The transition from a traditional W-2 employee to a freelancer, independent contractor, or small business owner is often hailed as a journey toward freedom. However, that freedom comes with a set of unique financial responsibilities—the most daunting of which is often the quarterly estimated tax system. Unlike employees who have taxes automatically withheld from every paycheck, the self-employed are responsible for calculating and remitting their own taxes to the IRS four times a year.

The United States operates on a “pay-as-you-go” tax system. This means the government expects to receive tax revenue as you earn it throughout the year, rather than in one lump sum every April. Failure to understand this system can lead to significant underpayment penalties and a stressful tax season. This guide will walk you through the mechanics of quarterly taxes, from determining if you owe them to the final click of the “submit payment” button.

Understanding the “Who” and “Why” of Estimated Tax Payments

Before diving into the “how,” it is essential to understand why these payments exist and who is legally required to make them. In the eyes of the IRS, if you are not an employee, you are both the employer and the employee. This means you are responsible for both the income tax and the self-employment tax (which covers Social Security and Medicare).

Who is Required to Pay?

Generally, you must make estimated tax payments if you expect to owe at least $1,000 in taxes for the year after subtracting your withholding and credits. This typically applies to sole proprietors, partners in a partnership, and S corporation shareholders. If you have a “side hustle” while working a full-time job, you may be able to avoid quarterly payments by increasing the withholding on your W-2 job. However, if your business income is substantial, quarterly filings are unavoidable.

The Safe Harbor Rule

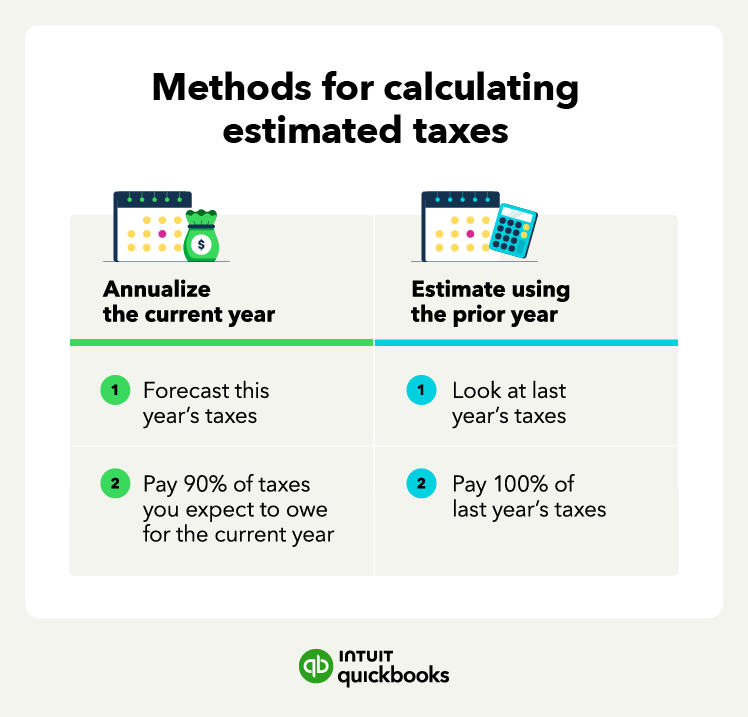

The IRS provides “Safe Harbor” rules to protect taxpayers from penalties, even if they underestimate their actual tax liability. To avoid a penalty, you generally must pay at least 90% of the tax for the current year or 100% of the tax shown on your return for the prior year, whichever is smaller. For high-income earners (those with an adjusted gross income over $150,000), the prior-year requirement increases to 110%. Understanding these benchmarks is the first step in creating a low-stress tax strategy.

Calculating Your Quarterly Tax Obligations

Calculating your taxes when your income fluctuates can feel like shooting at a moving target. However, accuracy is paramount to avoid end-of-year surprises. The goal is not to pay the exact cent owed, but to remain within the safe harbor limits.

Estimating Your Annual Income and Self-Employment Tax

To begin, you must estimate your total expected adjusted gross income (AGI) for the year. This includes not only your business profit but also interest, dividends, and any other taxable income. Once you have a projection of your net profit, you must calculate the self-employment tax. As of the current tax laws, the self-employment tax rate is 15.3%, consisting of 12.4% for Social Security and 2.9% for Medicare. It is important to remember that you can deduct the “employer-equivalent” portion of your self-employment tax in figuring your adjusted gross income, which provides a slight relief on your overall income tax burden.

Using Form 1040-ES and Previous Year Records

The IRS provides Form 1040-ES (Estimated Tax for Individuals) to help you navigate these calculations. This form includes a worksheet that mirrors the standard 1040. If your business is relatively stable, the easiest way to calculate your payments is to look at your previous year’s tax return. Take your total tax liability from the previous year, divide it by four, and pay that amount each quarter. This ensures you meet the 100% safe harbor rule. If your income has increased significantly, you may want to pay more to avoid a massive bill in April, even if you are technically “safe” from penalties.

Step-by-Step Methods for Making Payments

The IRS has modernized its systems significantly over the last decade, making the actual act of paying much simpler than the calculation phase. There are several ways to remit your funds, ranging from digital portals to traditional mail.

The IRS Direct Pay Portal

For most individuals, IRS Direct Pay is the most efficient method. This free service allows you to pay directly from your checking or savings account without any registration. You simply select the “Estimated Tax” reason for payment, choose the correct tax year, and verify your identity using information from a previous year’s tax return. The system provides an immediate confirmation number, which is vital for your record-keeping.

Electronic Federal Tax Payment System (EFTPS)

For business owners who prefer a more robust tracking system or need to schedule payments in advance, the EFTPS is the gold standard. While it requires a one-time enrollment process and a mailed PIN, it allows you to schedule all four quarterly payments at the beginning of the year. This “set it and forget it” approach is excellent for maintaining discipline and ensuring you never miss a deadline due to a busy schedule.

Paying via Mobile App or Mail

If you prefer to handle finances on the go, the IRS2Go mobile app provides a secure gateway to make payments. For those who still prefer paper, you can mail a check or money order along with the payment vouchers found in Form 1040-ES. If you choose this route, it is highly recommended to use certified mail with a return receipt requested. This serves as your legal proof that the payment was sent on time, should the IRS ever claim otherwise.

Critical Deadlines and Avoiding Penalties

Timeliness is just as important as accuracy when it comes to quarterly taxes. The IRS does not follow a standard three-month calendar for these payments, which often confuses new business owners.

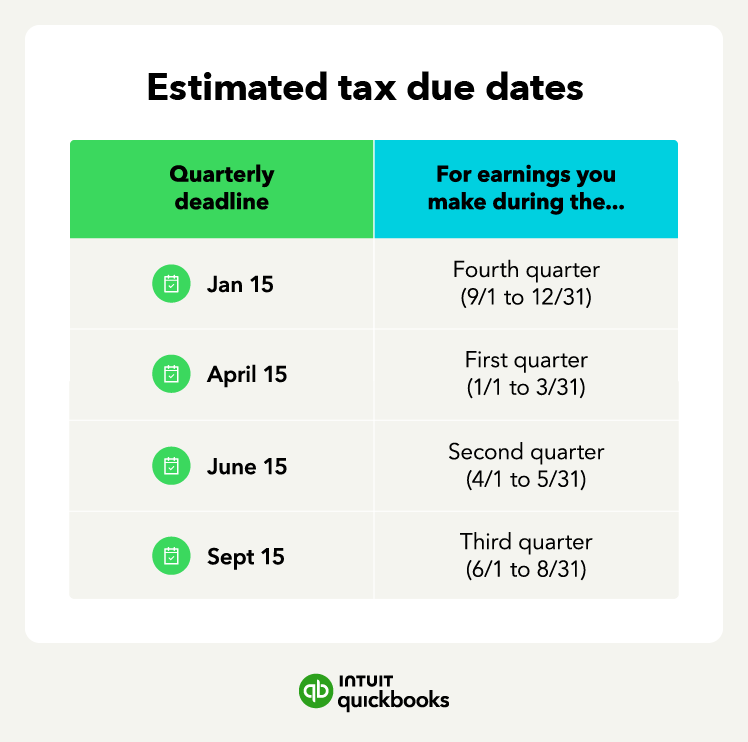

The Four Key Due Dates

The quarterly deadlines are generally as follows:

- April 15: For income earned Jan 1 – March 31.

- June 15: For income earned April 1 – May 31.

- September 15: For income earned June 1 – August 31.

- January 15 (of the following year): For income earned Sept 1 – Dec 31.

Note that if these dates fall on a weekend or a legal holiday, the deadline is pushed to the next business day. It is a common misconception that you only need to pay by the end of the year; however, because the system is “pay-as-you-go,” paying the full amount in January for income earned in March will still result in an underpayment penalty for the missed April deadline.

Underpayment Penalties and How to Avoid Them

The IRS calculates underpayment penalties based on how much you owed and how late the payment was. The penalty is essentially an interest charge on the money you should have paid throughout the year. To avoid this, always aim for the Safe Harbor targets mentioned earlier. If your income is highly seasonal—for example, if you make 80% of your money in the fourth quarter—you can use the “Annualized Income Installment Method” on Form 2210. This allows you to pay smaller amounts early in the year and a larger amount in January without being penalized, provided you can prove when the income was actually received.

Best Practices for Managing Your Tax Cash Flow

The biggest challenge in paying quarterly taxes isn’t the paperwork—it’s having the cash on hand when the deadline arrives. Without a strategy, a $5,000 tax bill can derail a small business’s operations.

Setting Up a Dedicated Tax Savings Account

Financial discipline is the cornerstone of successful tax management. A best practice used by seasoned entrepreneurs is to open a separate high-yield savings account specifically for taxes. Every time you receive a payment from a client, immediately transfer a percentage—typically between 25% and 30%—into that account. By treating this money as “already gone,” you ensure that you never accidentally spend your tax obligations on operating expenses or personal luxuries.

Working with Financial Professionals

While DIY tax software has made progress, nothing replaces the insight of a Certified Public Accountant (CPA) or a qualified tax strategist. A professional can help you identify deductions—such as the home office deduction, health insurance premiums, and retirement account contributions—that lower your overall tax liability. They can also assist in adjusting your quarterly estimates in real-time if your business experiences a sudden pivot or windfall. In the world of finance, the fee paid to a good accountant is often dwarfed by the tax savings and penalty avoidance they provide.

Managing quarterly taxes is a rite of passage for every successful entrepreneur. By understanding your obligations, calculating your liability accurately, and maintaining a disciplined savings strategy, you can turn a potentially stressful administrative burden into a routine part of your business’s financial health. Remember, the goal of the quarterly system isn’t to take more of your money; it’s to ensure that when April 15 rolls around, you aren’t left with a debt you cannot pay.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.