Navigating the intersection of earned income and Social Security benefits can feel like a complex puzzle, especially as you approach or enter retirement. Understanding the rules around earnings limits is crucial for maximizing your financial well-being during this significant life transition. This article delves into the specifics of how much you can earn while still receiving your Social Security benefits, exploring the thresholds, the implications of exceeding them, and strategies to manage your income effectively.

Understanding Social Security Earnings Limits

The Social Security Administration (SSA) has established specific rules that limit how much beneficiaries can earn from work without affecting their retirement benefits. These limits are in place for individuals who claim benefits before reaching their Full Retirement Age (FRA). The purpose of these limits is to ensure that Social Security retirement benefits are primarily intended for those who have largely stopped working. Once you reach your FRA, these earnings limits no longer apply.

Who is Affected by Earnings Limits?

The earnings limits primarily impact individuals who are:

- Receiving Social Security Retirement Benefits: This applies to those who have started drawing their retirement benefits.

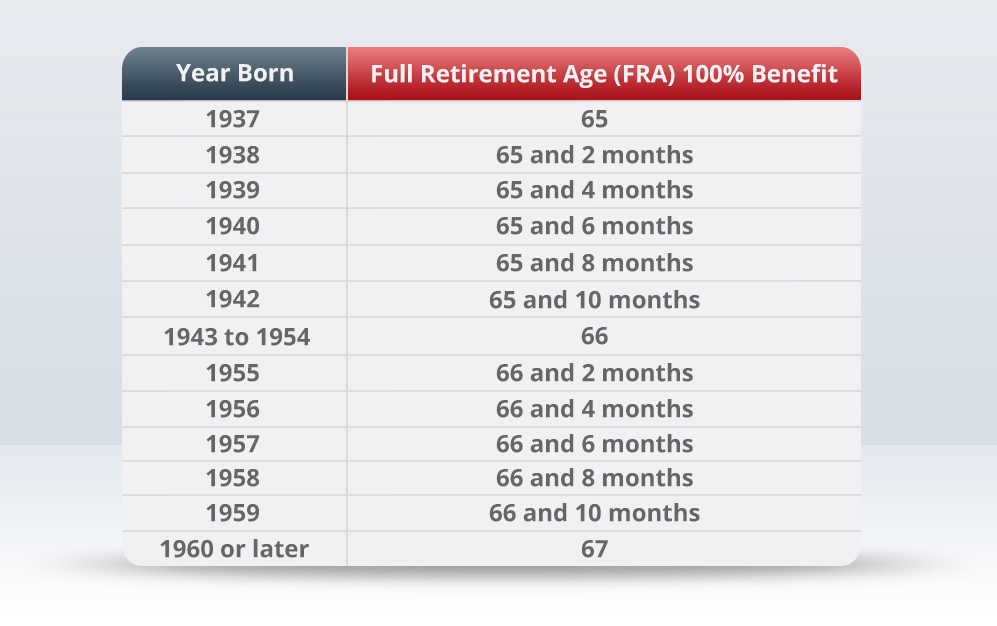

- Under Full Retirement Age (FRA): Your FRA is determined by your birth year. For those born in 1960 or later, the FRA is 67. For those born earlier, it ranges from 65 to 66 and 2 months.

- Still Working: The limits are based on your earned income from wages and net earnings from self-employment. Other forms of income, such as pensions, annuities, interest, dividends, and capital gains, do not count towards these limits.

The Two Tiers of Earnings Limits

The SSA uses two distinct earnings limits for individuals under their FRA, depending on the year and whether the individual has reached their FRA within that year.

The Lower Earnings Limit (for months before reaching FRA)

For the year in which you reach your FRA, a different, more generous limit applies for the months before you hit that birthday. In 2024, this lower limit is $59,520 per year.

- How it Works: For every dollar you earn above this threshold, your Social Security benefit will be reduced by $1. This reduction is applied on a monthly basis. The SSA essentially “recaptures” the excess benefit paid out during the months you earned above the limit.

- Example: If you are 63 and working, and your FRA is 67, and you earn $65,000 in 2024, you would be subject to the lower earnings limit calculation until you reach your FRA. If you reach your FRA in October 2024, the earnings limit calculation will apply only to your income earned from January to September.

The Higher Earnings Limit (for the year you reach FRA)

Once you reach your Full Retirement Age, the earnings limits are significantly relaxed. In 2024, the higher earnings limit is $22,320 per year.

- How it Works: For every dollar you earn above this higher threshold, your Social Security benefit is reduced by $0.50. This means that you can earn more before your benefits begin to be reduced once you are closer to or at your FRA.

- Example: If you reach your FRA in October 2024, and you earn $30,000 in 2024, the first $22,320 is disregarded. The excess is $7,680 ($30,000 – $22,320). Your benefits would be reduced by $3,840 (50% of $7,680). However, this reduction is only applied to the benefits you receive before you reach your FRA. Once you turn your FRA, there is no longer any reduction in benefits due to earnings.

The Year You Reach Full Retirement Age: A Special Calculation

The SSA employs a prorated calculation for the year you reach your FRA. This is a critical point for many retirees who might continue working part-time or even full-time as they approach their FRA.

- The Rule: In the month you reach your FRA, the earnings limits are no longer in effect. Therefore, the SSA calculates your earnings limit for the entire year in which you reach FRA by applying the higher limit for the months you are under FRA, and then effectively removing the limit for the months you are at or above FRA.

- Example (Continuing): Let’s revisit the individual who reaches FRA in October 2024.

- From January to September (9 months), they are under FRA. The monthly equivalent of the higher limit ($22,320 / 12 = $1,860 per month) would apply to these months, with a $1 reduction for each dollar earned above this.

- From October to December (3 months), they are at or above FRA. There is no earnings limit for these months.

- The SSA will calculate the total earnings limit for the year by summing the prorated limits for the months before FRA.

- Any earnings above the prorated limit for the months under FRA will cause a reduction in benefits only for those months. Once they reach FRA, any earnings, no matter how high, will not affect their monthly benefit amount.

What Happens to Reduced Benefits?

If your benefits are reduced due to exceeding the earnings limits, those reductions are not permanent.

- Benefit Adjustments: For each month your benefits were withheld due to exceeding the earnings limits, your benefit amount will be recalculated and increased. This adjustment is made starting in the month you reach your FRA. The SSA effectively “gives back” the benefits that were withheld, but without any interest.

- Lifetime Impact: While the reduction is temporary, it’s important to understand that you don’t receive the withheld amount as a lump sum. Instead, your monthly benefit amount is increased to reflect the months your benefits were previously reduced. This ensures that over your lifetime, you receive the correct total amount of benefits based on your claiming age and earnings history.

Strategies for Managing Earnings and Social Security Benefits

Given the nuances of Social Security earnings limits, a proactive approach to financial planning is essential for individuals who wish to continue working while receiving benefits.

Strategic Retirement Claiming Dates

Your decision on when to start claiming Social Security benefits has a significant impact on how earnings limits will affect you.

- Claiming Early: If you claim benefits as early as possible (age 62), you will be subject to the earnings limits for a longer period. Your initial benefit amount will also be permanently reduced.

- Delaying Benefits: By delaying your benefits until your FRA, you avoid the earnings limits altogether and receive your full monthly benefit. If you plan to continue working significantly beyond age 62, delaying your claim might be a financially advantageous strategy.

- The “Sweet Spot”: For some, continuing to work and delaying benefits until FRA might be the most beneficial strategy, allowing for higher earnings and a higher monthly Social Security payment, free from earnings limitations.

Optimizing Your Work and Income Streams

Consider how your work and other income sources interact with Social Security.

- Reviewing Your Work Structure: If you are self-employed, consider how your business structure and income are reported. While net earnings from self-employment count towards the earnings limit, some business expenses might reduce your taxable income. Consulting with a tax professional can be invaluable here.

- Understanding Non-Earned Income: Remember that pensions, annuities, interest, dividends, and capital gains do not count towards the earnings limits. If you have significant income from these sources, they will not affect your Social Security benefits even if you are below FRA. This can be a strategy to supplement your income without triggering benefit reductions.

- Part-Time vs. Full-Time: If you are considering returning to work, evaluate the number of hours and the potential income. A part-time role might keep you below the earnings limits, allowing you to receive your full benefits, while a full-time position might necessitate a more careful consideration of claiming strategies.

Planning for the Future and Beyond FRA

As you approach and pass your FRA, the earnings limits become irrelevant. This is a key milestone in managing your finances in retirement.

- The Power of FRA: Once you reach your Full Retirement Age, you can earn as much as you want from work, and your Social Security benefits will not be reduced. This can be a significant financial boost, allowing you to enjoy more disposable income in your later years.

- Future Benefit Adjustments: Even if your benefits were reduced in the years before FRA, they will be permanently increased once you reach FRA to account for the months withheld. This means the SSA is essentially “repaying” those withheld benefits through a higher monthly payment starting at FRA.

The Role of Self-Employment in Social Security Earnings

Self-employment income presents a unique set of considerations when it comes to Social Security earnings limits. The SSA looks at your net earnings from self-employment, which is your gross income minus your allowable business expenses.

Calculating Net Earnings from Self-Employment

Understanding how your self-employment income is categorized is crucial.

- Gross Income: This includes all income generated from your business activities.

- Business Expenses: These are costs directly related to operating your business. It’s important to keep meticulous records of all expenses.

- Net Earnings: Your net earnings are then subject to Social Security taxes. However, for the purpose of the earnings test, the SSA uses your net earnings before deducting half of your self-employment tax. This is a common point of confusion.

Social Security and Medicare Taxes

It’s important to distinguish between income that counts towards earnings limits and income subject to Social Security and Medicare taxes.

- Social Security Tax: This tax is only levied on earnings up to a certain annual limit (the Social Security wage base, which is $168,600 in 2024). Once you reach this limit, you no longer pay Social Security tax on additional earnings for that year.

- Medicare Tax: There is no wage base limit for Medicare taxes. All your earnings are subject to the Medicare tax, regardless of how high they are.

- Impact on Earnings Test: The Social Security tax portion of your self-employment tax is what is considered when calculating your net earnings for the earnings test. However, the calculation for the earnings test is distinct from how you calculate your taxable income for income tax purposes. The SSA’s calculation is based on your net earnings from self-employment, reduced by your allowable business expenses, and then factoring in certain deductions related to self-employment tax.

Practical Implications for Self-Employed Individuals

- Consult a Tax Professional: Given the complexities of self-employment income and Social Security, it is highly advisable to work with a qualified tax advisor or accountant. They can help you accurately calculate your net earnings, understand deductions, and navigate the Social Security earnings test.

- Quarterly Tax Payments: Self-employed individuals are typically required to make estimated tax payments quarterly. Ensure these payments accurately reflect your anticipated income and tax obligations, including those related to Social Security.

- Annual Reporting: When you file your annual tax return, you will report your self-employment income and expenses. This is the primary way the SSA will receive information about your earnings for the year, which they will then use to determine if any benefits need to be adjusted.

The “Recapture” of Withheld Benefits

A common concern for those approaching or in retirement is whether they permanently lose the Social Security benefits that were withheld due to exceeding earnings limits. The good news is that these benefits are not lost forever.

How Recapture Works

The SSA employs a “recapture” mechanism to ensure that individuals eventually receive the full amount of benefits they are entitled to, considering their claiming age and any applicable earnings limitations.

- Benefit Adjustments at Full Retirement Age: The primary way benefits are recaptured is through an upward adjustment of your monthly benefit amount starting in the month you reach your Full Retirement Age (FRA). For every month your benefits were reduced due to exceeding the earnings limits in prior years, your monthly benefit amount will be increased once you reach FRA.

- No Interest on Withheld Amounts: It’s important to note that this adjustment is a simple increase in your monthly payment; you do not receive the withheld amounts as a lump sum, nor do you receive any interest on those funds. The SSA is essentially “making up” for the months you didn’t receive your full benefit.

- Revised Benefit Calculation: Your benefit amount will be recalculated to reflect the total benefit you would have received if the earnings limits had not applied. This ensures that over your lifetime, you receive the correct total sum of benefits.

Example of Recapture

Let’s consider an individual who claimed Social Security at age 65 and has an FRA of 67. In the year they turned 66 (one year before their FRA), they earned $30,000 above the higher earnings limit. This would result in a reduction of their Social Security benefits for that year.

When this individual reaches their FRA of 67, the SSA will review their earnings history. They will calculate the total amount of benefits that were withheld in the previous year due to exceeding the earnings limit. This withheld amount will then be distributed by increasing their monthly benefit payment from age 67 onwards. This increase will continue for the rest of their life.

Implications for Long-Term Financial Planning

- Long-Term Value: While the immediate effect of exceeding earnings limits is a reduction in monthly income, the recapture process ensures that the value of your Social Security benefits is preserved over your lifetime.

- Focus on Lifetime Benefits: Instead of focusing solely on the monthly reduction, consider the overall lifetime benefit you will receive. The earnings test primarily delays when you receive certain portions of your benefits, rather than permanently reducing your total entitlement.

- Professional Advice: It’s always a good idea to consult with a financial advisor or a Social Security expert. They can help you model different scenarios, understand how earnings limits and benefit adjustments might affect your personal financial situation, and make informed decisions about your retirement income strategy.

By understanding these earnings limits, the impact of exceeding them, and the recapture process, you can make more informed decisions about working in retirement and ensure you are maximizing your Social Security benefits effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.