For many, owning a home represents a cornerstone of financial stability and personal aspiration. It’s not just a place to live; it’s often the largest single investment an individual or family will make. However, before you can start browsing listings or envisioning your dream kitchen, a crucial first step is understanding how much you can realistically qualify for a home loan. This figure isn’t arbitrary; it’s a carefully calculated assessment made by lenders based on a multitude of financial factors designed to ensure you can comfortably afford your monthly payments.

Navigating the mortgage landscape can feel daunting, with a lexicon of terms like DTI, PITI, credit scores, and interest rates. Yet, with a clear understanding of what lenders look for and how these elements impact your borrowing power, you can approach the process with confidence and clarity. This article will demystify the qualification process, shedding light on the key determinants, the calculation methods lenders employ, and proactive steps you can take to enhance your eligibility. Our aim is to equip you with the knowledge needed to accurately gauge your borrowing potential, making your journey to homeownership a well-informed and successful one.

Understanding the Core Factors Lenders Evaluate

When you apply for a home loan, lenders don’t just look at a single number; they perform a holistic evaluation of your financial health. Their primary goal is to assess your risk profile – specifically, how likely you are to repay the loan on time and in full. This assessment hinges on several critical factors, each playing a vital role in determining not only if you qualify, but also for how much and at what interest rate.

Your Credit Score and History

Perhaps the most universally recognized indicator of financial responsibility is your credit score. Typically ranging from 300 to 850, this three-digit number summarizes your creditworthiness based on your history of borrowing and repaying debt. Lenders use FICO scores and VantageScores, which are derived from data in your credit reports. A higher score generally indicates a lower risk, making you a more attractive borrower.

Lenders often have minimum credit score requirements, which can vary by loan program (e.g., FHA, VA, Conventional). For conventional loans, a score of 620 is often the baseline, but scores above 740 typically unlock the best interest rates. Beyond the score itself, lenders will scrutinize your credit history for patterns of timely payments, the types of credit accounts you have, the length of your credit history, and any derogatory marks like bankruptcies or foreclosures. A consistent history of responsible credit use signals to lenders that you are a reliable borrower.

Income and Employment Stability

Your income is the foundation of your repayment ability, and lenders need assurance that it’s sufficient, consistent, and reliable. They will require verification of your income, typically through W-2s, pay stubs, tax returns (usually the past two years), and sometimes bank statements. For self-employed individuals, this verification can be more rigorous, often requiring multiple years of business tax returns and profit and loss statements.

Beyond the raw income figures, employment stability is paramount. Lenders prefer to see a steady employment history, ideally with the same employer or within the same industry for at least two years. Frequent job changes, gaps in employment, or a volatile income stream (common for some commission-based or seasonal work) can raise red flags and may require additional explanation or documentation. The goal is to demonstrate a predictable and sustainable income stream that can comfortably cover your potential mortgage payments.

Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is one of the most crucial metrics lenders use. It’s a comparison of your total monthly debt payments to your gross monthly income. There are two types of DTI:

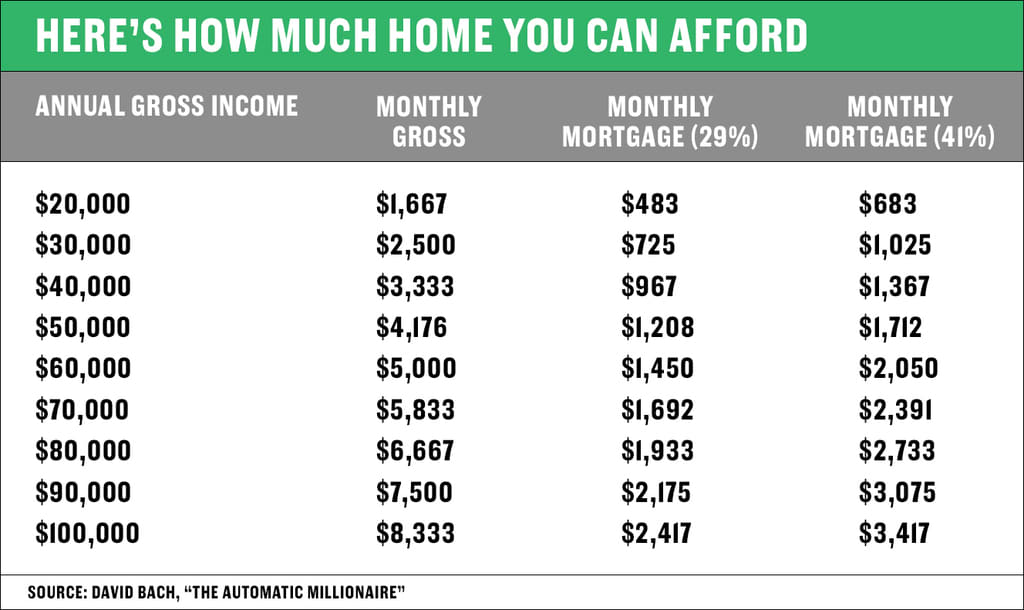

- Front-end DTI (Housing Ratio): This compares your prospective monthly housing expenses (principal, interest, property taxes, homeowner’s insurance, and sometimes HOA fees – collectively known as PITI) to your gross monthly income. Lenders typically look for a front-end DTI of no more than 28%.

- Back-end DTI (Total Debt Ratio): This compares your total monthly debt payments (including your prospective PITI, credit card minimums, car loans, student loans, and other installment debt) to your gross monthly income. Most lenders prefer a back-end DTI of 36% or less, though some programs may allow up to 43% or even 50% for highly qualified borrowers.

A lower DTI indicates that you have more disposable income available to manage your mortgage payments, thus lowering the lender’s risk. Understanding and managing your DTI is fundamental to qualifying for the desired loan amount.

Down Payment and Reserves

Your down payment is the initial sum of money you contribute towards the purchase of your home. It reduces the amount you need to borrow, thereby lowering your monthly payments and potentially securing a better interest rate. While 20% down has historically been the standard to avoid Private Mortgage Insurance (PMI) on conventional loans, many programs now allow for much smaller down payments (e.g., 3-5% for conventional, 3.5% for FHA, 0% for VA and USDA loans).

Beyond the down payment, lenders also like to see financial reserves. These are liquid assets, such as savings, checking accounts, or investment accounts, that could be used to cover mortgage payments or other expenses in case of a temporary income disruption. Lenders typically look for reserves equivalent to 2-6 months of your PITI payments, demonstrating that you have a financial cushion. A larger down payment and robust reserves signal financial strength and stability to lenders.

The Calculation Behind Your Affordability

While the factors above determine if you qualify, lenders then translate your financial profile into a maximum loan amount. This isn’t a simple equation but a multi-faceted assessment that blends industry guidelines with individual circumstances.

The 28/36 Rule and Other Guidelines

The “28/36 Rule” is a classic guideline used by many lenders. It suggests that your monthly housing costs (PITI) should not exceed 28% of your gross monthly income, and your total monthly debt payments (including housing) should not exceed 36% of your gross monthly income. For example, if your gross monthly income is $7,000:

- Front-end (Housing): $7,000 * 0.28 = $1,960 maximum for PITI

- Back-end (Total Debt): $7,000 * 0.36 = $2,520 maximum for total monthly debt

While these are general guidelines, specific loan programs have their own DTI thresholds. FHA loans, for instance, often allow for higher DTI ratios (e.g., 31% front-end, 43% back-end, and sometimes higher with compensating factors). VA loans are even more flexible, focusing heavily on residual income rather than strict DTI. Understanding these program-specific guidelines can help you explore options that might better suit your financial situation.

Principal, Interest, Taxes, and Insurance (PITI)

Your actual monthly mortgage payment is more than just principal and interest. It’s known as PITI:

- Principal: The portion of your payment that goes towards reducing the loan balance.

- Interest: The cost of borrowing money from the lender.

- Taxes: Property taxes levied by your local government. Lenders typically require these to be paid into an escrow account monthly.

- Insurance: Homeowner’s insurance, which protects your home against damage. Also usually paid into escrow.

Additionally, depending on your down payment, you might have:

- Private Mortgage Insurance (PMI): Required for conventional loans with less than 20% down.

- Mortgage Insurance Premium (MIP): Required for FHA loans.

- Homeowners Association (HOA) Fees: If you’re buying a condo or a home in a planned community, these mandatory fees are also factored into your overall housing costs.

Lenders will add up all these components to determine your total monthly housing expense, which then feeds into their DTI calculations. A higher PITI means a larger portion of your income is allocated to housing, reducing the maximum loan amount you can qualify for.

The Role of Interest Rates

Interest rates significantly impact your monthly payment and, consequently, how much you can qualify for. A lower interest rate means a smaller portion of your payment goes towards interest, allowing more to go towards the principal, or simply making the monthly payment more affordable for a given loan amount. Conversely, a higher interest rate will increase your monthly payment for the same loan amount, effectively reducing your overall borrowing capacity.

Interest rates are influenced by market conditions (e.g., Federal Reserve policies), your credit score, the type of loan you choose, and the loan term. Even a seemingly small difference of half a percentage point can translate into thousands of dollars over the life of the loan and significantly alter your monthly budget. It’s crucial to consider prevailing interest rates when estimating your qualification potential and to shop around for the best rate available to you.

Pre-Qualification vs. Pre-Approval: Knowing the Difference

Many aspiring homeowners mistakenly use “pre-qualification” and “pre-approval” interchangeably, but there’s a significant distinction between the two. Understanding this difference is crucial for setting realistic expectations and navigating the home buying process effectively.

What is Pre-Qualification?

Pre-qualification is an informal, preliminary assessment of how much you might be able to borrow. It’s typically based on a brief conversation with a lender or an online questionnaire where you provide verbal or self-reported information about your income, debts, and assets. The lender uses this information to give you an estimated loan amount without verifying any of the details.

- Pros: Quick, easy, no impact on your credit score (usually a “soft” credit pull, if any). Provides a rough idea of affordability.

- Cons: Not a commitment from the lender. It carries little weight with sellers and doesn’t involve a thorough review of your finances. It’s essentially an educated guess.

While a pre-qualification can be a good starting point for your research, it doesn’t give you a strong position when making an offer on a home.

The Power of Pre-Approval

Pre-approval is a much more robust and formal process. With pre-approval, you complete a full mortgage application and provide the lender with actual documentation (pay stubs, W-2s, bank statements, tax returns, etc.) for verification. The lender then conducts a thorough review of your credit report (a “hard” credit pull) and your financial situation. If approved, they issue a pre-approval letter stating the maximum amount they are willing to lend you, often with specific loan terms and interest rates (though rates can change).

- Pros: A strong indication of your borrowing power, taken seriously by sellers and real estate agents. It demonstrates that you are a serious and qualified buyer. Speeds up the closing process once an offer is accepted.

- Cons: Requires more effort and documentation. Involves a hard credit inquiry, which can slightly ding your credit score temporarily.

Having a pre-approval letter in hand is invaluable in a competitive housing market. It allows you to make offers with confidence, knowing exactly what you can afford, and gives sellers assurance that your financing is likely to go through. It truly empowers you in the home buying journey.

Strategies to Boost Your Home Loan Qualification

If your initial assessment or pre-qualification indicates you might not qualify for the desired amount, don’t despair. There are several proactive steps you can take to improve your financial standing and enhance your eligibility for a larger loan or more favorable terms.

Improving Your Credit Profile

Your credit score is dynamic and can be improved over time. Focus on:

- Paying bills on time, every time: Payment history is the most significant factor in your credit score.

- Reducing credit card balances: Aim to keep your credit utilization ratio (the amount of credit you’re using compared to your available credit) below 30%, ideally even lower.

- Avoiding new credit inquiries: Don’t open new credit accounts or apply for new loans in the months leading up to and during your mortgage application process.

- Checking your credit report for errors: Dispute any inaccuracies with the credit bureaus, as these could be negatively impacting your score.

- Keeping old accounts open: A longer credit history is generally better.

These actions, taken consistently, can significantly boost your credit score, making you a more attractive borrower.

Managing Your Debt Effectively

Lowering your Debt-to-Income (DTI) ratio is key to qualifying for a higher loan amount.

- Pay down high-interest debt first: Focus on credit cards and personal loans with high interest rates.

- Avoid taking on new debt: Refrain from financing a new car, furniture, or making large purchases on credit before or during your home loan application.

- Consider consolidating debt: In some cases, consolidating multiple high-interest debts into a single, lower-interest personal loan could reduce your monthly payments and improve your DTI, but be cautious and ensure it truly benefits your overall financial picture.

- Increase your income: While not always immediately feasible, finding ways to legitimately increase your gross monthly income (e.g., a raise, a well-documented side hustle) can also lower your DTI.

Increasing Your Savings and Down Payment

A larger down payment directly reduces the loan amount you need and can also improve your interest rate and eliminate PMI.

- Aggressively save: Create a dedicated savings plan, cut unnecessary expenses, and funnel extra income into your down payment fund.

- Look for down payment assistance programs: Many state and local governments offer programs to help first-time homebuyers with down payment and closing costs.

- Consider gift funds: If family members are willing to help, ensure they follow proper gifting guidelines (e.g., providing a gift letter) to avoid issues with lenders.

- Build up reserves: Having extra funds in savings beyond the down payment demonstrates financial stability.

Exploring Different Loan Programs

Not all mortgages are created equal. Different loan programs cater to various financial situations:

- Conventional Loans: Require good credit, can be flexible with down payment, but typically require PMI with less than 20% down.

- FHA Loans: Government-insured loans with lower credit score requirements and down payments (3.5%), suitable for first-time buyers or those with less-than-perfect credit.

- VA Loans: For eligible veterans, service members, and surviving spouses, offering 0% down payment and no PMI.

- USDA Loans: For low-to-moderate income borrowers in eligible rural areas, also offering 0% down.

Researching these options can reveal a program that aligns better with your current financial standing and potentially allows you to qualify for more.

Taking the Next Steps Towards Homeownership

Once you have a clearer picture of your qualification potential and have taken steps to optimize your financial profile, it’s time to move forward with confidence.

Gathering Your Documentation

Whether you’re going for pre-qualification or pre-approval, having your financial documents organized will streamline the process. Lenders will typically ask for:

- Proof of income: Pay stubs (past 30-60 days), W-2s (past two years), tax returns (past two years for self-employed or those with complex income).

- Bank statements (past 60 days) for all checking and savings accounts.

- Investment account statements (if applicable).

- Statements for all debts: Credit cards, car loans, student loans, etc.

- Photo ID and Social Security card.

Having these documents readily accessible will significantly speed up your application process and reduce stress.

Shopping for the Right Lender

Just as you shop for a home, you should shop for a mortgage lender. Interest rates, fees, and loan terms can vary significantly from one lender to another. Contact multiple lenders—including large banks, credit unions, and mortgage brokers—to compare offers.

- Get quotes from at least three different lenders.

- Compare the Annual Percentage Rate (APR), not just the interest rate. APR includes fees and points, giving you a more accurate picture of the total cost.

- Ask about closing costs and any origination fees.

- Read reviews and seek recommendations to find a lender with good customer service and a track record of closing loans efficiently.

A knowledgeable and responsive lender can make a substantial difference in your home buying experience.

The Importance of Professional Guidance

The home loan process is complex, and navigating it alone can be challenging. Working with experienced professionals can provide invaluable support:

- A reputable mortgage loan officer: They can explain different loan programs, help you understand your qualification limits, and guide you through the application process.

- A trusted real estate agent: They can connect you with reliable lenders, help you find homes within your budget, and represent your interests throughout negotiations.

- A financial advisor (if needed): For complex financial situations or long-term planning, a financial advisor can help you prepare for homeownership and integrate it into your broader financial goals.

By leveraging the expertise of these professionals, you can ensure you’re making informed decisions and are well-supported at every stage of your homeownership journey.

In conclusion, understanding “how much can I qualify for a home loan” is the foundational step towards achieving your dream of homeownership. It’s a comprehensive assessment based on your credit, income, debts, and savings. By proactively managing these financial elements and seeking professional guidance, you can confidently determine your borrowing power and embark on the exciting path to finding your perfect home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.