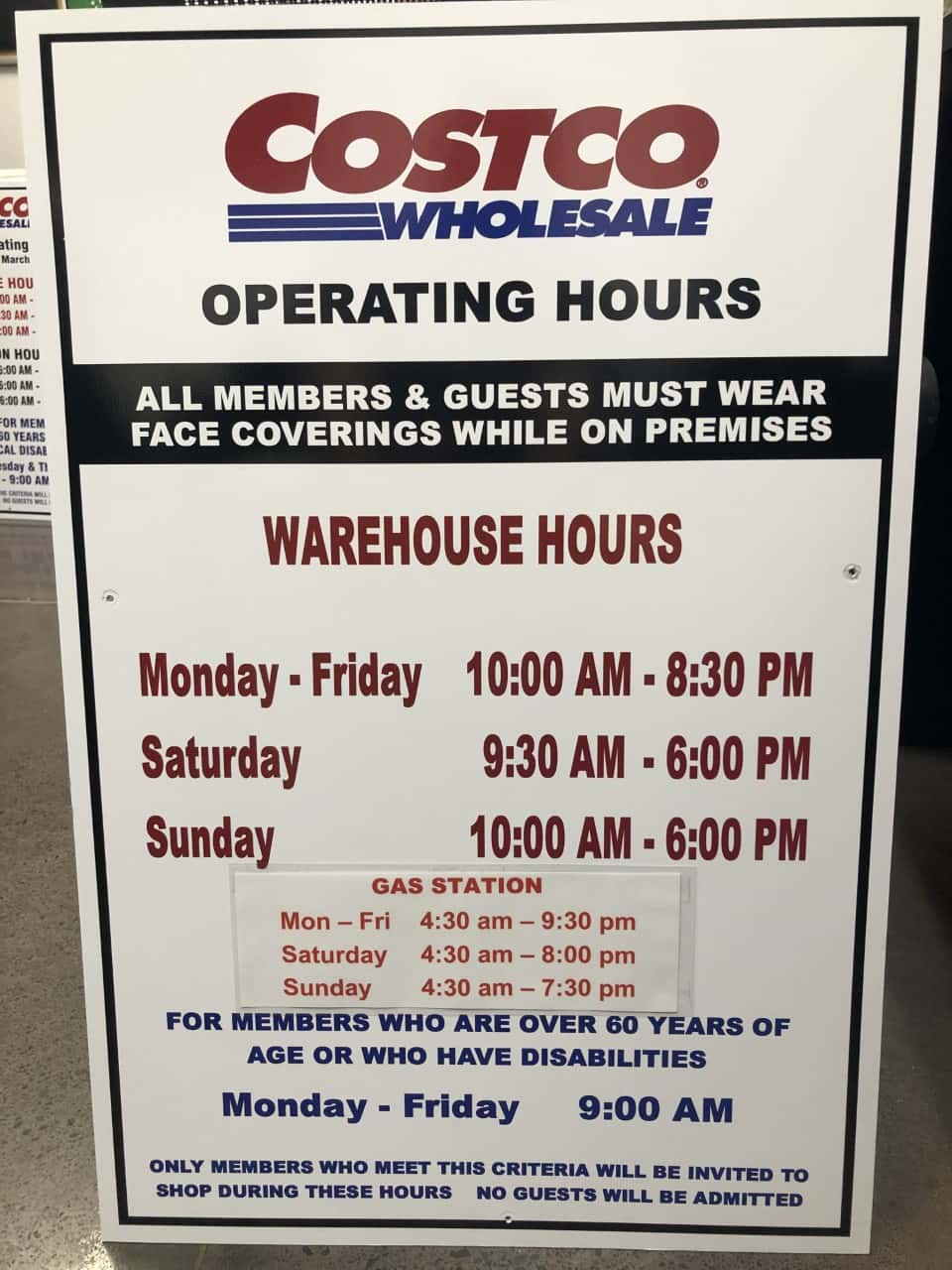

For many consumers, the question “how late is Costco open today?” is the first step in a carefully orchestrated financial ritual. While the surface-level query seeks a window of time—typically ending at 8:30 PM on weekdays and 6:00 PM on weekends—the underlying motivation is rooted in the pursuit of fiscal efficiency. In the landscape of personal finance, a Costco membership is less of a shopping pass and more of a strategic financial tool designed to optimize household expenditures and increase long-term purchasing power.

Understanding the operational nuances of the warehouse giant is essential for anyone looking to master their “Money” niche. From the cost-benefit analysis of the membership fee to the sophisticated math of unit pricing, shopping at Costco represents a sophisticated approach to wealth management and resource allocation.

The Economics of the Warehouse Club: A Strategic Investment

To the uninitiated, paying a fee for the right to spend money seems counterintuitive. However, from a financial perspective, the Costco membership is an entry-level investment in a high-yield savings vehicle. The primary objective is to lower the “cost of living” through high-volume, low-margin retail.

The Membership Fee vs. Annual Savings

Costco offers two primary tiers: the Gold Star and the Executive Membership. At $65 and $130 respectively (as of the most recent adjustments), these fees represent a fixed cost that must be amortized over the course of a year. To determine the ROI (Return on Investment), a savvy shopper must calculate their “break-even point.”

For an Executive Member, who receives a 2% reward on most purchases, the break-even point for the membership upgrade alone is $3,250 in annual spending. If your household spends more than $271 per month at the warehouse, the higher-tier membership pays for itself, effectively making the “club” access a free financial perk.

How Operational Hours Impact Your Household Budget

The limited operating hours of Costco—shorter than many 24-hour supermarkets—are a deliberate financial decision that benefits the consumer. By closing earlier, Costco reduces overhead costs related to labor, utilities, and security. These savings are directly passed on to the member in the form of lower markups.

For the disciplined shopper, the “how late is Costco open” query is a prompt for time management. Aligning your schedule with these hours forces a planned shopping approach, which is a proven method for reducing impulse buys. When you are racing against a 6:00 PM Sunday closing time, you are less likely to browse aimlessly and more likely to stick to a pre-vetted list of financial necessities.

Strategic Shopping: How to Leverage Bulk Buying for Long-Term Wealth

The core of the Costco financial strategy is the “Unit Price Advantage.” In personal finance, the goal is often to lower the cost of goods sold (COGS) for your own household. By purchasing in bulk, members can hedge against inflation and reduce the frequency of high-cost, small-quantity convenience purchases.

The Unit Price Advantage and Inflation Hedging

Inflation erodes purchasing power, but bulk buying allows a consumer to “lock in” current prices for non-perishable goods. When you buy 30 rolls of toilet paper or a gallon of olive oil, you are essentially shorting future price increases.

The key is to look past the “sticker price” and focus on the price per ounce, sheet, or pound. Costco’s business model caps markups at approximately 14-15%, whereas traditional grocery stores may markup items by 25-50%. By understanding these margins, a consumer can better allocate their monthly cash flow toward high-value items that offer the most significant delta between warehouse and traditional retail prices.

Reducing Impulse Spending through Planned Trips

One of the greatest threats to a personal budget is the “convenience tax”—the extra money paid at a local corner store because you ran out of a staple item. By utilizing the warehouse model, you move your household toward a “just-in-case” inventory system rather than a “just-in-time” system.

While the “treasure hunt” atmosphere of Costco (where high-end luxury items are placed near the entrance) is designed to entice, a disciplined financial mind views this as a test of budgetary resolve. Successful “Money-focused” shoppers use the warehouse hours to schedule one or two high-impact trips per month, thereby reducing the “fuel and friction” costs associated with multiple weekly trips to smaller, more expensive retailers.

The Financial Ecosystem of Costco Services

Beyond the aisles of bulk snacks and electronics lies a suite of financial services that can significantly alter a family’s net worth over time. These services are often the most overlooked aspect of the membership’s value proposition.

Gasoline and Insurance: Indirect Savings

For many, the cost of the membership is recovered solely at the gas pump. Costco Gasoline is typically priced several cents below the market average, and it is “Top Tier” certified. For a two-car household, the annual savings on fuel can easily exceed $200-$300, providing a 300% to 500% return on the basic membership fee.

Furthermore, Costco’s partnership with services like insurance providers (home, auto, life) and pet insurance often leverages the collective bargaining power of millions of members to secure rates that individuals could not obtain on the open market. In the context of “Business Finance” for the individual, these are essential optimizations of fixed monthly expenses.

The Executive Membership and Cash Back Optimization

To truly master the financial aspect of the warehouse, one must integrate the Costco Anywhere Visa® Card by Citi. This creates a “stacked” reward system. When an Executive Member uses this card, they can earn up to 4% back on gas (up to a limit), 3% on restaurants and travel, and an additional 2% on Costco purchases (on top of the 2% provided by the Executive Membership itself).

This 4% “rebate” on warehouse spend effectively negates the impact of many state sales taxes, allowing the member to shop at “net-zero” tax in certain jurisdictions. This level of financial optimization is a hallmark of sophisticated personal finance management.

Corporate Transparency and Investor Relations: The “Costco Effect”

For those interested in “Business Finance” and “Investing,” the operating model of Costco (COST) provides a masterclass in corporate stability and shareholder value. The reason the store doesn’t stay open “late” in the traditional sense is deeply tied to its identity as a low-cost leader.

Why Operating Hours Reflect Labor Efficiency and Profitability

Costco pays its employees significantly above the retail industry average. To sustain these wages while keeping prices low, the company must maintain extreme operational efficiency. The limited hours ensure that staff are utilized during peak demand, maximizing “sales per labor hour.”

As an investor or a business-minded consumer, this transparency is reassuring. It demonstrates a company that prioritizes long-term stability over short-term “convenience” gains. The “Costco Effect” refers to the company’s ability to maintain a loyal customer base (90%+ renewal rates) even while raising membership fees or maintaining strict hours, simply because the value proposition is so mathematically sound.

The “Loss Leader” Strategy as a Financial Lesson

The $1.50 hot dog combo and the $4.99 rotisserie chicken are famous examples of loss leaders. These items are sold at a loss or at cost to drive foot traffic. For the financially savvy shopper, these items represent a “subsidy.” By taking advantage of these loss leaders while avoiding the high-margin “impulse” items (like high-end jewelry or seasonal decor unless planned), a consumer can effectively “win” the game against the retailer’s margins.

In conclusion, knowing “how late is Costco open today” is about more than just a clock; it is about respecting the window of opportunity to execute a high-efficiency financial plan. By treating a Costco trip as a strategic business operation—analyzing unit costs, maximizing cash-back rewards, and leveraging bulk-buy hedges—the average consumer can transform a simple grocery run into a significant driver of personal wealth. Whether you are an investor looking at the stock’s stability or a household manager looking to shave 15% off your annual expenses, the warehouse model remains one of the most powerful tools in the modern financial toolkit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.