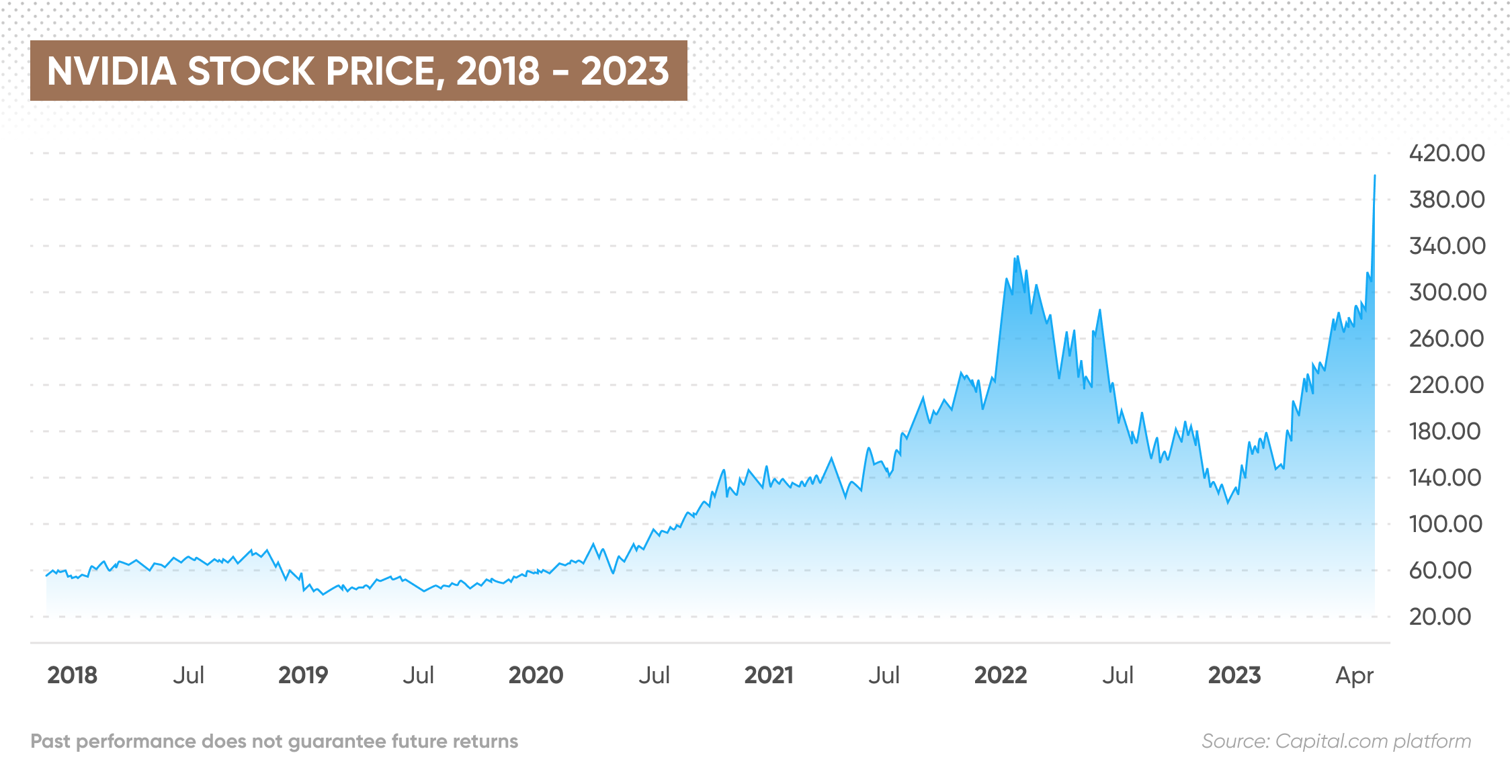

In the history of the modern stock market, few companies have captured the collective imagination of investors quite like Nvidia (NVDA). Once known primarily as a niche provider of graphics processing units (GPUs) for gamers, the Silicon Valley giant has transformed into the primary engine of the global Artificial Intelligence (AI) revolution. As its market capitalization flirts with the valuations of titans like Microsoft and Apple, long-term investors are faced with a pivotal question: where will Nvidia stock be in five years?

Predicting the trajectory of a hyper-growth stock requires a deep dive into financial fundamentals, market psychology, and the sustainability of high-margin revenue streams. While the past three years have seen unprecedented gains, the next five will be defined by Nvidia’s ability to defend its “moat” and transition from a hardware provider to a holistic AI ecosystem provider.

Analyzing the Fundamental Drivers of Nvidia’s Market Valuation

The backbone of any long-term stock projection lies in the company’s ability to generate consistent, growing cash flows. For Nvidia, the narrative has shifted from consumer hardware to enterprise infrastructure on a massive scale.

The Dominance of Data Centers and AI Infrastructure

The most significant contributor to Nvidia’s valuation over the next five years will be its Data Center segment. We are currently in the midst of a multi-trillion-dollar transition from general-purpose computing (CPUs) to accelerated computing (GPUs). Companies, governments, and research institutions are racing to build out the infrastructure required to train and deploy Large Language Models (LLMs) and generative AI applications.

Nvidia’s “H100” and “Blackwell” architectures are not just products; they are the gold standard of the industry. By 2029, the demand for these chips is expected to evolve from initial training to “inference”—the stage where AI models are used to provide answers and perform tasks. If Nvidia can maintain its dominance in the inference market, its revenue floor will remain significantly higher than its historical averages, providing a sturdy foundation for the stock price.

Diversification into Automotive and Omniverse Segments

To justify a higher valuation five years from now, Nvidia must prove it is not a “one-trick pony” dependent solely on LLMs. The automotive sector, specifically autonomous driving, represents a massive untapped revenue stream. Nvidia’s DRIVE platform is being integrated by major automakers to power next-generation self-driving features.

Furthermore, the “Omniverse”—Nvidia’s platform for industrial digitalization—aims to revolutionize how factories are designed and products are manufactured. By creating digital twins of physical systems, Nvidia is positioning itself as a central player in the Fourth Industrial Revolution. If these segments contribute even 15–20% of total revenue by 2029, it would significantly de-risk the investment thesis.

Financial Metrics and Competitive Moats

From an investing standpoint, a stock is only as good as the company’s ability to protect its profit margins. Nvidia currently enjoys gross margins that are the envy of the semiconductor world, often exceeding 70%.

Margin Sustainability and Pricing Power

One of the primary concerns for investors over a five-year horizon is margin compression. As competitors like AMD and Intel release their own AI chips, and as big tech firms (Google, Amazon, Meta) develop in-house silicon, will Nvidia be forced to lower prices?

Nvidia’s secret weapon is not just the chip, but the software—specifically the CUDA (Compute Unified Device Architecture) platform. Developers have spent nearly two decades building software on CUDA, creating a powerful “lock-in” effect. This software ecosystem allows Nvidia to maintain premium pricing. For the stock to reach new heights by 2029, Nvidia must continue to demonstrate that its integrated hardware-software stack offers a lower “Total Cost of Ownership” (TCO) than cheaper, less efficient alternatives.

Assessing the Competitive Landscape and Market Share Risks

In the next five years, the competitive landscape will undoubtedly sharpen. We are likely to see a “good enough” tier of AI chips emerge for simpler tasks. However, Nvidia’s strategy of an annual product release cycle—moving from Hopper to Blackwell to Rubin architectures—is designed to keep the competition perpetually one step behind.

Investors should monitor Nvidia’s “Capital Expenditures” (CapEx) trends among its largest customers (the “Hyperscalers”). If Microsoft and Meta continue to increase their AI-related spending through 2027, Nvidia’s stock will likely continue its upward trajectory. The risk lies in a “digestion period” where customers slow down purchases to optimize the hardware they have already bought.

Macroeconomic Factors and Regulatory Headwinds

No stock exists in a vacuum. The broader economic environment will play a crucial role in determining Nvidia’s 2029 valuation.

Interest Rates and the Cost of Capital

Growth stocks, particularly those in the technology sector, are sensitive to interest rate fluctuations. In a high-rate environment, the “discount rate” applied to future earnings is higher, which can compress price-to-earnings (P/E) multiples.

However, Nvidia has the advantage of a fortress-like balance sheet. With billions in cash and minimal debt, the company is less sensitive to the cost of capital than smaller tech firms. Over the next five years, if the global economy enters a period of rate stabilization or cuts, Nvidia’s valuation could see further multiple expansion as investors seek out high-growth, high-quality cash flows.

Geopolitical Tensions and Supply Chain Integrity

Perhaps the greatest threat to Nvidia’s stock price is its reliance on Taiwan Semiconductor Manufacturing Company (TSMC) for production. Geopolitical tensions regarding Taiwan present a “tail risk”—a low-probability but high-impact event.

Furthermore, U.S. export restrictions on high-end chips to China have already impacted Nvidia’s revenue. Over the next five years, investors must watch how Nvidia navigates these regulatory hurdles. The company’s ability to design “export-compliant” chips that still offer competitive performance will be vital for maintaining its market share in the second-largest economy in the world.

Projecting the 2029 Price Target: Bull, Bear, and Base Cases

When looking five years into the future, it is helpful to visualize different scenarios based on market adoption and financial performance.

The Bull Case: The Sovereign AI Revolution

In the most optimistic scenario, AI becomes the “new electricity.” We see the rise of “Sovereign AI,” where nations build their own domestic AI clouds to protect their data and culture. In this world, Nvidia’s addressable market expands from a few dozen tech giants to dozens of nation-states.

If Nvidia can maintain its 80%+ market share in AI accelerators and grow its software revenue into a multi-billion dollar recurring stream, a market capitalization of $5 trillion or even $7 trillion is not out of the realm of possibility. This would imply a stock price significantly higher than today’s levels, potentially doubling or tripling as AI moves from experimental to ubiquitous.

The Bear Case: Saturation and Cyclical Downturns

The bear case hinges on the idea that the AI hype cycle has outpaced actual utility. If businesses find that the Return on Investment (ROI) for AI projects is lower than expected, they may slash their infrastructure budgets.

Semiconductors have historically been a cyclical industry. If we enter a period of oversupply, Nvidia’s margins could shrink, and its P/E multiple could contract from its current premium levels to a more modest “mature tech” multiple (similar to Cisco after the dot-com bubble). In this scenario, the stock could remain flat or experience a 30–40% correction over the five-year period as it waits for the next growth catalyst.

Conclusion: Building a Long-Term Investment Thesis

Predicting the exact price of Nvidia in five years is an exercise in probability, not certainty. However, the financial data suggests that Nvidia is uniquely positioned at the intersection of the most important technological shift of the century.

For the long-term investor, Nvidia represents more than just a chip company; it is a play on the increasing computational intensity of the global economy. While volatility is guaranteed, the combination of high-margin software ecosystems, a relentless pace of innovation, and a dominant position in the data center market makes Nvidia a formidable contender for continued growth.

Where will Nvidia stock be in five years? If the company continues to execute its roadmap and the world remains hungry for intelligence-as-a-service, Nvidia is likely to remain one of the most valuable and influential entities in the financial world. The key for investors will be to look past the quarterly “noise” and focus on the structural shift toward an AI-first economy—a shift that Nvidia is currently leading with no clear end in sight.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.