The question of how much money is required for retirement is perhaps the most significant financial inquiry any individual will face. For many, retirement is no longer a fixed date on a calendar marked by a gold watch and a pension; instead, it is a specific financial state where your assets generate enough income to cover your cost of living indefinitely. Achieving this state requires more than just disciplined saving; it requires a sophisticated understanding of withdrawal rates, inflation, tax implications, and lifestyle design.

Calculating your “magic number” is a deeply personal process. While generic benchmarks provide a starting point, a truly robust retirement plan must account for your unique aspirations and the economic realities of the modern world. In this guide, we will break down the essential frameworks, calculation methods, and strategic considerations needed to determine exactly how much you need to secure your financial future.

Defining Your Retirement Lifestyle and Estimated Expenses

Before you can determine a total savings goal, you must first define what your life will look like in retirement. Your “number” is a direct reflection of your annual spending. If you plan to travel the world in luxury, your requirements will differ vastly from someone planning a quiet life in a low-cost rural area.

Estimating Post-Retirement Spending

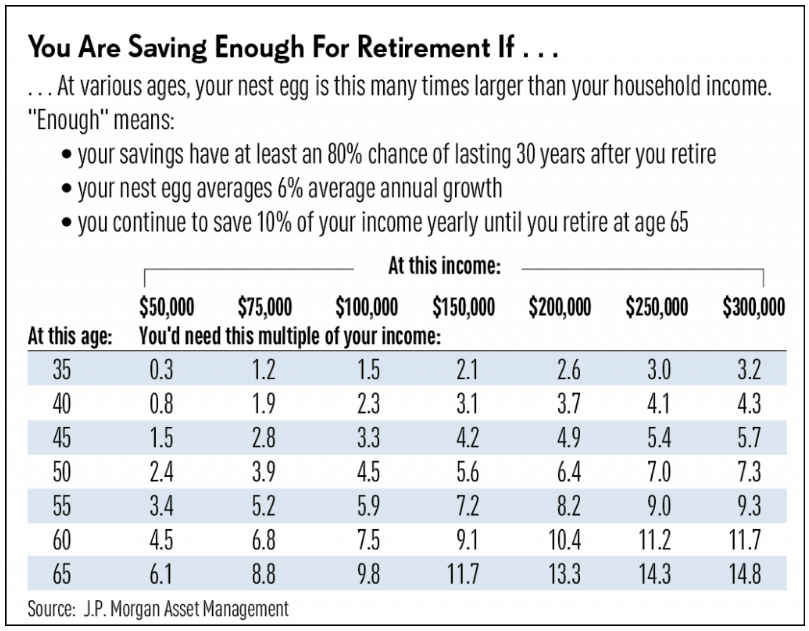

A common starting point is the “Income Replacement Rule,” which suggests you will need approximately 70% to 80% of your pre-retirement annual income to maintain your standard of living. The logic is that once you stop working, you no longer need to save for retirement, your payroll taxes decrease, and work-related expenses (like commuting or professional wardrobes) disappear.

However, this rule can be misleading. Many retirees find that their spending actually increases in the early years of retirement—often called the “Go-Go” years—as they pursue travel and hobbies they previously didn’t have time for. To get a precise figure, you should create a mock budget that categorizes “must-have” expenses (housing, healthcare, food) versus “nice-to-have” expenses (travel, entertainment, gifting).

The Impact of Inflation on Purchasing Power

One of the greatest threats to a retirement nest egg is inflation. Even at a modest 3% annual inflation rate, the purchasing power of a dollar is cut in half roughly every 24 years. This means if you need $60,000 to live comfortably today, you may need over $100,000 for that same lifestyle twenty years from now.

When calculating your retirement needs, you cannot simply look at today’s prices. You must project your expenses into the future. This is why investing in assets that historically outpace inflation, such as equities and real estate, is crucial. A “cash-only” retirement strategy is often a recipe for a diminishing standard of living over time.

Calculating the Magic Number: Common Frameworks

Once you have a handle on your projected annual expenses, you can use established financial frameworks to work backward toward a total portfolio goal.

The 4% Rule and the 25x Multiplier

The most famous benchmark in retirement planning is the “4% Rule,” derived from the Trinity Study. This rule suggests that if you withdraw 4% of your total portfolio in the first year of retirement and adjust that amount for inflation every year thereafter, your money has a very high probability of lasting at least 30 years.

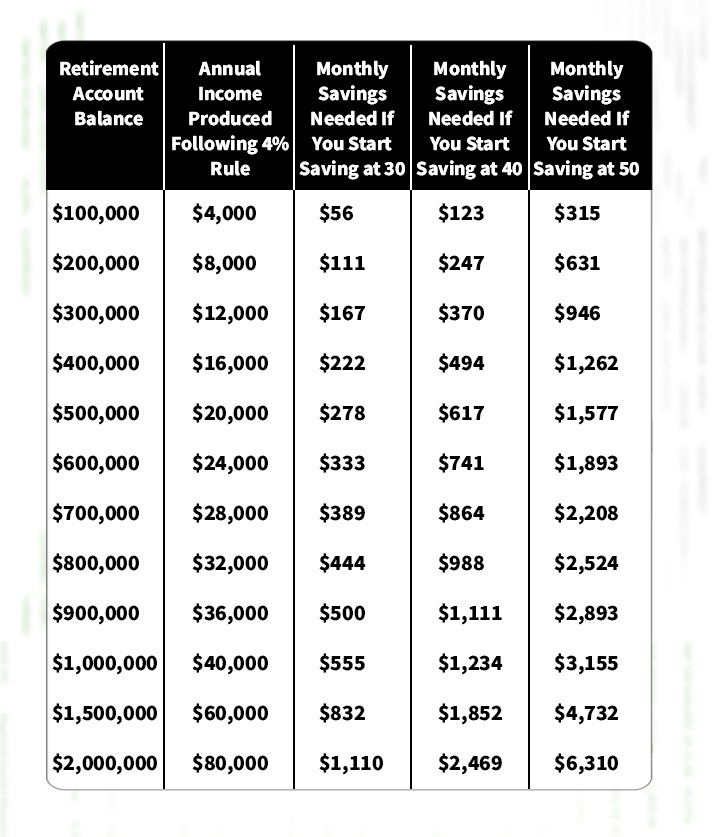

To use this rule to find your target number, you simply take your expected annual expenses and multiply them by 25. For example, if you determine you need $80,000 per year to live, your target would be $2,000,000 ($80,000 x 25). While this is a helpful “back-of-the-napkin” calculation, critics argue that in an era of lower bond yields and higher market volatility, a more conservative 3.3% or 3.5% withdrawal rate (a 30x multiplier) may be safer for those planning a retirement longer than three decades.

Factoring in the Sequence of Returns Risk

A critical component that a simple multiplier doesn’t capture is “Sequence of Returns Risk.” This refers to the danger of the market experiencing a significant downturn in the first few years of your retirement. If you are forced to sell assets to fund your lifestyle when the market is down, you deplete your principal much faster, making it difficult for the portfolio to recover when the market eventually rebounds.

To mitigate this risk, many financial planners recommend a “Bucket Strategy.” This involves keeping 1–2 years of cash in a liquid account, 3–5 years of expenses in stable fixed-income assets (like bonds or CDs), and the remainder in a growth-oriented stock portfolio. This structure ensures that you never have to sell stocks during a bear market to pay your rent.

Strategic Wealth Accumulation and Investment Vehicles

Knowing your number is one thing; building the engine to reach it is another. The “how” of your saving strategy is just as important as the “how much.”

Maximizing Tax-Advantaged Accounts

Your choice of investment vehicle significantly impacts your “net” retirement income. In the United States, 401(k)s and Traditional IRAs offer tax-deferred growth, meaning you pay taxes upon withdrawal. Conversely, Roth IRAs and Roth 401(k)s are funded with after-tax dollars, allowing for tax-free withdrawals in retirement.

A sophisticated retirement plan often utilizes “Tax Diversification.” By having funds in both traditional and Roth accounts, you can strategically choose which accounts to draw from in a given year to manage your tax bracket. For instance, if you have a high-expense year due to a medical emergency or a big trip, pulling from a Roth account can prevent that extra spending from pushing you into a higher tax bracket.

The Power of Compounding and Asset Allocation

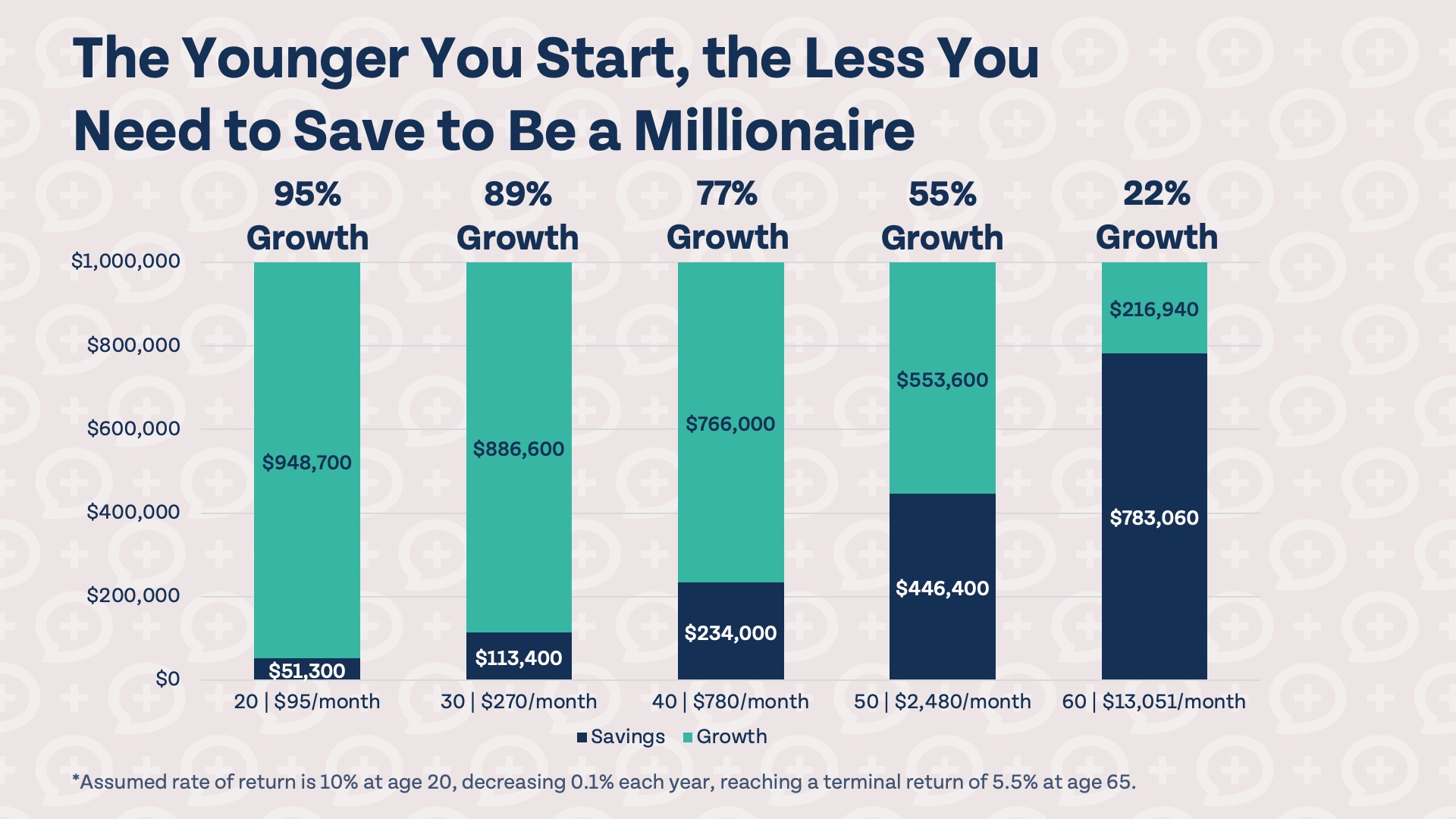

The greatest tool in your arsenal is time. Through the power of compounding, even modest contributions made in your 20s or 30s can grow to represent a massive portion of your final nest egg. As you approach your retirement goal, your asset allocation—the mix of stocks, bonds, and cash—should generally shift from “aggressive growth” to “capital preservation.”

However, being too conservative too early is a common mistake. Given that many people will spend 20 to 30 years in retirement, a portion of the portfolio must remain in equities to ensure the pot continues to grow even after you stop contributing. A classic “60/40” (stocks to bonds) split is a traditional baseline, though modern advisors often tailor this based on an individual’s risk tolerance and total net worth.

External Variables and Contingency Planning

No retirement plan exists in a vacuum. There are external factors that can either provide a safety net or act as a significant drain on your resources.

Healthcare Costs and Long-Term Care

Healthcare is often the largest “wildcard” expense in retirement. Many retirees underestimate the costs not covered by Medicare, including premiums, deductibles, and dental/vision care. According to recent estimates, a healthy couple retiring today might need upwards of $300,000 just to cover medical expenses throughout their retirement years.

Furthermore, long-term care—such as assisted living or home nursing—can evaporate a lifetime of savings in a matter of months. Incorporating Long-Term Care Insurance or setting aside a dedicated “health HSA” (Health Savings Account) is a vital part of protecting your core retirement fund from being depleted by medical emergencies.

Social Security and Passive Income Streams

On a more positive note, your “magic number” may be lower than expected once you factor in guaranteed income streams. Social Security, though often debated, remains a cornerstone of retirement for millions. By delaying your Social Security benefits until age 70, you can significantly increase your monthly payout, thereby reducing the amount you need to withdraw from your private investments.

Additionally, many retirees look toward “Online Income” or side hustles as a way to supplement their lifestyle. Whether it’s rental income from real estate, dividends from a brokerage account, or consulting in your former field, having multiple streams of income creates a “margin of safety.” If your investments are underperforming, these secondary streams can bridge the gap, allowing your main portfolio time to recover.

Conclusion: The Path to Financial Clarity

The journey to determining how much money you need to retire is an iterative process. It begins with a vision of your future self, moves through the cold mathematics of withdrawal rates and inflation, and concludes with a disciplined execution of your investment strategy.

There is no single “correct” number, but there is a “safe” number for you. By applying the 25x rule as a baseline, accounting for healthcare and inflation, and utilizing tax-advantaged accounts, you can transform retirement from a vague hope into a concrete, achievable goal. The most important step you can take today is to start tracking your expenses and optimizing your savings rate. The earlier you define your destination, the more certain your arrival will be.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.