Discovering you owe the IRS can be a moment of significant stress and confusion. Whether it’s a surprising balance due after filing your tax return, a notice from the IRS demanding payment, or simply the proactive question of what your potential liability might be, understanding “how much I owe IRS” is a critical first step towards financial peace of mind. This isn’t just about a number; it’s about navigating the complex landscape of personal finance, taxation, and your obligations as a taxpayer. Ignoring a tax debt won’t make it disappear; in fact, it often leads to escalating penalties and interest. This comprehensive guide will dissect the reasons behind tax liabilities, walk you through the process of accurately determining your debt, explore actionable strategies for managing what you owe, and provide insights on how to prevent similar situations in the future, all firmly within the realm of personal finance and financial tools.

Unraveling Your Tax Bill: Why You Might Owe

The first step in addressing an IRS tax bill is to understand its origin. A tax liability doesn’t appear out of thin air; it’s a direct result of your financial activities and how they interact with the tax code. Pinpointing the root cause is crucial for both resolving the current situation and preventing future surprises.

Common Reasons for Unexpected Tax Debt

Several scenarios can lead to an unexpected tax bill, often catching taxpayers off guard. Understanding these can help demystify the amount you owe.

Insufficient Withholding or Estimated Payments

One of the most frequent culprits is insufficient tax withholding from your paycheck or inadequate estimated tax payments throughout the year. If you’re an employee, your W-4 form dictates how much tax your employer withholds. If you claimed too many allowances, or didn’t update your W-4 after a significant life change (like marriage, having a child, or getting a second job), you might have paid too little tax during the year. For self-employed individuals, freelancers, or those with significant investment income, estimated taxes are crucial. Failing to pay these quarterly or underestimating your income can lead to a substantial bill at tax time. The “pay-as-you-go” system is fundamental to U.S. tax law, and deviating from it often results in a balance due.

Untaxed Income and Capital Gains

Income sources that aren’t subject to regular withholding can also contribute to a tax debt. This includes income from investments (stock dividends, interest, capital gains from selling assets), rental properties, or side hustles that don’t issue a W-2. While you might receive a Form 1099 for some of these, the tax isn’t automatically deducted. If you had a banner year in the stock market or sold a property for a profit, the resulting capital gains can significantly increase your taxable income and, consequently, your tax liability. Many taxpayers overlook the tax implications of these types of income until they’re preparing their returns.

Life Changes and Financial Events

Significant life events often have profound tax implications that are easy to overlook. Getting married or divorced, having children, buying or selling a home, changing jobs, or even inheriting assets can all alter your tax situation. For instance, a new marriage might push you into a higher tax bracket when filing jointly, or a large bonus from work might not have had enough tax withheld. Similarly, if you made early withdrawals from retirement accounts (like a 401(k) or IRA), these distributions are typically taxable and can also incur a 10% early withdrawal penalty if you’re under 59½, adding to your debt. Without proactive adjustments to your withholding or estimated payments, these changes can lead to an unexpected balance due.

Key Documents to Verify Your Liability

Before you panic about the amount, gather and review all relevant financial documents. These provide the factual basis for your tax obligations.

Your Filed Tax Return (Form 1040 and Schedules)

If you’ve already filed your return and received a notice, your Form 1040 (or 1040-SR) is your primary reference. Review every line, especially those detailing your income, deductions, credits, and payments. Pay close attention to Schedule 1 (Additional Income and Adjustments to Income), Schedule B (Interest and Ordinary Dividends), Schedule D (Capital Gains and Losses), and Schedule C (Profit or Loss from Business) if applicable. Your tax software or preparer should have provided you with a copy. The “Amount You Owe” line will clearly state your reported liability. If the IRS notice shows a different amount, it’s crucial to understand why – it could be an adjustment made by the IRS or a miscalculation on your part.

Income Statements (W-2s, 1099s, K-1s)

These forms summarize the income you received throughout the year. Your W-2s from employers show wages, tips, and other compensation, along with taxes withheld. Various 1099 forms (1099-NEC for non-employee compensation, 1099-INT for interest, 1099-DIV for dividends, 1099-B for stock sales, etc.) report other forms of income. If you have interests in partnerships or S corporations, you’ll receive a Schedule K-1. Ensure all your income sources reported on these forms are accurately reflected on your tax return. Discrepancies here are a common reason for IRS adjustments and additional tax due.

Records of Payments Made

Verify all tax payments you’ve made throughout the year. This includes federal income tax withheld from your paychecks (as shown on W-2s), estimated tax payments you made directly to the IRS (Form 1040-ES), and any payments made with an extension request (Form 4868). Sometimes, the IRS’s records might not perfectly align with yours, especially if a payment was made recently or through an unusual method. Keeping meticulous records of payment dates and confirmation numbers can be invaluable in resolving any discrepancies.

The Path to Precision: Calculating Your True Liability

Once you understand why you might owe, the next step is to accurately calculate the exact amount. This involves a careful review of your tax return, leveraging available tools, and knowing when to seek professional assistance. Getting this right is paramount to avoiding overpayment or further issues with the IRS.

Methodical Review of Your Tax Return

A line-by-line review of your tax return, specifically Form 1040 and its accompanying schedules, is the most direct way to verify your liability. This process allows you to identify any errors, omissions, or misinterpretations that could lead to an incorrect balance.

Income Verification

Start by cross-referencing all income reported on your W-2s, 1099s, and K-1s with what you reported on your Form 1040. Ensure that every source of taxable income, including wages, self-employment income, interest, dividends, capital gains, and rental income, is correctly entered. Pay attention to boxes on 1099 forms that indicate federal income tax withheld; sometimes, small amounts are withheld from investment income, which reduces your overall liability. A mismatch in income reporting is one of the most common reasons for an IRS notice and a change in your tax due.

Deduction and Credit Analysis

Next, thoroughly review all deductions and credits you claimed. Did you qualify for all of them? Were they calculated correctly? Deductions (like student loan interest, IRA contributions, or itemized deductions) reduce your taxable income, while credits (like the Child Tax Credit, Earned Income Tax Credit, or education credits) directly reduce the amount of tax you owe, dollar for dollar. Mistakes in claiming these, either through oversight or incorrect eligibility, can significantly impact your final tax bill. For instance, accidentally claiming a dependent that doesn’t qualify or miscalculating a business expense deduction can lead to an underpayment.

Understanding Penalties and Interest

If you owe money to the IRS, it’s likely that penalties and interest will be added to your original tax liability. It’s crucial to understand these additional charges.

- Failure-to-File Penalty: This is typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax.

- Failure-to-Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25% of your unpaid tax. It’s important to note that if both penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay penalty for that month.

- Accuracy-Related Penalty: If the IRS determines your underpayment resulted from negligence or substantial understatement of income, they might impose a 20% penalty on the underpaid amount.

- Interest: Interest is charged on underpayments, and on unpaid penalties, from the due date of the return until the date the tax is paid in full. The interest rate is determined quarterly and is typically the federal short-term rate plus 3 percentage points. Interest compounds daily, meaning it grows on both the original tax due and any accumulated interest. Understanding these additions is key to knowing the total amount you truly owe.

Leveraging IRS Resources and Professional Help

While self-review is valuable, external resources and expertise can provide invaluable accuracy and peace of mind.

IRS.gov and Online Tools

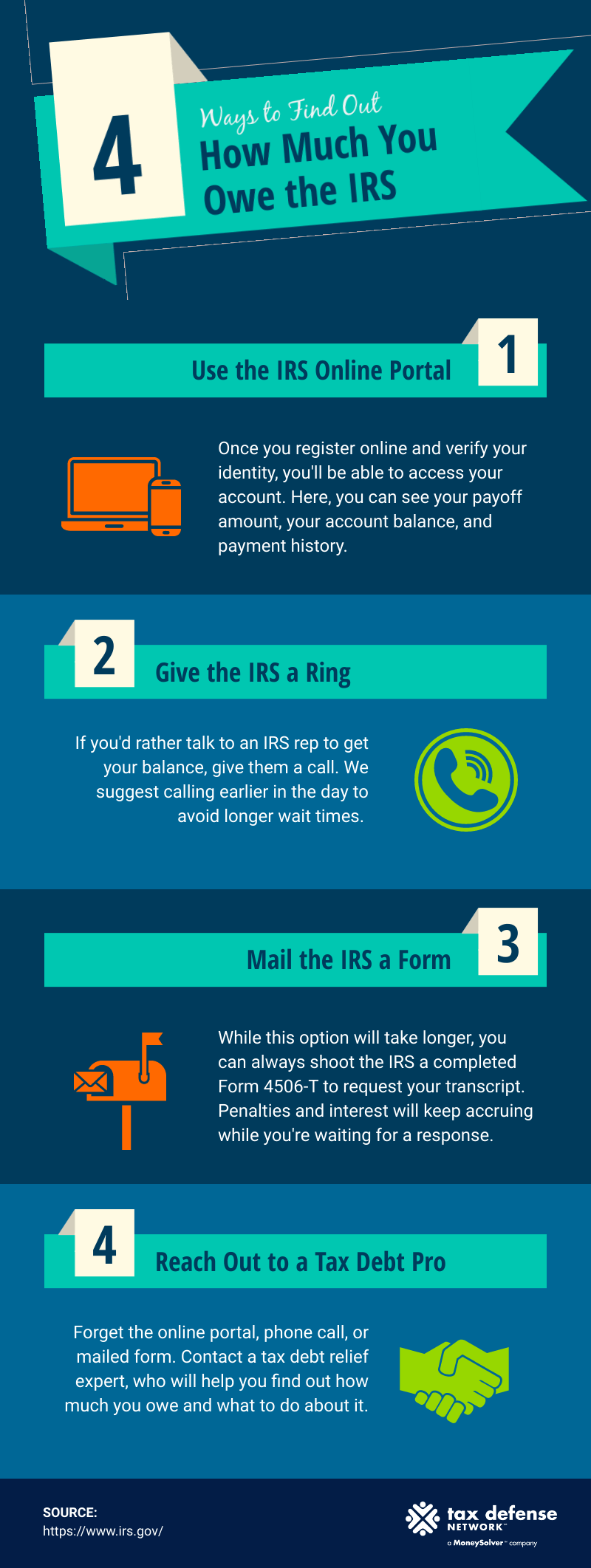

The IRS website (IRS.gov) is a treasure trove of information and tools. You can find forms, publications, and specific instructions for various tax situations. The “Tax Withholding Estimator” is an excellent tool for adjusting your W-4 to prevent future underpayments. For current year issues, you can often check your account balance by creating an IRS online account. This secure portal allows you to view your tax balance, payment history, and key tax return information for the current tax year and the prior nine years. This is particularly useful if you’ve received a notice and want to verify the IRS’s stated amount.

Tax Software and Calculators

If you used tax software (like TurboTax, H&R Block, or TaxAct) to prepare your original return, you can often revisit your file and run “what-if” scenarios or re-check calculations. Most reputable tax software packages have built-in calculators and audit risk assessments that can help identify potential issues. There are also numerous online tax calculators (both free and paid) that can help you estimate your tax liability based on your income and deductions, allowing you to cross-reference your own calculations.

When to Seek Professional Tax Assistance

For complex situations, significant discrepancies, or if you simply feel overwhelmed, consulting a tax professional is highly recommended.

- Certified Public Accountants (CPAs): CPAs are licensed accountants who can prepare tax returns, provide financial planning advice, and represent taxpayers before the IRS.

- Enrolled Agents (EAs): EAs are tax specialists authorized by the IRS to represent taxpayers in all matters before the IRS, including audits, collections, and appeals.

- Tax Attorneys: For severe issues, such as audits, appeals, or criminal investigations, a tax attorney offers legal expertise and attorney-client privilege.

A qualified professional can review your return for errors, help you understand IRS notices, advise on the best payment strategies, and even negotiate with the IRS on your behalf. Their expertise can save you money, time, and significant stress in the long run, especially when dealing with penalties or complex tax situations.

Action Plan: Strategies for Addressing Your IRS Debt

Once you’ve accurately determined how much you owe the IRS, the immediate concern shifts to payment. It’s crucial to address the debt promptly to prevent further penalties and interest. Fortunately, the IRS offers several pathways for taxpayers who find themselves owing money, whether they can pay in full or need more time.

Paying Your Tax Bill in Full

If you have the funds available, paying your tax bill in full by the due date (usually April 15th, or the extended due date if you filed an extension) is always the best option. This immediately stops the accrual of further penalties and interest, providing immediate closure to your tax obligation.

IRS Direct Pay

One of the easiest and most secure ways to pay is through IRS Direct Pay. This free service allows you to make tax payments directly from your checking or savings account. You can schedule payments up to 365 days in advance, providing flexibility. No registration is required, and you receive an email confirmation of your payment. It’s an excellent option for one-time payments or estimated tax installments.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is a federal tax payment system used by individuals and businesses. While it requires enrollment, it offers greater control and flexibility once set up. You can schedule payments up to 365 days in advance, view your payment history, and receive email confirmations. It’s particularly useful for those who make frequent estimated tax payments or need to manage business tax obligations.

Debit, Credit Card, or Digital Wallet

The IRS also accepts payments via debit card, credit card, or digital wallet through approved third-party payment processors. While convenient, these processors charge a fee, which varies depending on the provider and payment method. This option might be appealing if you need to buy time, earn credit card rewards (if you can pay off the balance quickly), or if you lack sufficient funds in your bank account for a direct payment. However, weigh the processing fees against the potential interest and penalties you’d incur from the IRS if you delayed payment.

If You Can’t Pay Immediately: Exploring Payment Options

Many taxpayers find themselves in a situation where they owe money but don’t have the immediate cash flow to pay it off. The IRS has established various programs to help taxpayers manage their debt without resorting to extreme measures. It’s vital to contact the IRS as soon as possible if you can’t pay; ignoring the problem will only make it worse.

Short-Term Payment Plan (STPP)

If you need a little more time, typically up to 180 days, you might qualify for a short-term payment plan. While interest and a failure-to-pay penalty still apply, this plan allows you a brief reprieve to gather the necessary funds without formal paperwork or a setup fee. You can request this directly when e-filing your return, through your IRS online account, or by contacting the IRS. It’s ideal for those who anticipate receiving funds (like a bonus or a maturity of an investment) within the next few months.

Offer in Compromise (OIC)

An Offer in Compromise allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. The IRS may agree to an OIC if there’s doubt as to collectibility (you can’t afford to pay), doubt as to liability (you believe the amount is incorrect), or if paying the full amount would create economic hardship. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating an OIC. It’s a complex process that requires significant documentation (Form 656, Form 433-A, etc.) and is typically reserved for taxpayers facing significant financial distress where full payment would prevent them from meeting basic living expenses. A qualified tax professional can greatly assist in preparing and negotiating an OIC.

Installment Agreement (IA)

An Installment Agreement allows you to make monthly payments for up to 72 months (6 years). This is generally available if you owe a combined total of under $50,000 in tax, penalties, and interest (for individuals) or $25,000 (for businesses). While an installment agreement is in effect, penalties and interest continue to accrue, but the failure-to-pay penalty rate is reduced. There’s a setup fee for an installment agreement, but it’s often reduced or waived for low-income taxpayers. You can apply for an installment agreement online via IRS.gov/OPA, by mail using Form 9465, or by calling the IRS. This option provides a structured way to pay off your debt over an extended period.

Considering a Loan or Credit Line

In some cases, securing a personal loan, home equity line of credit (HELOC), or even a balance transfer credit card might be considered to pay off an IRS debt. The primary benefit is that the interest rate on a personal loan or HELOC could be significantly lower than the combined penalty and interest rates charged by the IRS. It consolidates your debt and typically simplifies payments to a single lender. However, this option should be approached with caution. You’re effectively trading one debt for another, and if you can’t manage the loan payments, you could end up in a worse financial position, potentially even risking collateral like your home with a HELOC. Carefully compare interest rates, fees, and repayment terms before opting for external financing.

Proactive Measures: Avoiding Future Tax Surprises

The best defense against a future tax bill is a strong offense rooted in meticulous planning and regular financial review. Proactive tax management isn’t just for businesses; it’s a cornerstone of sound personal finance that can save you significant stress, penalties, and interest.

Adjusting Your Withholding and Estimated Payments

The “pay-as-you-go” system requires that taxes are paid throughout the year, either through wage withholding or estimated tax payments. Ensuring these are set correctly is the most effective way to prevent future underpayments.

Optimizing Your W-4

If you’re an employee, your Form W-4, Employee’s Withholding Certificate, is your primary tool for managing federal income tax withholding. Review and update your W-4 annually, or whenever you experience a significant life event such as marriage, divorce, having a child, purchasing a home, or changing jobs. The IRS Tax Withholding Estimator on IRS.gov is an invaluable online tool that helps you tailor your withholding to your specific financial situation, accounting for multiple jobs, deductions, and credits. The goal is to have enough tax withheld to cover your liability without having too much withheld, which essentially gives the government an interest-free loan.

Making Accurate Estimated Tax Payments

For self-employed individuals, freelancers, gig workers, those with significant investment income, or anyone else who doesn’t have taxes withheld from their primary income, estimated tax payments are critical. These payments are typically made quarterly (April 15, June 15, September 15, and January 15 of the following year) using Form 1040-ES. Accurately estimating your income and deductions for the year is key. If your income fluctuates, you might need to adjust your estimated payments throughout the year. The IRS has an estimated tax worksheet in Publication 505 that can help, or you can use tax software to project your income and liability. Failing to pay enough estimated tax can result in underpayment penalties, even if you pay the full balance due by the April deadline.

Maximizing Deductions and Credits

Understanding and properly utilizing all available deductions and credits can significantly reduce your taxable income and direct tax liability, helping you avoid an unexpected bill.

Understanding Eligibility and Limitations

Tax laws are complex, and eligibility for deductions and credits often comes with specific criteria and limitations. For instance, the Child Tax Credit has income phase-outs, and certain itemized deductions might only benefit you if they exceed the standard deduction. Research common deductions (e.g., IRA contributions, student loan interest, HSA contributions) and credits (e.g., education credits, dependent care credit, energy efficiency credits) that might apply to your situation. Don’t claim deductions or credits without understanding their rules; doing so can lead to an IRS audit or penalties.

Meticulous Record Keeping

The golden rule of tax planning is excellent record keeping. For every deduction or credit you claim, you must have documentation to back it up. This includes receipts for charitable donations, medical expenses, business expenses, educational costs, and home improvements. Keep digital and physical copies of all relevant financial statements, bank statements, investment records, and tax forms for at least three to seven years, as recommended by the IRS. Good records not only help you accurately claim what you’re entitled to but also provide crucial evidence if the IRS ever questions your return. Digital tools, cloud storage, and personal finance software can greatly simplify this process.

Financial Planning and Tax Forecasting

Integrating tax considerations into your overall financial planning is a powerful strategy for long-term financial health and avoiding tax surprises.

Year-Round Tax Planning

Don’t wait until tax season to think about taxes. Engage in year-round tax planning. This involves reviewing your financial situation periodically, especially after major life events, and proactively making tax-advantaged decisions. For example, considering the tax implications before selling a large investment, making a significant charitable contribution, or adjusting your retirement contributions can make a substantial difference. A good financial planner or tax advisor can help you integrate tax strategies into your broader financial goals, such as retirement planning, college savings, and wealth accumulation.

Utilizing Financial Tools for Projections

Leverage modern financial tools and software to project your tax liability throughout the year. Many personal finance apps allow you to categorize income and expenses, which can be invaluable for estimating self-employment income and associated deductions. Tax planning software can help you run “what-if” scenarios, such as the tax impact of selling a stock, contributing more to your 401(k), or making a large deductible purchase. These tools empower you to make informed financial decisions that align with your tax goals and minimize your liability.

Understanding “how much I owe IRS” is not merely about a debt; it’s a critical component of personal financial management. By proactively understanding the reasons for potential tax liabilities, diligently calculating the exact amount due, strategically addressing the payment, and implementing preventative measures, you can transform a stressful situation into an opportunity for greater financial control and peace of mind. Staying informed, utilizing available resources, and seeking professional guidance when needed are all essential steps on the path to a healthier financial future, free from unexpected tax burdens.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.