Understanding your potential Social Security benefits, especially as you approach retirement age, is a cornerstone of sound financial planning. While 65 has historically been a significant age associated with retirement, it’s crucial to recognize that Social Security retirement benefits are typically claimed at different ages. This article delves into the intricacies of Social Security retirement benefits, focusing on how your claiming age, specifically at 65, impacts your monthly payout, and what factors contribute to that calculation.

Understanding the Social Security Retirement Age

The age at which you begin receiving Social Security retirement benefits is a critical determinant of your monthly benefit amount. The system is designed to provide a reduced benefit if claimed before your “full retirement age” and an increased benefit if claimed after. Understanding these ages is fundamental to maximizing your Social Security income.

Full Retirement Age (FRA) and Its Significance

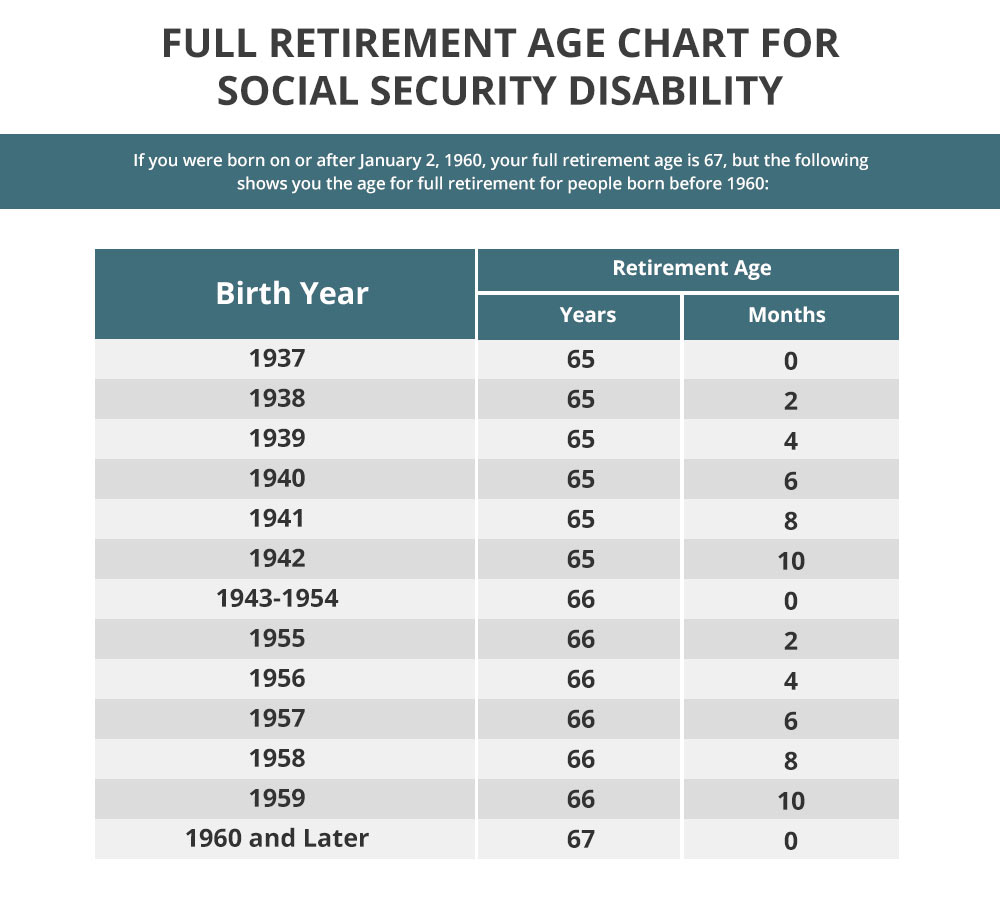

Your Full Retirement Age (FRA) is not a fixed number for everyone. It depends on your birth year. The Social Security Administration (SSA) has established a tiered system for FRA, gradually increasing it for those born in 1938 and later. For example, if you were born between 1943 and 1954, your FRA is 66. If you were born in 1960 or later, your FRA is 67.

The FRA is the age at which you are eligible to receive 100% of the Social Security benefit you have earned based on your lifetime earnings. Claiming benefits at your FRA is often considered the ideal scenario for most individuals, as it ensures you receive the full amount you are entitled to without any reductions.

Early Retirement: Claiming Before FRA

While the question specifically mentions 65, it’s important to note that 65 is before the Full Retirement Age for most individuals currently approaching retirement. If you choose to claim Social Security benefits before your FRA, your monthly benefit will be permanently reduced. This reduction is calculated based on the number of months you claim before your FRA.

For each month you claim early, your benefit is reduced by a small percentage. The maximum reduction occurs if you claim as early as possible, which is age 62. At age 62, your benefit is reduced by approximately 30% compared to what you would receive at your FRA.

Delayed Retirement: Claiming After FRA

Conversely, if you choose to delay claiming your Social Security benefits beyond your FRA, your monthly benefit will increase. For each month you delay beyond your FRA, up to age 70, your benefit is increased by a certain percentage. This is known as the “delayed retirement credits.” These credits are a powerful incentive to postpone claiming, especially if you are financially able to do so.

The maximum benefit you can receive from Social Security is achieved by waiting until age 70 to claim. After age 70, there are no further delayed retirement credits, so your benefit amount will not increase beyond that point.

Calculating Your Social Security Benefit

Your Social Security benefit is not an arbitrary number; it’s meticulously calculated based on your earnings history and the age at which you decide to claim benefits. The SSA uses a complex formula that aims to reflect your contributions to the system over your working life.

Your Average Indexed Monthly Earnings (AIME)

The foundation of your Social Security benefit calculation is your Average Indexed Monthly Earnings (AIME). This figure represents your average monthly earnings over your 35 highest-earning years, adjusted for inflation. The SSA “indexes” your past earnings to bring them up to current dollar values, ensuring that earnings from earlier in your career are given appropriate weight in the calculation.

The indexing process is crucial because it accounts for changes in wage levels over time. Without indexing, someone earning $10,000 in 1970 would have that amount considered in the calculation, which would be vastly different in purchasing power compared to $10,000 earned today. Indexing smooths out these discrepancies.

To calculate your AIME, the SSA takes your 35 highest-earning years (or fewer if you haven’t worked 35 years) and divides the total indexed earnings by 420 (the number of months in 35 years).

The Primary Insurance Amount (PIA)

Once your AIME is determined, it’s plugged into a progressive formula to arrive at your Primary Insurance Amount (PIA). The PIA is the benefit amount you would receive at your Full Retirement Age. This formula uses “bend points” that are adjusted annually by the SSA. Essentially, the formula applies a higher percentage to the lower portions of your AIME and a lower percentage to the higher portions. This progressive structure is designed to provide a more significant replacement rate of income for lower-earning workers.

For example, the formula might look something like this (using hypothetical bend points for illustration):

- 90% of the first $X of your AIME

- 32% of your AIME between $X and $Y

- 15% of your AIME above $Y

The exact bend points change each year, but the progressive nature remains constant. This means that two individuals with the same AIME will have the same PIA.

Adjustments Based on Claiming Age

Your PIA is your baseline benefit. However, as discussed earlier, your actual monthly benefit amount can be higher or lower depending on when you choose to claim.

If you claim at your FRA, you will receive your full PIA.

If you claim before your FRA (e.g., at 65, assuming your FRA is later), your PIA will be permanently reduced. For instance, if your FRA is 67, claiming at 65 means you are claiming 24 months early. This would result in a reduction of approximately 13.3% (24 months * 0.555% per month reduction).

If you claim after your FRA (e.g., at 66, assuming your FRA is 65), your PIA will be increased by delayed retirement credits.

The Impact of Claiming at Age 65

For many individuals, age 65 is a symbolic retirement age, often associated with Medicare eligibility. However, in the context of Social Security, claiming at 65 generally means claiming before your Full Retirement Age, leading to a reduced monthly benefit. The exact reduction depends on your specific Full Retirement Age.

Scenario 1: FRA is 67 (Born 1960 or later)

If your FRA is 67, claiming at age 65 means you are taking benefits 24 months earlier than your FRA. This early claiming will result in a reduction of approximately 13.3% of your PIA. So, if your PIA is $2,000, you would receive roughly $1,734 per month.

Scenario 2: FRA is 66 and 8 Months (Born 1957)

If your FRA is 66 and 8 months, claiming at age 65 means you are taking benefits 20 months earlier than your FRA. This would result in a reduction of approximately 11.1% of your PIA (20 months * 0.555% per month). If your PIA is $2,000, you would receive approximately $1,778 per month.

Scenario 3: FRA is 66 (Born 1943-1954)

If your FRA is 66, claiming at age 65 means you are taking benefits 12 months earlier than your FRA. This would result in a reduction of approximately 6.7% of your PIA (12 months * 0.555% per month). If your PIA is $2,000, you would receive approximately $1,866 per month.

These scenarios illustrate that claiming at 65 rarely means receiving your full earned benefit. The reduction is permanent, meaning you will receive this lower amount for the rest of your life.

Other Factors Influencing Your Benefit Amount

While your earnings history and claiming age are the primary drivers of your Social Security benefit, several other factors can influence the final amount you receive. These factors can either increase or decrease your monthly payout.

Cost-of-Living Adjustments (COLAs)

Social Security benefits are subject to Cost-of-Living Adjustments (COLAs) to help them keep pace with inflation. These adjustments are typically made annually, based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). A COLA increase means your monthly benefit will go up, preserving your purchasing power over time. While COLAs can’t undo the reduction from early claiming, they will apply to your reduced benefit amount, so your monthly check will still grow over time.

Spousal and Survivor Benefits

Your Social Security benefit is primarily based on your own earnings record. However, if you are married or have been married, you might be eligible for spousal or survivor benefits. A spousal benefit can be up to 50% of the primary earner’s benefit if claimed at their FRA. Survivor benefits can also be significant, allowing a surviving spouse to receive a portion of the deceased spouse’s benefit. These benefits can be claimed at age 60 (or earlier if disabled), but claiming before FRA will result in a reduction, similar to retirement benefits.

Maximum Earnings Subject to Social Security Taxes

There is an annual limit on the amount of earnings subject to Social Security taxes. This limit, known as the “taxable maximum,” changes each year. If your earnings exceed this limit, the portion above the maximum is not subject to Social Security taxes and does not count towards your AIME calculation. Therefore, individuals who consistently earn above the taxable maximum will likely receive a higher benefit than those with lower earnings, all other factors being equal.

Work Credits and Eligibility

To be eligible for Social Security retirement benefits, you need to earn a certain number of work credits. You can earn up to four credits per year. Generally, you need 40 credits (equivalent to about 10 years of work) to qualify for retirement benefits. If you have not accumulated enough work credits, you may not be eligible to receive benefits, or your benefit amount could be significantly lower if you have fewer than 35 years of earnings to include in your AIME calculation.

Making Informed Decisions for Your Retirement

Deciding when to claim Social Security is one of the most significant financial decisions you will make in retirement planning. While age 65 might seem like a natural retirement age, understanding how it interacts with Social Security’s structure is crucial for maximizing your income.

Utilize the Social Security Administration’s Tools

The Social Security Administration (SSA) offers a wealth of resources to help you estimate your benefits. Creating an account on the SSA’s website (ssa.gov) allows you to access your Social Security statement. This statement provides an estimate of your future benefits at different claiming ages, based on your earnings history. It’s an invaluable tool for personalized planning.

Consider Your Health and Longevity

Your personal health and family history of longevity should play a role in your claiming decision. If you have health concerns or a family history of shorter lifespans, claiming earlier might be more advantageous to ensure you receive benefits for a significant period. Conversely, if you are in good health and have a family history of living into your 80s or 90s, delaying benefits can lead to substantially higher monthly payments throughout your retirement.

Evaluate Your Financial Situation and Other Income Sources

Your overall financial picture is a critical factor. Do you have other retirement savings, such as a 401(k) or IRA? Do you anticipate any pension income? If you have substantial savings, you might be able to afford to delay Social Security, allowing your benefits to grow. This strategy can provide a higher, guaranteed income stream in your later retirement years, when other savings may be depleted. If you have limited savings, you might feel compelled to claim earlier to supplement your income.

Ultimately, there is no single “best” age to claim Social Security. The optimal strategy is highly personal and depends on a careful assessment of your individual circumstances, financial goals, and anticipated future needs. By understanding the mechanisms of Social Security benefits and their impact on your retirement income, you can make a more informed and confident decision about when to begin receiving your well-earned benefits.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.