For most households, a vehicle is the second largest purchase they will ever make, trailing only the acquisition of a home. Yet, in recent years, the financial burden of car ownership has shifted from a manageable monthly expense to a significant portion of the average consumer’s take-home pay. As supply chain disruptions, inflationary pressures, and rising interest rates have converged, the “average car payment” has reached historic heights.

Understanding these figures is no longer just about curiosity; it is a vital component of modern personal finance. To navigate the current automotive market without compromising your long-term wealth, you must look beyond the sticker price and delve into the mechanics of financing, interest, and the total cost of ownership.

The Current Landscape: Analyzing the Data Behind the Monthly Bill

The average car payment in the United States has undergone a dramatic transformation over the last three years. Data from major credit bureaus and automotive research firms indicate that the average monthly payment for a new vehicle now hovers around $730, while used car payments average approximately $530. These figures represent a stark increase from pre-2020 levels, driven by a combination of higher MSRPs and a tightening credit market.

New vs. Used: The Widening Financial Gap

Historically, used cars were the primary refuge for budget-conscious consumers. However, the used car market experienced unprecedented volatility recently, with prices surging as new car inventory dwindled. While the market has begun to stabilize, the “average” payment for a used vehicle remains high because many buyers are financing older vehicles at higher interest rates. When deciding between new and used, the payment often reflects a trade-off: a new car offers a lower interest rate but a higher principal, whereas a used car offers a lower principal but a significantly higher APR (Annual Percentage Rate).

The Impact of Rising Interest Rates

Interest rates are the “silent” component of a car payment. In a low-interest environment, a $40,000 loan might feel manageable. However, as the Federal Reserve has raised rates to combat inflation, auto loan APRs have followed suit. For a buyer with “prime” credit, rates might sit between 5% and 7%. For those in the “subprime” category, rates can soar above 15% or even 20%. A 5% difference in an interest rate can result in thousands of dollars added to the total cost of the loan, significantly inflating the monthly payment without adding any value to the vehicle itself.

The Trend Toward Longer Loan Terms

To keep monthly payments “affordable” in the face of rising prices, many lenders and consumers have turned to extended loan terms. While 48-month or 60-month loans were once the standard, 72-month and 84-month loans are now increasingly common. While this strategy lowers the immediate monthly output, it is a dangerous financial maneuver. Longer terms lead to “negative equity”—a situation where you owe more on the car than it is actually worth—for a longer duration of the ownership cycle.

Key Factors That Dictate Your Monthly Outlay

Identifying the average is helpful for benchmarking, but your specific car payment is determined by a unique intersection of personal financial health and market conditions. Understanding these levers allows you to manipulate them in your favor before you ever step onto a dealership lot.

Credit Scores and Their Financial Weight

Your credit score is the single most influential factor in determining your car payment outside of the vehicle’s price. Lenders categorize borrowers into tiers: Super Prime, Prime, Nonprime, Subprime, and Deep Subprime. The difference in a monthly payment between a Super Prime buyer and a Subprime buyer on the exact same vehicle can be as much as $200 per month. Improving your credit score by even 50 points before applying for a loan can save you a fortune over the life of the loan.

The Power of the Down Payment

The “average” payment often assumes a minimal down payment, but this is a pitfall for the savvy investor. A substantial down payment serves two purposes: it reduces the principal amount borrowed (which lowers the monthly payment) and it provides an immediate equity cushion. In a market where new cars can lose 20% of their value in the first year, a 20% down payment ensures that you aren’t “underwater” the moment you drive off the lot.

Trade-in Values in a Volatile Market

Your current vehicle is a financial asset that can be leveraged to lower your next car payment. However, many consumers fail to research their trade-in value independently, often accepting the first offer from a dealer. By treating your trade-in as a separate transaction and obtaining multiple quotes from third-party buyers, you can maximize the “credit” applied to your new purchase, effectively lowering the amount you need to finance.

The 20/4/10 Rule and Financial Frameworks

How much should you be paying? Personal finance experts often point to the “20/4/10 rule” as a gold standard for maintaining a healthy budget while owning a vehicle. While the “average” payment may be high, your personal limit should be dictated by your income, not by market trends.

Deciphering the 20/4/10 Guideline

The 20/4/10 rule suggests the following:

- 20% Down: Put at least 20% down on the vehicle.

- 4-Year Term: Finance the vehicle for no more than four years (48 months).

- 10% of Income: Ensure that your total transportation costs (including payment, insurance, and fuel) do not exceed 10% of your gross monthly income.

Following this rule prevents “car-rich, cash-poor” scenarios where a significant portion of a household’s wealth is tied up in a depreciating asset.

Assessing Total Cost of Ownership (TCO)

The monthly payment is only one part of the financial equation. To truly understand the impact of a car on your “Money” niche goals, you must calculate the Total Cost of Ownership. This includes insurance premiums (which are rising alongside car prices), scheduled maintenance, unscheduled repairs, fuel or charging costs, and registration fees. A car with a $500 payment might actually cost $900 per month to keep on the road.

Leasing vs. Buying: A Monthly Comparison

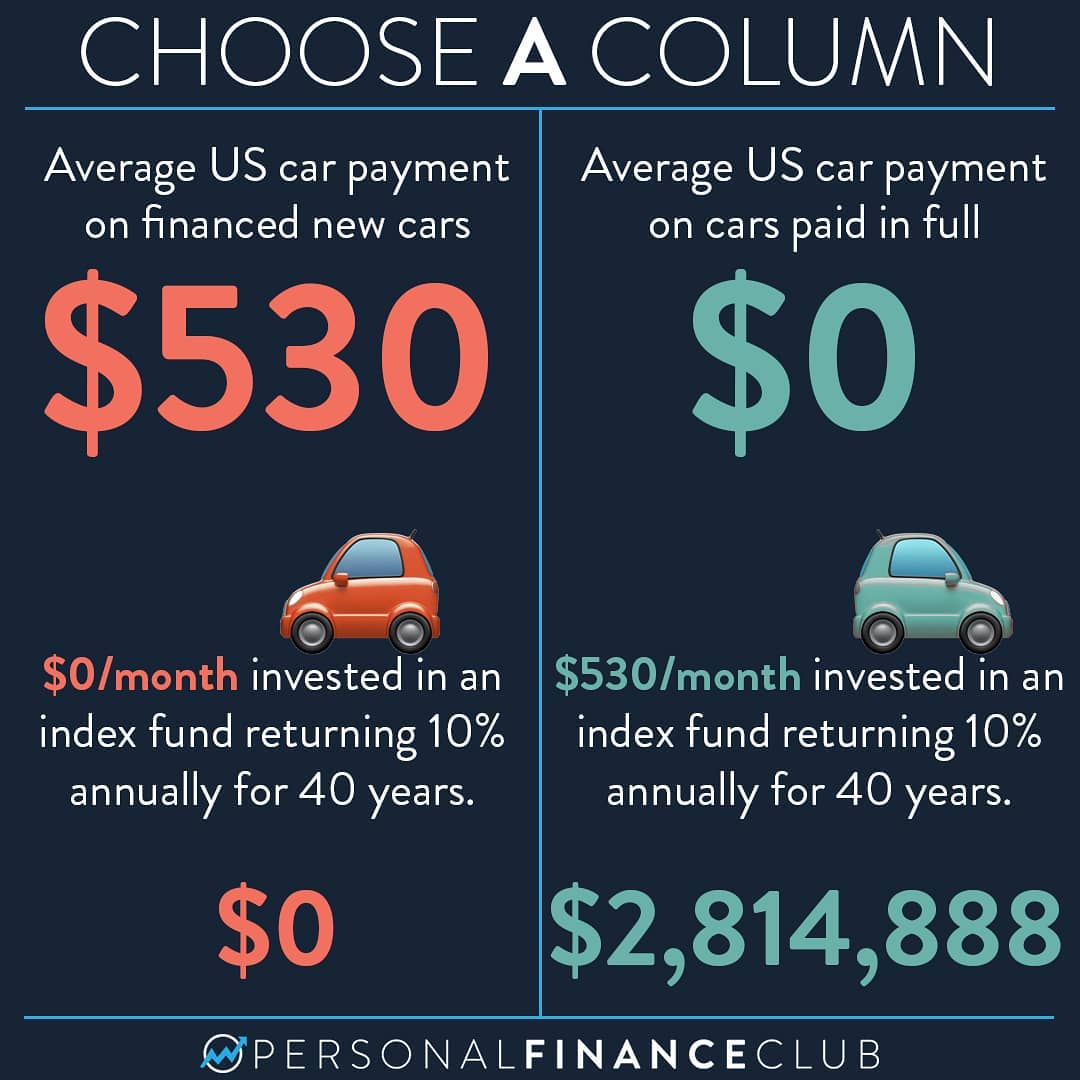

Leasing is often marketed as a way to get a lower monthly payment on a more expensive car. While the average lease payment is indeed lower than the average purchase payment, it is important to remember that leasing is essentially a long-term rental. You are paying for the vehicle’s depreciation during the most expensive years of its life. From a wealth-building perspective, buying a reliable vehicle and driving it long after the loan is paid off is almost always the superior financial move.

Strategies to Lower Your Monthly Car Payment

If you find yourself facing a car payment that is higher than the average or higher than your budget allows, there are several strategic moves you can make to regain control of your cash flow.

Refinancing Existing Auto Loans

If interest rates have dropped since you bought your car, or if your credit score has significantly improved, refinancing is a powerful tool. By moving your loan to a different lender—often a credit union, which typically offers lower rates than commercial banks or dealership financing—you can reduce your APR. This can either lower your monthly payment or allow you to pay off the principal faster without increasing your monthly outlay.

Gap Insurance and Add-ons: What to Trim

During the “F&I” (Finance and Insurance) stage of a car purchase, dealers often bundle products like extended warranties, tire and wheel protection, and GAP insurance into the loan. While some of these have value, they are often marked up significantly. Financing these items increases your monthly payment. In many cases, you can purchase similar protection through your own insurance provider or a third party for a fraction of the cost, or simply opt out and self-insure through an emergency fund.

Shopping for the Loan Before the Car

One of the biggest mistakes consumers make is “payment shopping” at the dealership. Dealerships are incentivized to focus on the monthly payment because they can hide the total cost of the loan by extending the term or increasing the interest rate. To avoid this, secure a pre-approval from your bank or credit union before you visit a dealer. This sets a hard ceiling on your interest rate and allows you to negotiate the “out-the-door” price of the car as a cash buyer would, ensuring your monthly payment is a reflection of value rather than financial manipulation.

Conclusion: Balancing Mobility and Wealth

The average car payment of $700+ is a sobering reminder of the current economic climate, but it does not have to be your reality. In the realm of personal finance, a vehicle should be viewed as a tool for utility, not a status symbol that compromises your ability to invest, save for retirement, or build an emergency fund.

By understanding the components of a car loan—from the impact of credit scores to the hidden costs of extended terms—you can make an informed decision that aligns with your financial goals. Whether that means buying a reliable used car in cash, adhering to the 20/4/10 rule, or aggressively refinancing an existing high-interest loan, the goal is the same: to minimize the cost of mobility so you can maximize the growth of your net worth. In the journey toward financial independence, the car you drive is far less important than the speed at which you are building your assets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.