Navigating the landscape of personal finance often involves understanding a myriad of terms and entities, and among the most crucial for anyone with outstanding debt is the “loan servicer.” While many people are familiar with their original lender – the bank or institution that initially disbursed the funds – fewer fully grasp the distinct role of a loan servicer. Yet, knowing who your loan servicer is profoundly impacts how you manage your debt, from making payments to addressing financial hardships. This article delves into the critical distinction between lenders and servicers, explains why identifying your servicer is paramount, and provides practical, step-by-step methods to pinpoint this essential entity for various types of loans. Understanding this aspect of your financial obligations is not merely an administrative detail; it’s a fundamental step towards effective debt management and financial empowerment.

Understanding the Role of a Loan Servicer

The relationship between a borrower and their debt is often more complex than a simple transaction with a single entity. Behind every loan lies a system involving various players, each with a specific function. At the heart of daily loan management is the loan servicer, an entity whose responsibilities are distinct from – though often confused with – the original lender.

What is a Loan Servicer?

A loan servicer is the company responsible for handling the day-to-day administration of your loan account. This includes a broad spectrum of activities such as processing your monthly payments, managing your escrow account (for mortgages), communicating with you about your loan, and maintaining your payment history. They are the primary point of contact for any questions, concerns, or adjustments related to your loan once it has been originated. While the original lender might have funded your loan, the servicer ensures that the loan agreement is properly executed and that you, the borrower, fulfill your obligations according to the terms. They track balances, apply payments, calculate interest, and often handle late payments or defaults. In essence, the loan servicer acts as the operational arm that keeps your loan account active and updated.

Servicer vs. Lender: The Key Distinction

To truly grasp the servicer’s role, it’s vital to differentiate it from the lender. The lender is the financial institution that initially provided you with the money, taking on the financial risk and holding the note (the legal document promising repayment). This could be a bank, credit union, or even the federal government for student loans. They are the ones who approved your application and disbursed the funds.

The servicer, on the other hand, is the company contracted to manage the loan on behalf of the lender (or the loan owner, which might be an investor). Often, the original lender might also be the servicer, especially for smaller, local institutions. However, it’s very common for loans, particularly mortgages and student loans, to be sold to investors or transferred to a third-party servicing company shortly after origination. When a loan is sold or transferred, the new owner (investor) or a designated servicer takes over the management. You, as the borrower, are legally obligated to repay the loan, regardless of who owns or services it. The key takeaway is that while the lender owns the debt, the servicer handles all the administrative interactions with you.

Why Does it Matter?

Knowing your loan servicer is not just a matter of bureaucratic detail; it’s fundamental to effective financial management. Your servicer is who you contact for every critical aspect of your loan:

- Making Payments: They provide the address, account numbers, and online portals for payment.

- Account Inquiries: Questions about your balance, interest rates, or payment history are directed to them.

- Payment Assistance: If you face financial hardship, your servicer is the one to discuss options like deferment, forbearance, or loan modifications.

- Escrow Management: For mortgages, they manage your property taxes and insurance payments.

- Tax Information: They issue statements like Form 1098 (Mortgage Interest Statement) or student loan interest paid.

Without knowing your servicer, you effectively lose control over your loan, risking missed payments, late fees, and potential damage to your credit score. It’s the essential link between you and the ongoing obligations of your debt.

Why You Might Need to Find Your Loan Servicer

There are numerous practical and critical situations that necessitate knowing precisely who your loan servicer is. Proactively identifying this entity can save you time, stress, and potential financial penalties.

Making Payments and Account Management

The most straightforward reason to know your loan servicer is to fulfill your primary obligation: making timely payments. Each servicer has specific channels for payment—whether it’s an online portal, a physical mailing address, or automated phone systems. Without this information, you wouldn’t know where to send your money, potentially leading to missed payments, late fees, and negative marks on your credit report. Beyond just making payments, your servicer’s online portal or customer service line is where you access your account details, track your payment history, view your current balance, and understand the specifics of your loan terms. This ongoing account management is impossible without knowing your servicer.

Seeking Payment Assistance or Forbearance

Life can present unexpected financial challenges, from job loss to medical emergencies. When these situations impact your ability to make loan payments, your loan servicer is the first and only point of contact for exploring relief options. Servicers are equipped to discuss possibilities such as deferment (temporarily postponing payments), forbearance (temporuding a pause or reduction in payments), or even loan modification programs (altering the terms of your loan to make it more affordable). If you don’t know your servicer, you cannot access these crucial safety nets, potentially escalating a temporary hardship into a permanent financial crisis or default.

Refinancing or Loan Modifications

When you decide to refinance your loan to secure a lower interest rate, change your loan terms, or consolidate multiple debts, your new lender will need detailed information about your current loan. This often involves contacting your existing loan servicer to obtain payoff statements, verify balances, and confirm payment history. Similarly, if you’re pursuing a loan modification directly with your current loan, such as converting an adjustable-rate mortgage to a fixed-rate one, all discussions and paperwork will go through your servicer. Knowing who they are streamlines this process significantly.

Resolving Disputes or Errors

Mistakes can happen. You might find an incorrect charge on your statement, dispute a late fee you believe was applied in error, or question the way a payment was allocated. All these issues must be addressed directly with your loan servicer. They have the records and the authority to investigate and rectify discrepancies. Attempting to resolve such matters with the original lender, especially if they are not the servicer, will likely result in being redirected and delaying resolution.

Tax Season Information

Each tax season, borrowers often need specific information related to their loan interest payments for tax deductions. For instance, mortgage interest paid is typically reported on Form 1098, which is issued by your loan servicer. Similarly, student loan interest paid is also often tax-deductible. Without knowing your servicer, you won’t know where to retrieve these vital tax documents, potentially missing out on eligible deductions. Your servicer is the official source for accurate annual statements reflecting interest paid and other relevant tax-related data.

Methods for Identifying Your Loan Servicer

Identifying your loan servicer might seem daunting, especially if your loan has changed hands since origination. However, there are several reliable methods to pinpoint this crucial entity, regardless of the loan type.

Checking Recent Statements and Correspondence

The most straightforward method to identify your loan servicer is to examine any recent mail or electronic communications related to your loan. Loan servicers are legally required to send regular statements detailing your loan balance, payments made, and upcoming due dates. These statements will prominently display the servicer’s name, logo, contact information, and often a customer service number or website. If you’ve just received your loan, look for the welcome packet or initial correspondence from the company that will be managing your account. For digital-savvy borrowers, check your email for notifications from your loan account, as many servicers opt for paperless billing and communication.

Online Account Portals and Lender Websites

If you initially set up an online account with your original lender, log in and navigate to your loan details. Sometimes, even if the loan has been transferred, the original lender’s site might provide a link or information directing you to the new servicer. More commonly, if your loan has been sold, you would have received notification to create an account with the new servicer. Visiting the website you usually use to make payments is a strong indicator of who your current servicer is.

Credit Reports

Your credit report is a comprehensive record of your financial obligations, including all active loan accounts. Each loan listed on your credit report will typically include the name of the lender or servicer reporting the account. You can obtain a free copy of your credit report annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Carefully review each loan entry for the “Creditor Name” or “Company Reporting” field, which should indicate your loan servicer. This method is particularly effective if you suspect your loan has been transferred and you haven’t received direct notification.

Specific Loan Type Resources

Certain types of loans have centralized databases designed to help borrowers identify their servicers:

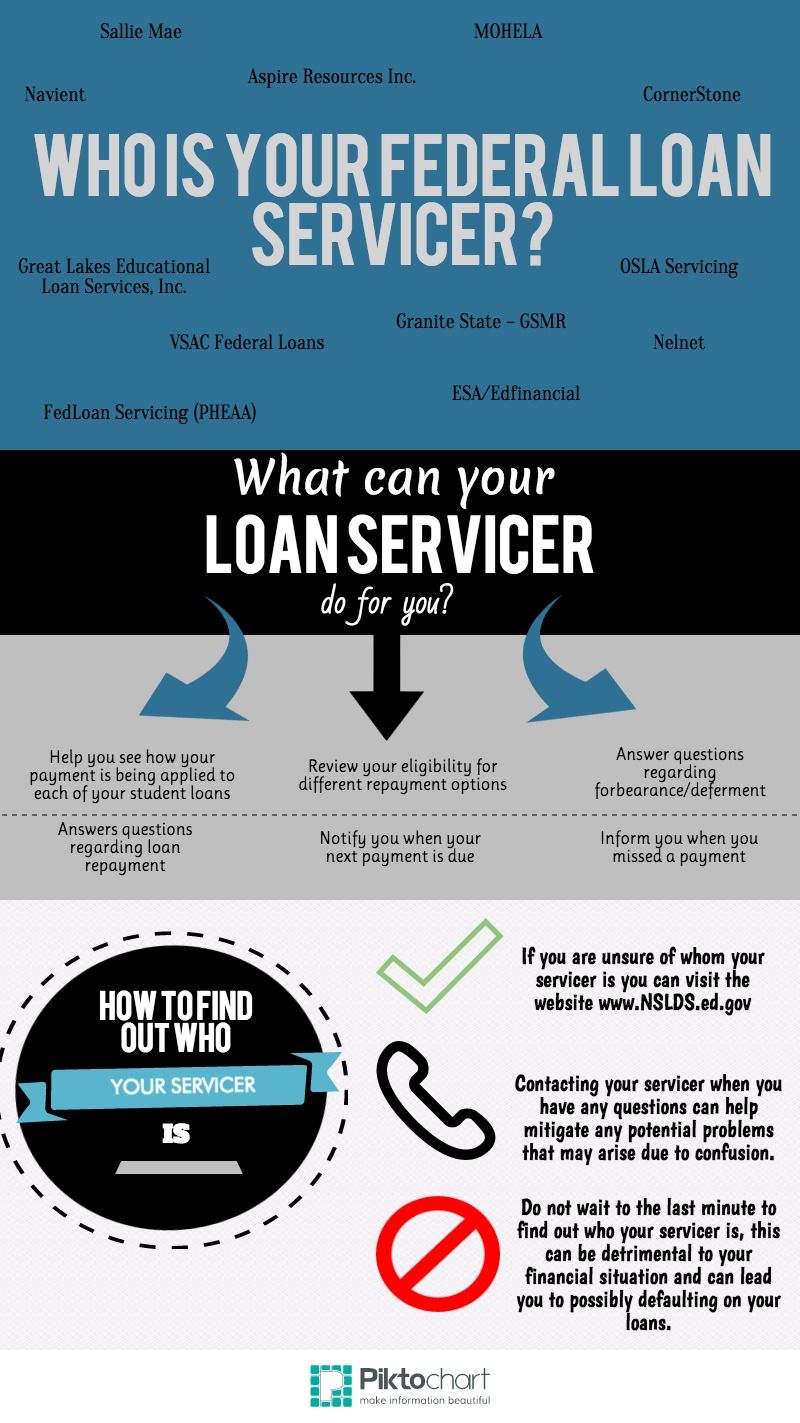

National Student Loan Data System (NSLDS / StudentAid.gov) for Federal Student Loans

For federal student loans, the National Student Loan Data System (NSLDS), now integrated into StudentAid.gov, is the definitive resource. By logging in with your FSA ID, you can view a comprehensive list of all your federal student loans, including the original lender, current balance, and crucially, the name and contact information of your current servicer(s). This is an invaluable tool for federal student loan borrowers, as loans are often consolidated or transferred between different federal servicers.

MERS (Mortgage Electronic Registration Systems) for Mortgages

For mortgages, the Mortgage Electronic Registration Systems (MERS) can be a helpful resource. MERS is a national electronic registry that tracks the ownership and servicing rights of mortgage loans in the United States. While MERS primarily tracks the current owner of the mortgage (the investor), their website sometimes offers a “MERS Servicer ID Search” feature which can help identify the servicer if your loan is registered with them. You’ll typically need your loan number or property address. It’s worth noting that not all mortgages are registered with MERS, but it’s a valuable avenue for those that are.

Contacting Your Original Lender

If all else fails, and you’re still unable to identify your loan servicer, reach out to the original lender who disbursed your loan. They are legally obligated to inform you if your loan has been sold or transferred and provide you with the contact information for your new servicer. Have your original loan documents and account number ready to facilitate the inquiry. While they may no longer own or manage your loan, they initiated the process and should be able to guide you.

What to Do Once You’ve Found Your Loan Servicer

Once you’ve successfully identified your loan servicer, the immediate next steps are crucial for establishing effective communication, managing your account efficiently, and maintaining control over your financial obligations. This proactive engagement will prevent future confusion and ensure a smoother repayment journey.

Setting Up Online Access

The very first action you should take is to set up an online account with your loan servicer, if you haven’t already. Most modern servicers offer robust online portals that serve as a central hub for managing your loan. Through this portal, you can:

- View your current balance and payment history.

- Access electronic statements and tax documents (like Form 1098).

- Enroll in auto-pay (often a requirement for interest rate reductions on some loans).

- Make one-time payments.

- Update your contact information.

- Communicate securely with customer service.

Establishing online access provides convenience, transparency, and often, more efficient communication than traditional mail or phone calls.

Understanding Your Account Details

After gaining access, take the time to thoroughly review all your loan details. This includes:

- Loan balance: Confirm that the amount matches your records.

- Interest rate: Understand if it’s fixed or variable, and what the current rate is.

- Loan terms: Review the repayment period, any fees, and specific conditions.

- Payment due date and amount: Ensure you know exactly when and how much to pay.

- Escrow details (for mortgages): Understand what your escrow payments cover (taxes, insurance) and how those funds are managed.

- Options for hardship: Familiarize yourself with the servicer’s policies regarding deferment, forbearance, or modification options, even if you don’t need them immediately.

A clear understanding of these details empowers you to make informed decisions and detect any discrepancies early.

Communicating Effectively

Your loan servicer is your primary point of contact for anything related to your loan. When you need to communicate:

- Be prepared: Have your account number and relevant details ready before calling or sending a message.

- Be clear and concise: State your query or issue plainly.

- Keep records: Document the date, time, and name of the representative you spoke with, along with a summary of the conversation. If communicating in writing (email or secure message through the portal), save copies. This is invaluable if a dispute arises later.

- Follow up: If you’re expecting an action or response, don’t hesitate to follow up if you don’t hear back within the promised timeframe.

Effective communication minimizes misunderstandings and ensures your concerns are addressed promptly.

Managing Your Payments

Now that you know who your servicer is and how to access your account, focus on efficient payment management:

- Consider auto-pay: Setting up automatic payments directly from your bank account can prevent missed payments and late fees. Some servicers even offer a slight interest rate reduction for enrolling in auto-pay.

- Understand payment allocation: Know how your payments are applied (e.g., towards interest first, then principal).

- Explore extra payments: If financially feasible, understand how to make additional payments and specify that they should be applied directly to the principal to accelerate debt repayment.

Proactive payment management is key to minimizing interest paid and achieving debt freedom sooner.

Common Challenges and Best Practices

While identifying and managing your loan servicer is a critical step in personal finance, borrowers may encounter several challenges. Being aware of these potential pitfalls and adopting best practices can significantly streamline your debt management journey.

Loan Transfers and Sales

One of the most frequent challenges borrowers face is when their loan is sold or transferred from one servicer to another. This is a common practice in the financial industry, particularly for mortgages and student loans. When a transfer occurs:

- You must be notified: Federal law typically requires servicers to notify you in writing about a transfer at least 15 days before the effective date, providing information about the new servicer and where to send payments.

- New account, new rules: The new servicer will have its own payment portal, customer service contacts, and sometimes slightly different processes.

- Potential for confusion: Payments might be sent to the old servicer mistakenly, or communication might be temporarily disrupted.

Best Practice: Always open and read all loan-related correspondence. Immediately update your records with the new servicer’s information, set up a new online account, and verify that your payment method (especially auto-pay) has been correctly transferred or re-established. Keep copies of both the old and new servicer’s notifications.

Avoiding Scams and Misinformation

Unfortunately, the financial services sector is ripe for scams, and loan servicing can be a target. Scammers may impersonate legitimate servicers or offer “debt relief” services that are fraudulent.

- Red flags: Be wary of unsolicited calls or emails demanding immediate payment, asking for personal information beyond what a legitimate servicer would know, or promising unrealistic outcomes (e.g., guaranteed loan forgiveness for a fee).

- Verify everything: If you receive a communication that seems suspicious, do not respond directly. Instead, contact your known loan servicer using the official contact information from their website or your loan statements to verify the legitimacy of the communication.

Best Practice: Always initiate contact yourself using verified information. Never give out sensitive personal or financial details to unsolicited callers or emailers. Trust your instincts; if something feels off, it probably is.

Maintaining Accurate Records

The onus is largely on the borrower to maintain accurate records of their loan interactions. This practice can be invaluable in resolving disputes or confirming information.

- Digital and physical copies: Keep copies of all loan documents: the original promissory note, welcome letters, monthly statements, payment confirmations, and any correspondence related to changes in terms or servicer transfers. Store these in an organized manner, both digitally (scanned copies) and physically.

- Communication log: As mentioned earlier, maintain a log of all interactions with your servicer, including dates, names of representatives, and a summary of discussions.

Best Practice: Create a dedicated folder (digital or physical) for each loan. Review statements regularly against your own payment records to catch errors promptly. This diligence can be your best defense against administrative oversights or disputes.

Proactive Monitoring of Your Loans

Your loans are dynamic financial products, and proactive monitoring is key to responsible debt management.

- Regular credit report checks: Periodically check your credit report (at least annually) to ensure all your loan accounts are reported accurately by the correct servicer and that there are no unexpected entries or errors.

- Stay informed about changes: Keep an eye on your servicer’s website or newsletters for announcements regarding new policies, payment options, or potential changes to your loan terms.

- Understand your rights: Familiarize yourself with borrower rights under federal and state laws, particularly concerning loan servicing. Organizations like the Consumer Financial Protection Bureau (CFPB) offer valuable resources.

Best Practice: Treat your loans as ongoing relationships that require attention. Don’t just set up auto-pay and forget about them. Regular oversight ensures you remain in control and can adapt to any changes effectively.

In conclusion, understanding and identifying your loan servicer is a foundational element of sound personal finance. It empowers you to manage your payments, access assistance, resolve issues, and ultimately navigate your debt repayment journey with confidence and clarity. By applying the methods and best practices outlined above, you can transform a potentially confusing aspect of financial management into a clear path towards financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.