Interest is often described as the “price of time” or the “cost of money.” Whether you are a saver looking to grow your wealth or a borrower seeking to understand the total cost of a loan, knowing how to calculate interest is one of the most vital skills in the realm of personal finance. In an era where financial literacy is directly correlated with long-term stability, understanding the nuances of interest can save you thousands of dollars over a lifetime.

This guide explores the mechanisms behind interest calculation, transitioning from basic concepts to complex financial instruments, ensuring you have the tools to navigate the modern economic landscape.

Understanding the Fundamentals: Simple vs. Compound Interest

Before diving into complex spreadsheets or financial applications, one must understand the two primary ways interest is calculated: simple and compound. These two methods represent the difference between linear growth and exponential acceleration.

Simple Interest: The Basic Formula

Simple interest is the most straightforward method of calculation. It is determined by multiplying the daily interest rate by the principal by the number of days that elapse between payments. Simple interest is most commonly found in short-term personal loans, certain types of auto loans, and basic fixed-deposit accounts.

The formula for simple interest is:

I = P × r × t

- I = Interest

- P = Principal (the original amount borrowed or invested)

- r = Annual interest rate (decimal)

- t = Time (in years)

For example, if you borrow $10,000 at a 5% simple interest rate for three years, you would pay $1,500 in interest ($10,000 × 0.05 × 3). The total repayment would be $11,500. While simple, this method is increasingly rare in long-term modern finance because it does not account for the “interest on interest” phenomenon.

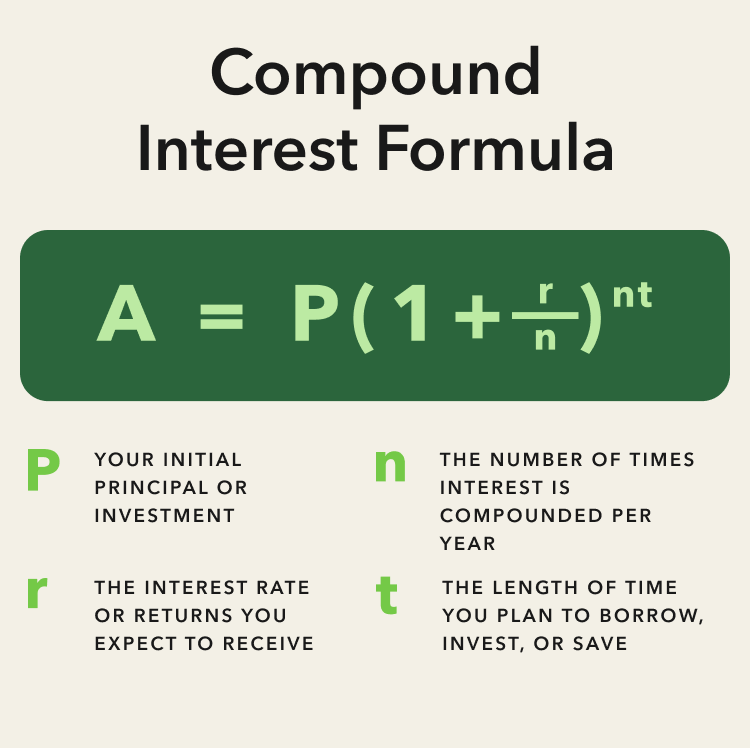

Compound Interest: The Power of Exponential Growth

Compound interest is what Albert Einstein reportedly called the “eighth wonder of the world.” Unlike simple interest, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods. This creates a snowball effect that can work heavily in your favor when saving, or against you when managing debt.

The formula for compound interest is:

A = P(1 + r/n)^(nt)

- A = The total amount of money after interest

- P = Principal

- r = Annual interest rate

- n = Number of times interest is compounded per year

- t = Number of years

If you invested that same $10,000 at a 5% rate compounded monthly (n=12) for three years, you would end up with approximately $11,614.72. The additional $114.72 compared to simple interest is the result of compounding. In the world of money, the frequency of compounding—whether daily, monthly, or annually—can significantly alter the final outcome.

Practical Applications: Mortgages, Loans, and Savings

Understanding the formulas is only the first step. To truly master financial calculation, one must apply these principles to the most common financial products in the market: mortgages, personal loans, and high-yield savings accounts.

Interest on Personal Loans and Credit Cards

Credit cards are perhaps the most complex area for interest calculation because they typically use a method called the “Average Daily Balance.” To calculate this, the credit card issuer tracks your balance every day of the billing cycle, adds them all together, and divides by the number of days in the cycle.

They then apply a daily periodic rate (your APR divided by 365) to that average balance. Because credit cards compound interest—often daily—carrying a balance can lead to a debt spiral where you are paying interest on interest that was charged only weeks prior. This highlights the importance of paying off balances in full to avoid the compounding cost of high-interest debt.

Managing Mortgage Interest and Amortization

A mortgage is usually the largest financial obligation an individual will ever undertake. Unlike a simple loan, mortgages are “amortized.” This means that while your monthly payment remains the same, the proportion of that payment going toward interest versus principal changes over time.

In the early years of a 30-year mortgage, the vast majority of your payment goes toward interest. As the principal balance slowly decreases, the amount of interest charged each month also decreases, allowing more of your payment to go toward the principal. Calculating this requires an amortization schedule. For a homeowner, understanding that an extra payment toward the principal in the early years can shave years off the loan and save tens of thousands in interest is a hallmark of savvy financial management.

Maximizing Returns on Savings and Investment Accounts

On the flip side of borrowing is the world of “Interest Earned.” When you deposit money into a High-Yield Savings Account (HYSA) or a Certificate of Deposit (CD), you are essentially lending money to the bank. To maximize these returns, you must look for accounts that offer frequent compounding.

For instance, a savings account that compounds daily will offer a slightly higher “Effective Annual Yield” than one that compounds monthly, even if the stated interest rate is the same. When evaluating where to place your emergency fund or long-term savings, calculating the total projected yield based on the compounding frequency is essential for wealth optimization.

Advanced Concepts: APR, APY, and the Impact of Inflation

In the financial industry, interest rates are rarely presented as a single, simple number. To compare different financial products accurately, you must understand the distinction between APR and APY, as well as how external factors like inflation affect the “real” value of your money.

Annual Percentage Rate (APR) vs. Annual Percentage Yield (APY)

These two terms are frequently confused, but the difference is crucial.

- APR (Annual Percentage Rate) represents the annual cost of a loan to a borrower, including fees and interest, but it does not account for compounding.

- APY (Annual Percentage Yield) represents the real rate of return on an investment or the real cost of a loan, accounting for the effect of compounding interest.

When you are borrowing (like a car loan), the lender will often highlight the APR. When you are saving, the bank will highlight the APY because it looks higher. A professional approach to money management involves converting all rates to a comparable format to ensure you are getting the best deal. If a loan has a 10% interest rate compounded monthly, its effective APR is actually 10.47%.

The Impact of Inflation on Real Interest Rates

Calculating interest is not just about the numbers on your bank statement; it is about purchasing power. The “Nominal Interest Rate” is the rate stated by your bank. However, the “Real Interest Rate” is the nominal rate minus the rate of inflation.

If your savings account earns 4% interest, but inflation is running at 5%, you are technically losing 1% of your purchasing power every year. When calculating the long-term growth of an investment portfolio or a retirement fund, failing to account for inflation is a common mistake. A truly insightful financial plan calculates interest in “constant dollars” to ensure that the wealth being built will actually be able to sustain the desired lifestyle in the future.

Digital Tools and Strategies for Efficient Calculation

In the modern era, you do not need to do these calculations by hand. However, knowing how to use the available digital tools is a requirement for professional financial management.

Using Financial Calculators and Spreadsheet Functions

Microsoft Excel and Google Sheets are the most powerful tools in a financier’s arsenal. Most interest-related questions can be solved using built-in functions:

=PMT(rate, nper, pv): Calculates the payment for a loan based on constant payments and a constant interest rate.=FV(rate, nper, pmt, [pv]): Calculates the future value of an investment based on periodic, constant payments and a constant interest rate.=IPMT: Calculates the interest payment for a given period of an investment.

By setting up a dynamic spreadsheet, you can model different “what-if” scenarios, such as how increasing your monthly payment by $200 would impact the interest paid over the life of a loan.

Automation Strategies for Debt Reduction

Once you understand how interest is calculated, you can use technology to “game” the system. One popular strategy is the “Debt Avalanche” method. This involves using financial software to identify the debt with the highest interest rate and directing all excess cash flow toward it, regardless of the balance size. Because you are targeting the highest “cost of money” first, this mathematically minimizes the total interest paid over time.

Furthermore, many digital banking platforms now allow for “round-up” features or automated transfers. By calculating the interest you would have paid on a debt and instead automating that amount into a compound-interest-bearing investment account, you flip the script from being a victim of interest to a beneficiary of it.

Conclusion: The Strategic Value of Interest Literacy

Calculating interest is far more than a mathematical exercise; it is a strategic necessity. For the individual, it is the difference between being trapped in a cycle of debt and building a legacy of wealth. By mastering the formulas of simple and compound interest, understanding the nuances of APR versus APY, and leveraging digital tools for precise calculation, you gain control over your financial destiny.

In the world of money, those who do not understand interest are destined to pay it, while those who do understand it are destined to earn it. Whether you are analyzing a mortgage, choosing a savings account, or planning for retirement, always run the numbers. The clarity provided by a precise interest calculation is the foundation of every sound financial decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.