Social Security benefits represent a cornerstone of financial security for millions of Americans, providing a vital income stream during retirement, in cases of disability, and for surviving family members. Understanding how these benefits are calculated is crucial for effective financial planning and ensuring a secure future. The Social Security Administration (SSA) employs a complex but systematic approach to determine the amount an individual receives, based on a lifetime of earnings and specific eligibility criteria. This article delves into the intricacies of this determination process, breaking down the key factors that contribute to the final benefit amount.

The Foundation: Your Lifetime Earnings Record

At the heart of Social Security benefit calculation lies your earnings history. The SSA tracks your earnings throughout your working life, up to the annual limit subject to Social Security taxes. This record forms the basis for determining your primary insurance amount (PIA), which is the benefit you would receive at your full retirement age. The process involves several steps to translate your cumulative earnings into a monthly benefit.

Average Indexed Monthly Earnings (AIME)

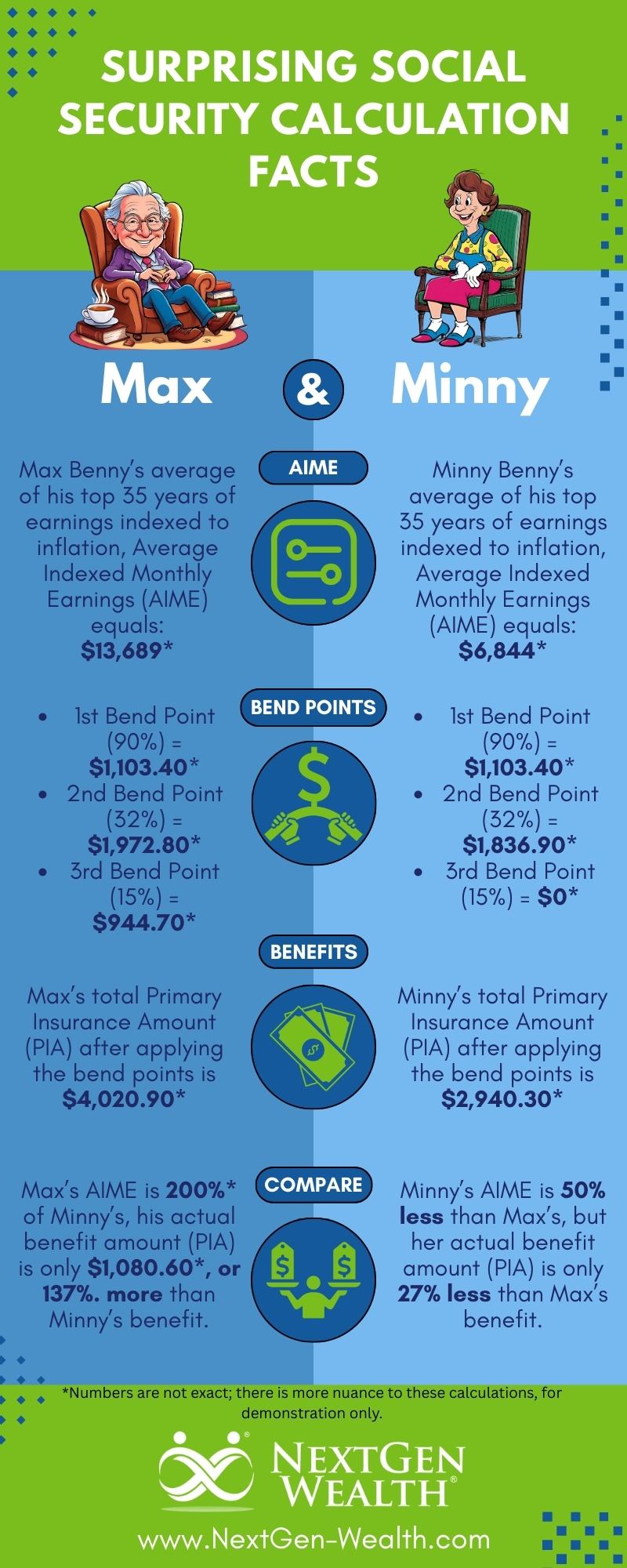

The first major step in calculating your Social Security benefit is determining your Average Indexed Monthly Earnings (AIME). This isn’t simply an average of all the money you’ve ever earned. Instead, the SSA uses a process that “indexes” your past earnings to reflect changes in general wage levels over time. This indexing ensures that your earlier earnings are brought up to more current wage levels, providing a fairer representation of their value relative to today’s economy.

The Indexing Process

Earnings from each year are multiplied by an indexing factor based on the national average wage index for that year. For example, if you earned $20,000 in 1980, that amount would be indexed to its approximate equivalent value in today’s dollars to account for inflation and wage growth. This process is applied to all years up to the year you turn 60. Earnings from age 60 onward are counted at their actual dollar amount.

Selecting the Highest Earning Years

Once your earnings have been indexed, the SSA then selects your highest 35 years of earnings. If you have fewer than 35 years of recorded earnings, the years with zero earnings will be included in the calculation, which will lower your average. This is why consistent work history is important for maximizing Social Security benefits. The total indexed earnings from these 35 years are then summed up.

Calculating the Average

The sum of your highest 35 indexed years of earnings is then divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings (AIME). This AIME is a crucial intermediate figure that represents your average monthly earnings over your working lifetime, adjusted for wage inflation.

The Primary Insurance Amount (PIA)

The AIME is then plugged into a formula to calculate your Primary Insurance Amount (PIA). The PIA is the amount you would receive if you claim benefits at your full retirement age. The PIA formula is progressive, meaning it replaces a higher percentage of earnings for lower-income workers than for higher-income workers. This progressive nature is a key feature of the Social Security system, designed to provide a more substantial replacement rate for those who earned less throughout their careers.

The PIA Formula’s Bend Points

The PIA formula uses “bend points,” which are specific dollar amounts that change annually with inflation. These bend points divide your AIME into three portions. For example, the first portion might be calculated as 90% of the AIME up to the first bend point, the second portion as 32% of the AIME between the first and second bend points, and the third portion as 15% of the AIME above the second bend point.

Examples of PIA Calculation

Let’s consider a hypothetical simplified example. Suppose your AIME is $3,000. Using the current bend points (which are subject to change annually), the calculation might look something like this:

- 90% of the first $1,174 of your AIME = $1,056.60

- 32% of the AIME between $1,174 and $4,720 (your AIME of $3,000 falls within this range) = 32% of ($3,000 – $1,174) = 32% of $1,826 = $584.32

- 15% of your AIME above $4,720 (your AIME is below this, so this portion is $0) = $0

Adding these portions together: $1,056.60 + $584.32 + $0 = $1,640.92. This hypothetical $1,640.92 would be your PIA. It’s important to remember that these bend points and the resulting PIA amounts are adjusted annually to reflect changes in the cost of living and national wage levels.

Factors Influencing Your Benefit Amount

While your lifetime earnings record is the primary determinant of your Social Security benefit, several other factors can significantly influence the actual amount you receive. These factors relate to when you choose to claim benefits, your work history, and other Social Security provisions.

Claiming Age: Early, Full, or Delayed Retirement

The age at which you decide to start receiving Social Security benefits has a direct and substantial impact on your monthly payment. The SSA defines three key claiming ages: early retirement age, full retirement age, and delayed retirement age.

Early Retirement Age

You can begin receiving Social Security retirement benefits as early as age 62. However, claiming benefits before your full retirement age results in a permanently reduced monthly benefit. The reduction is calculated based on the number of months you claim early. For each month before your full retirement age, your benefit is reduced by a fraction of a percent. If you claim at age 62 and your full retirement age is 67, you will receive approximately 30% less per month than if you waited. This reduction is permanent for the duration of your retirement.

Full Retirement Age (FRA)

Your full retirement age is determined by your birth year. It’s the age at which you are entitled to receive 100% of your calculated PIA. For individuals born between 1943 and 1954, the full retirement age is 66. For those born in 1960 or later, the full retirement age is 67. For those born between 1955 and 1959, the full retirement age gradually increases from 66 and 2 months to 66 and 10 months. Claiming at your full retirement age ensures you receive the full benefit amount that your earnings record supports.

Delayed Retirement Credits

Conversely, if you delay claiming benefits beyond your full retirement age, you will earn delayed retirement credits. These credits increase your monthly benefit amount for each month you postpone claiming, up to age 70. For each year you delay, your benefit increases by a certain percentage, capped at age 70. For example, for individuals born in 1943 or later, delaying retirement past their full retirement age up to age 70 results in an 8% increase in benefits per year. This strategy can significantly boost your lifetime income, especially if you have a longer life expectancy.

Maximum Taxable Earnings

The Social Security system is funded by payroll taxes. However, there’s an annual limit on the amount of earnings subject to these taxes. This limit is known as the “maximum taxable earnings.” For 2024, this amount is $168,600. Any earnings above this threshold are not subject to Social Security taxes, nor are they counted in the calculation of your AIME. This means that individuals with very high incomes will not see their Social Security benefits increase beyond a certain point, as their earnings above the taxable maximum do not contribute to their AIME.

Spouse and Survivor Benefits

Social Security benefits are not solely for the individual worker. The program also provides benefits for spouses and surviving family members.

Spousal Benefits

If you are married, your spouse may be eligible to receive benefits based on your earnings record. This can be particularly beneficial if your spouse earned significantly less than you during their working years or if they did not work outside the home. A spouse can receive up to 50% of your primary insurance amount (PIA) if they claim at their full retirement age. If they claim early, their benefit will be reduced.

Survivor Benefits

Upon the death of a worker who paid into Social Security, their eligible surviving spouse, children, and dependent parents may be entitled to survivor benefits. The amount of these benefits depends on the deceased worker’s earnings record and the survivor’s age and relationship to the deceased. These benefits are designed to provide financial support to families who have lost a primary earner.

Other Considerations Affecting Benefit Amounts

Beyond the core calculation of your AIME and PIA, several other aspects of the Social Security system can influence the final benefit amount you receive. These include the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), which primarily affect individuals with pensions from non-covered employment.

Windfall Elimination Provision (WEP)

The Windfall Elimination Provision (WEP) affects individuals who have a pension from work where they did not pay Social Security taxes (e.g., some state and local government jobs, certain foreign employment). If you are eligible for a pension from this type of employment and also qualify for Social Security benefits based on other work, WEP can reduce your Social Security benefit. The intent of WEP is to prevent a “windfall” that could occur if someone receives both a pension from non-covered work and a Social Security benefit calculated using the system’s progressive formula, which disproportionately benefits those with lower average lifetime earnings.

How WEP Impacts Benefits

WEP modifies the PIA formula for those affected. Instead of using the standard 90% factor for the first portion of the AIME, it uses a lower percentage, which is determined by a specific formula. The reduction is capped, meaning your Social Security benefit will not be reduced to zero. The goal is to ensure that the Social Security benefit reflects only the earnings from work where Social Security taxes were paid, rather than being inflated by the presence of a pension from non-covered work.

Government Pension Offset (GPO)

The Government Pension Offset (GPO) is similar in principle to WEP but applies specifically to spouses or surviving spouses receiving Social Security benefits based on another person’s earnings record, while also receiving a pension from a federal, state, or local government job where Social Security taxes were not paid. Under GPO, your Social Security spouse or survivor benefit is reduced by two-thirds of the amount of your government pension.

GPO Calculation Example

For instance, if you are eligible for a $1,000 monthly Social Security survivor benefit but receive a $600 monthly pension from non-covered government employment, your Social Security benefit would be reduced by two-thirds of your pension: (2/3) * $600 = $400. This would leave you with a Social Security survivor benefit of $600 ($1,000 – $400). Like WEP, GPO aims to ensure that benefits are distributed fairly and reflect the intended purpose of each program.

Maximizing Your Social Security Benefits

While the Social Security system is designed to provide a safety net, there are strategic steps you can take to maximize the benefits you receive. These strategies often involve careful planning around claiming age and understanding how different work and earning scenarios can impact your ultimate payout.

Strategic Claiming Age

As discussed earlier, the age at which you claim benefits is paramount. For many, delaying retirement beyond their full retirement age, if financially feasible, can lead to a significantly higher monthly income throughout their retirement years. This is particularly advantageous for individuals with a longer life expectancy. It’s a trade-off: fewer years of receiving a smaller benefit versus more years of receiving a larger benefit.

Maintaining a Strong Earnings Record

A consistent and robust earnings record is fundamental to a higher Social Security benefit. Working for at least 35 years, and ideally earning at or above the maximum taxable earnings in your highest-earning years, will directly contribute to a higher AIME and consequently a higher PIA. Minimizing gaps in employment and striving for well-compensated positions can pay dividends in retirement.

Understanding Spousal and Survivor Benefit Options

For married couples or those who have been married, understanding the intricacies of spousal and survivor benefits is essential. A careful analysis of both partners’ earnings records and potential benefit amounts can lead to optimized claiming strategies. Sometimes, it may be more advantageous for one spouse to claim early while the other delays, or for one spouse to claim their own benefit while the other claims a spousal benefit.

In conclusion, the determination of Social Security benefits is a multi-faceted process rooted in an individual’s lifetime earnings, but also influenced by critical decisions regarding claiming age, and potentially affected by specific provisions for those with non-covered employment pensions. By understanding these components, individuals can better plan for their financial future and make informed choices to maximize their Social Security income throughout retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.