In an era of fluctuating interest rates and economic uncertainty, maximizing the return on your hard-earned money is more critical than ever. However, many savers overlook a silent predator that erodes their wealth over time: taxation. When you earn interest on a savings account, that interest is often treated as taxable income. Depending on your tax bracket, a significant portion of your gains could be redirected to the government rather than compounding in your account.

Understanding how to legally and strategically minimize or avoid tax on your savings is not just about “saving money”; it is about optimizing your entire financial ecosystem. By utilizing tax-advantaged accounts, understanding government allowances, and employing strategic asset location, you can ensure that more of your interest stays in your pocket. This guide explores the professional strategies used by high-net-worth individuals and savvy savers to protect their liquid assets from the taxman.

1. Leveraging Tax-Advantaged Savings Vehicles

The most effective way to avoid tax on savings interest is to move your capital into “tax-wrapped” environments. These are specialized accounts recognized by revenue services that provide a legal shield against income and capital gains taxes.

The Power of the Individual Savings Account (ISA) and Roth IRA

Depending on your jurisdiction, there are specific accounts designed to encourage personal saving by offering tax-free growth. In the United Kingdom, the Individual Savings Account (ISA) is the gold standard. Any interest earned on cash held within an ISA is entirely exempt from income tax, regardless of how much you earn. Currently, the annual allowance is generous, allowing individuals to shield a significant portion of their wealth every year.

In the United States, while traditional savings accounts are usually taxable, the Roth IRA (Individual Retirement Account) offers a similar principle for long-term savers. While primarily a retirement tool, the “backdoor” or “mega-backdoor” strategies allow high earners to place post-tax dollars into an environment where all future growth and withdrawals are tax-free. For those looking at shorter-term goals, certain Health Savings Accounts (HSAs) offer a “triple tax advantage”: contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are tax-free.

Retirement Accounts as a Tax Shield

While retirement accounts like the 401(k) or SIPP (Self-Invested Personal Pension) are often viewed as “locked” funds, they serve as the ultimate tax avoidance tool for savings. By contributing to these accounts, you often reduce your taxable income in the present year. The interest and dividends generated within these accounts compound without being subject to annual tax filings. For a long-term saver, the difference between a taxable savings account and a tax-deferred retirement account over 30 years can amount to hundreds of thousands of dollars in “saved” tax.

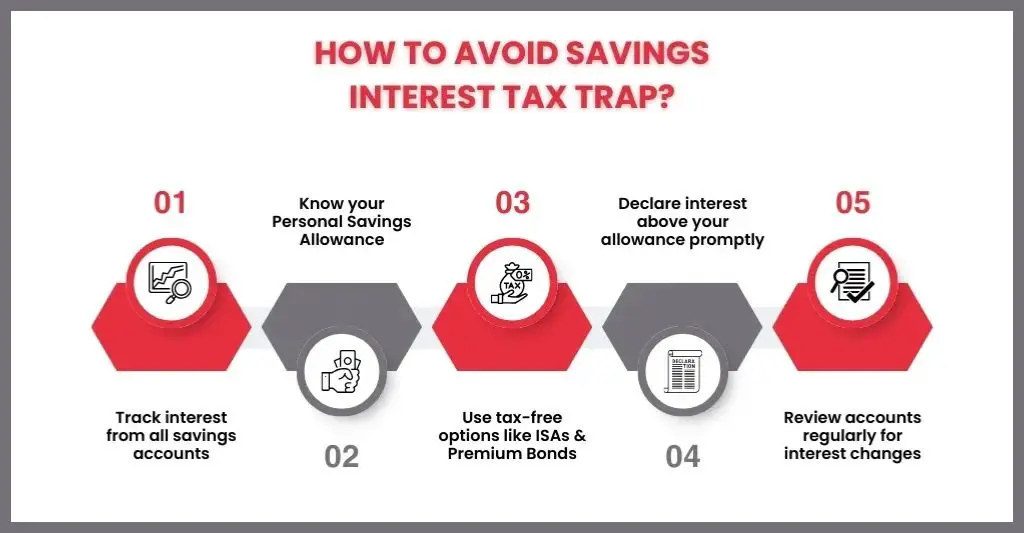

2. Navigating Personal Allowances and Thresholds

Most tax systems provide a “safety zone”—a specific amount of interest you can earn before you owe a single penny to the tax authorities. Understanding these thresholds is the first step in basic tax planning.

Maximizing the Personal Savings Allowance (PSA)

In many regions, the government grants a Personal Savings Allowance (PSA). For instance, in the UK, basic-rate taxpayers can earn up to £1,000 in savings interest tax-free, while higher-rate taxpayers have a £500 limit. If your savings are distributed correctly, you can ensure that your total interest stays just below these thresholds.

To manage this, savers must be proactive. If you have a large sum of cash, it may be more tax-efficient to split that cash between a high-yield taxable account (to utilize your PSA) and a tax-free ISA. Once you exceed your PSA, every dollar or pound of interest is taxed at your marginal rate, which could be as high as 40% or 45%. Monitoring your “interest income” throughout the year allows you to move funds into tax-sheltered vehicles before you cross the threshold.

The Role of the Starting Rate for Savings

Some tax systems offer a “starting rate” for savings specifically for those with lower overall incomes. If your earned income (from a job or pension) is below a certain level, your tax-free allowance for savings interest may actually increase significantly. This is particularly relevant for retirees or individuals transitioning between careers. By keeping your earned income low in specific years, you can “harvest” interest from your savings accounts without paying any tax, effectively utilizing the government’s lower-income provisions to your advantage.

3. Strategic Asset Location and Family Planning

Tax avoidance is often a “team sport.” If you are part of a household, you have more tools at your disposal than a single filer. Furthermore, where you put your money is just as important as how much you save.

Utilizing Spousal Transfers and Joint Accounts

One of the simplest yet most underutilized strategies is the transfer of assets between spouses or civil partners. If one partner is in a high tax bracket and the other is in a lower bracket (or has no income), it makes financial sense to hold the majority of the savings in the name of the lower-earning partner.

Most tax jurisdictions allow for the “inter-spousal transfer” of assets without triggering a tax event. By moving savings into the account of the spouse with the lower marginal tax rate, the household can maximize the use of two Personal Savings Allowances and ensure that any interest earned above the allowance is taxed at 20% rather than 40% or more. This simple administrative move can result in a significant “instant” return on investment by reducing the tax drag on the family’s liquid net worth.

Children’s Savings and Junior Wrappers

If you are saving for your children’s future, holding that money in your own name is a mistake. Most countries offer specific tax-free accounts for minors (such as the Junior ISA in the UK or 529 plans/UTMA accounts in the US). By placing the money in the child’s name within these wrappers, the interest is not attributed to the parents (subject to certain limits). This allows the capital to grow entirely tax-free until the child reaches adulthood. It is a powerful way to build a nest egg while ensuring the government doesn’t take a cut of the educational or housing fund you are building for the next generation.

4. Alternative Instruments: Bonds and Treasury Securities

Sometimes, the best way to avoid tax on a “savings account” is to stop using a traditional savings account altogether and look toward government-backed instruments that carry inherent tax advantages.

The Appeal of Municipal Bonds and Gilts

In the United States, Municipal Bonds (Munis) are a favorite of high-income earners. The interest earned on these bonds is often exempt from federal income tax and, in many cases, state and local taxes as well. While the “headline” interest rate on a muni bond might look lower than a high-yield savings account, the “tax-equivalent yield” is often much higher for those in top tax brackets.

Similarly, in other countries, specific government bonds (like low-coupon Gilts in the UK) can be highly tax-efficient. If a bond is purchased at a discount and held to maturity, the “gain” is often treated as a capital gain rather than interest. If that specific instrument is exempt from Capital Gains Tax (CGT), the saver effectively receives a high-interest return that is completely invisible to the tax authorities.

National Savings and Investment Products

Many governments offer their own branded savings products designed to encourage national thrift. In the UK, National Savings & Investments (NS&I) offers “Premium Bonds.” Instead of traditional interest, these bonds enter the holder into a monthly prize draw. Crucially, all winnings from Premium Bonds are 100% tax-free. For a saver who has already exhausted their ISA allowance and their Personal Savings Allowance, moving cash into Premium Bonds is a way to seek a return (in the form of prizes) that the taxman cannot touch.

5. The Long-Term Impact of Tax Efficiency

To truly appreciate the value of avoiding tax on savings, one must look at the math of compounding. If you have $100,000 in a savings account earning 5% interest, you earn $5,000 in year one. If you are in a 40% tax bracket, you lose $2,000 to taxes, leaving you with only $3,000 to reinvest.

The Drag of Annual Taxation

Over 20 years, that “tax drag” becomes a chasm. A tax-free account growing at 5% will grow significantly faster than a taxable account because the money that would have gone to taxes remains in the account to earn its own interest the following year. This is the “interest on interest on interest” effect. By avoiding tax, you aren’t just saving the 20% or 40% today; you are preserving the seed capital that generates future wealth.

Professional Financial Planning and Review

Tax laws are not static; they change with every new government budget. A strategy that worked last year may be less effective this year. Professional savers treat their tax-efficiency as a dynamic part of their portfolio. This involves an annual review of:

- Current interest rates vs. tax-free wrappers.

- Changes in personal income that might shift your tax bracket.

- New government savings products or allowance increases.

By staying informed and agile, you can ensure that your savings strategy remains optimized. Avoiding tax on your savings is not about complex loopholes; it is about using the system as it was intended—utilizing the incentives the government provides to reward those who plan for their financial future. In the quest for financial independence, reducing your tax bill is often the easiest and most “guaranteed” return you will ever find.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.