or has undergone significant changes.

An annual review allows you to spot potential issues early, implement tax-saving strategies, and ensure that your next tax filing accurately reflects your financial reality, thereby minimizing the chances of owing the IRS unexpectedly.

In conclusion, understanding whether you owe the IRS and what to do about it is a critical aspect of personal and business financial management. By leveraging official IRS resources, acting decisively when an obligation is identified, and adopting proactive financial habits, you can navigate your tax responsibilities with confidence and maintain a healthy financial standing.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.