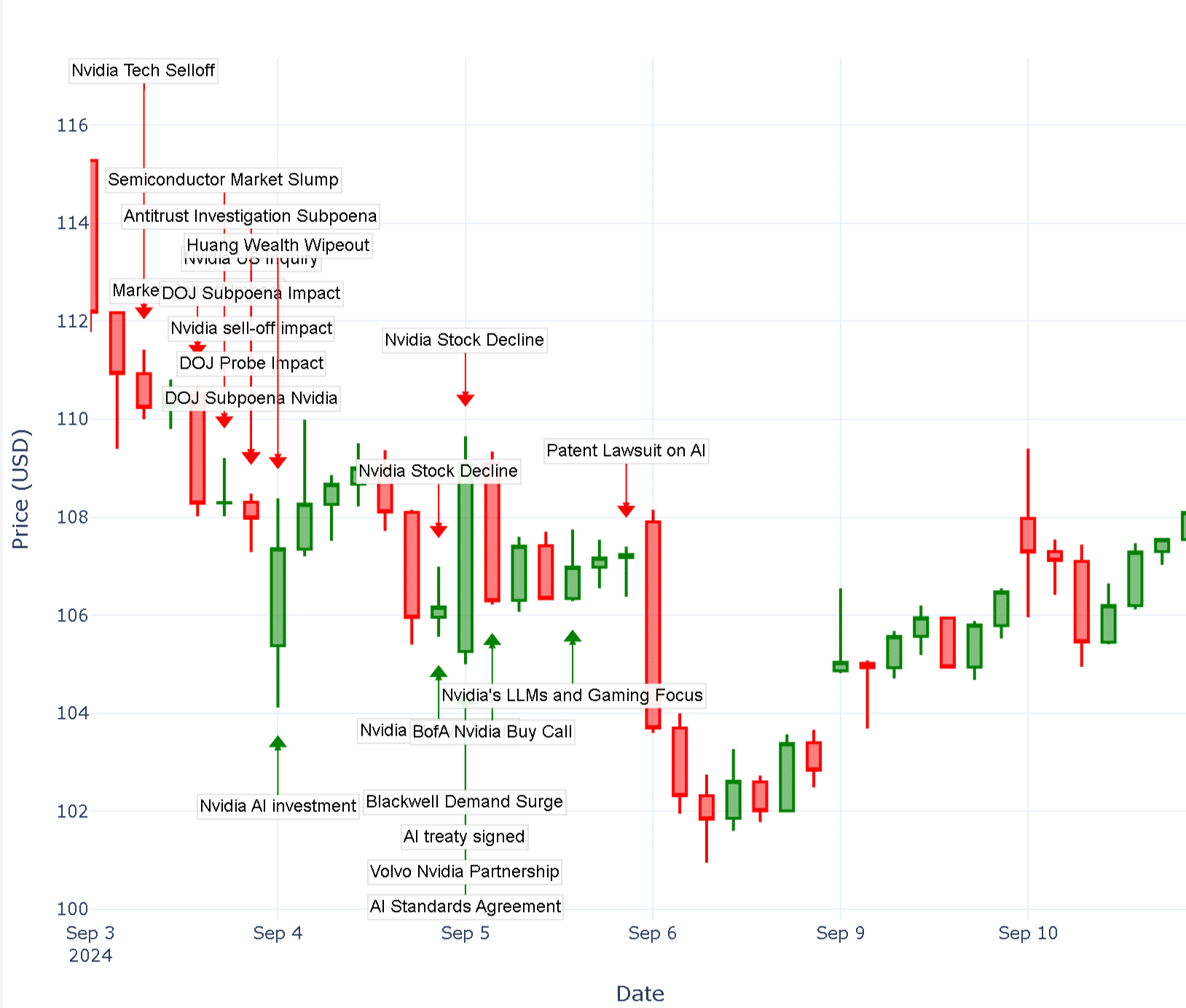

In the modern financial landscape, few companies have captured the collective imagination of the investing public quite like NVIDIA (NVDA). As the primary architect of the hardware powering the artificial intelligence revolution, NVIDIA’s ascent from a niche graphics card manufacturer to a multi-trillion-dollar titan has been nothing short of historic. However, even the most formidable growth engines encounter periods of turbulence. When a stock that has outperformed the S&P 500 by such a wide margin begins to slide, it triggers a wave of anxiety across brokerage platforms and institutional trading desks alike.

To understand why NVIDIA stock is going down, one must look beyond the surface-level headlines. The decline is rarely the result of a single catastrophic failure; rather, it is usually a confluence of macroeconomic pressures, shifting valuation metrics, and the natural ebb and flow of market cycles.

Macroeconomic Pressures and the Interest Rate Environment

The valuation of high-growth technology companies is inextricably linked to the broader macroeconomic climate. While NVIDIA’s business fundamentals may remain strong, external factors often dictate the price investors are willing to pay for those fundamentals.

The Impact of High Interest Rates on Growth Stocks

Central bank policies, particularly those of the Federal Reserve, play a decisive role in the pricing of equity. When interest rates are elevated or expected to remain “higher for longer,” it creates a headwind for growth stocks like NVIDIA. The primary mechanism here is the “discount rate” used in discounted cash flow (DCF) models. Since a large portion of NVIDIA’s perceived value is based on earnings that will occur far in the future, a higher interest rate makes those future dollars less valuable in today’s terms. This leads to a natural contraction in the stock’s price-to-earnings (P/E) multiple, even if earnings stay constant.

Global Economic Uncertainty and Recession Fears

Investors hate uncertainty. When geopolitical tensions rise or manufacturing data suggests a cooling global economy, capital tends to rotate out of high-beta tech stocks and into defensive sectors like utilities or consumer staples. If market participants fear that a recession is on the horizon, they begin to question whether NVIDIA’s “Big Tech” customers—Microsoft, Alphabet, and Meta—will continue their aggressive capital expenditure (CapEx) on AI infrastructure. Any hint of a slowdown in enterprise spending can cause a preemptive sell-off in the semiconductor space.

Valuation Realities and the “Priced to Perfection” Dilemma

One of the most common reasons for a stock decline in a high-performing company is the weight of its own success. When a stock rises as rapidly as NVIDIA’s has, it often reaches a point where it is “priced to perfection.”

Mean Reversion and the Psychology of Profit-Taking

No stock moves in a straight line forever. After a period of parabolic growth, “mean reversion” becomes a significant risk. Professional fund managers and retail investors alike often decide to “take chips off the table” to lock in gains. This institutional profit-taking can create a downward momentum that feeds on itself. When a stock hits a psychological milestone, it often triggers automated sell orders, leading to a temporary decline that has more to do with portfolio rebalancing than the company’s actual health.

Understanding the Price-to-Earnings (P/E) Multiples

NVIDIA often trades at a significant premium compared to the rest of the semiconductor industry. While its growth justifies a higher multiple, there is a limit to how much investors are willing to pay for each dollar of profit. If NVIDIA reports stellar earnings but provides a “forward guidance” that is only slightly above expectations rather than a massive beat, the market often reacts negatively. In a “priced to perfection” scenario, anything less than a monumental surprise is viewed as a disappointment, leading to a valuation reset.

Sector-Specific Headwinds: The AI Hype Cycle and Saturation

NVIDIA is the poster child for the AI era. However, being the leader means the company is also the first to feel the impact of shifting sentiments regarding the viability of artificial intelligence.

Transitioning from Speculative Growth to Sustainable Earnings

We are currently moving from the “infrastructure build-out” phase of AI to the “return on investment (ROI)” phase. Investors are beginning to demand proof that the billions of dollars being spent on NVIDIA’s H100 and Blackwell chips are resulting in profitable software products for the end-users. If the market perceives a gap between the hardware spending and the software revenue generated by AI, a “bubble” narrative begins to take hold. This skepticism puts downward pressure on NVIDIA as investors wait for more concrete evidence of AI’s long-term economic impact.

Capital Expenditure (CapEx) Fatigue Among Big Tech Clients

NVIDIA’s revenue is heavily concentrated among a few “Hyperscalers.” If companies like Amazon or Meta signal in their earnings calls that they are reaching a plateau in their data center investments, NVIDIA’s stock will suffer. The fear of “CapEx fatigue”—where companies slow down their purchasing to digest the hardware they’ve already bought—is a recurring theme that keeps tech investors on edge. When these giants hint at fiscal discipline, the semiconductor supply chain is the first to feel the chill.

Production Constraints and Competitive Incursions

While NVIDIA dominates the market share for AI training chips, it does not operate in a vacuum. Internal execution and external competition are constant factors in stock price fluctuations.

Production Delays and the Blackwell Architecture Rollout

The semiconductor industry is notoriously complex. Any news regarding production delays, particularly with the new Blackwell architecture, can send shockwaves through the stock price. If reports surface suggesting design flaws or supply chain bottlenecks at fabrication partners like TSMC, investors bake that risk into the stock immediately. Delays mean deferred revenue, and in a high-growth environment, deferred revenue is often treated as lost revenue by impatient traders.

Increasing Competition and Market Share Protection

NVIDIA currently enjoys a near-monopoly in high-end AI chips, but the “moat” is being challenged. Competitors like AMD are releasing increasingly competitive hardware, and companies like Google and Amazon are developing their own in-house custom silicon (ASICs) to reduce their reliance on NVIDIA. While NVIDIA remains the gold standard, the mere threat of losing a few percentage points of market share can lead to a contraction in its valuation multiple. Investors are constantly monitoring whether NVIDIA can maintain its industry-leading margins in the face of cheaper alternatives.

Technical Analysis and Market Mechanics

Finally, the movement of NVIDIA’s stock is often influenced by the mechanics of the stock market itself, independent of the company’s business operations.

Resistance Levels and Moving Averages

For many institutional traders, the decision to buy or sell is driven by technical indicators. If NVIDIA’s stock price breaks below a key “support level,” such as the 50-day or 200-day moving average, it can trigger a wave of algorithmic selling. These technical “breakdowns” often cause the stock to go down even if there is no negative news. Conversely, the stock may face “resistance” at previous all-time highs, where a large number of sellers are waiting to exit their positions.

The Role of Institutional Rebalancing and ETF Flows

As one of the largest companies in the world by market cap, NVIDIA is a massive component of major indices like the S&P 500 and the NASDAQ-100. When pension funds or large ETFs (Exchange Traded Funds) need to rebalance their portfolios to maintain specific sector weightings, they may be forced to sell NVIDIA shares regardless of their outlook on the company. Additionally, if there is a general outflow of capital from tech-focused ETFs, NVIDIA—as a top holding—will naturally see its price decline as the fund liquidates shares to meet redemptions.

Conclusion

The downward movement of NVIDIA stock is rarely a sign of a company in distress. Instead, it is usually the result of the market attempting to find a “fair value” in an environment of high expectations, shifting interest rates, and evolving technology cycles. For the long-term investor, these periods of decline represent the “volatility tax” paid for participating in one of the greatest wealth-creation stories of the 21st century.

Understanding that NVIDIA is sensitive to macroeconomic shifts, client spending habits, and technical market levels allows investors to view price drops through a lens of logic rather than fear. While the “AI gold rush” continues, the path for the leading shovel-seller will inevitably include peaks and valleys. Monitoring these financial indicators—valuation multiples, CapEx trends, and interest rate trajectories—is essential for anyone looking to navigate the complex journey of NVIDIA’s stock.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.