The pursuit of higher education is a transformative investment, but for many, it comes with a significant financial hurdle. Student loans are often the crucial bridge that connects aspiring students to their academic dreams. Yet, navigating the intricate world of student financing – replete with federal programs, private lenders, varying interest rates, and diverse repayment plans – can feel overwhelming.

This guide aims to demystify the process, providing a professional and insightful overview of where to secure student loans. We will delineate the primary sources of funding, highlight their unique characteristics, and equip you with the knowledge to make informed decisions that support your educational journey without undue financial stress.

Decoding Student Loan Types: Federal, Private, and Niche Options

The landscape of student financing is broadly categorized into federal and private loans, each with distinct advantages and considerations. Understanding these fundamental differences is the first step toward building a sound financial plan for your education.

Federal Student Loans: The Cornerstone of Aid

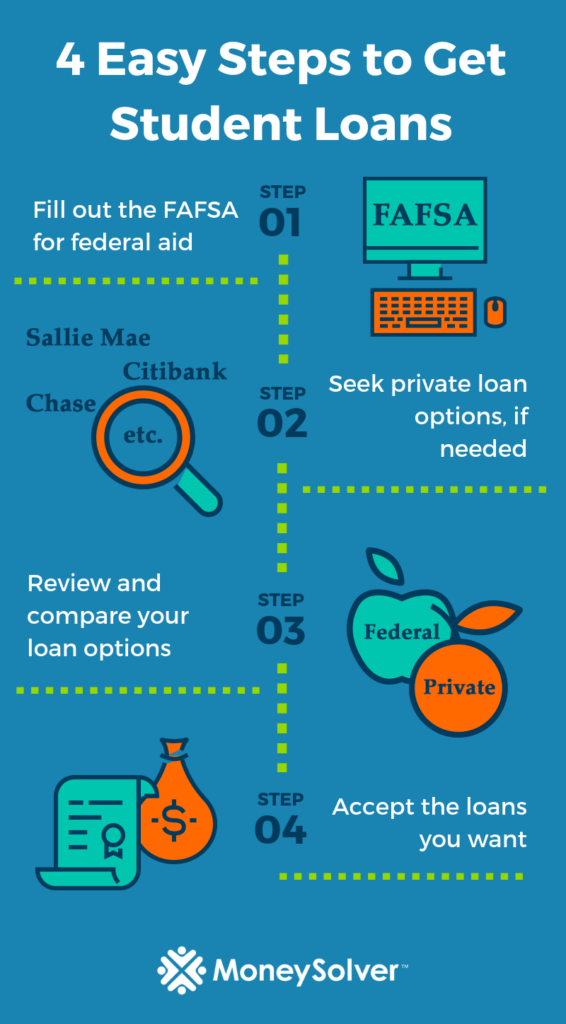

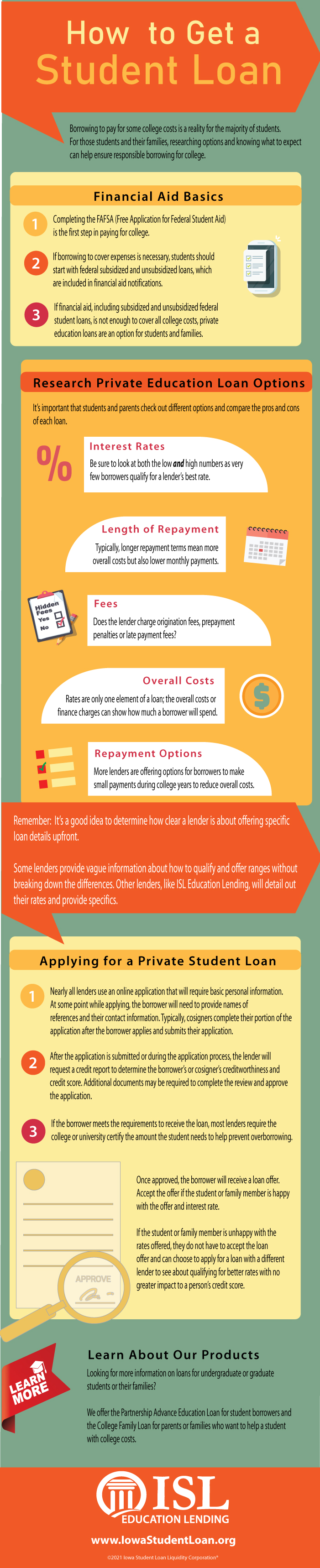

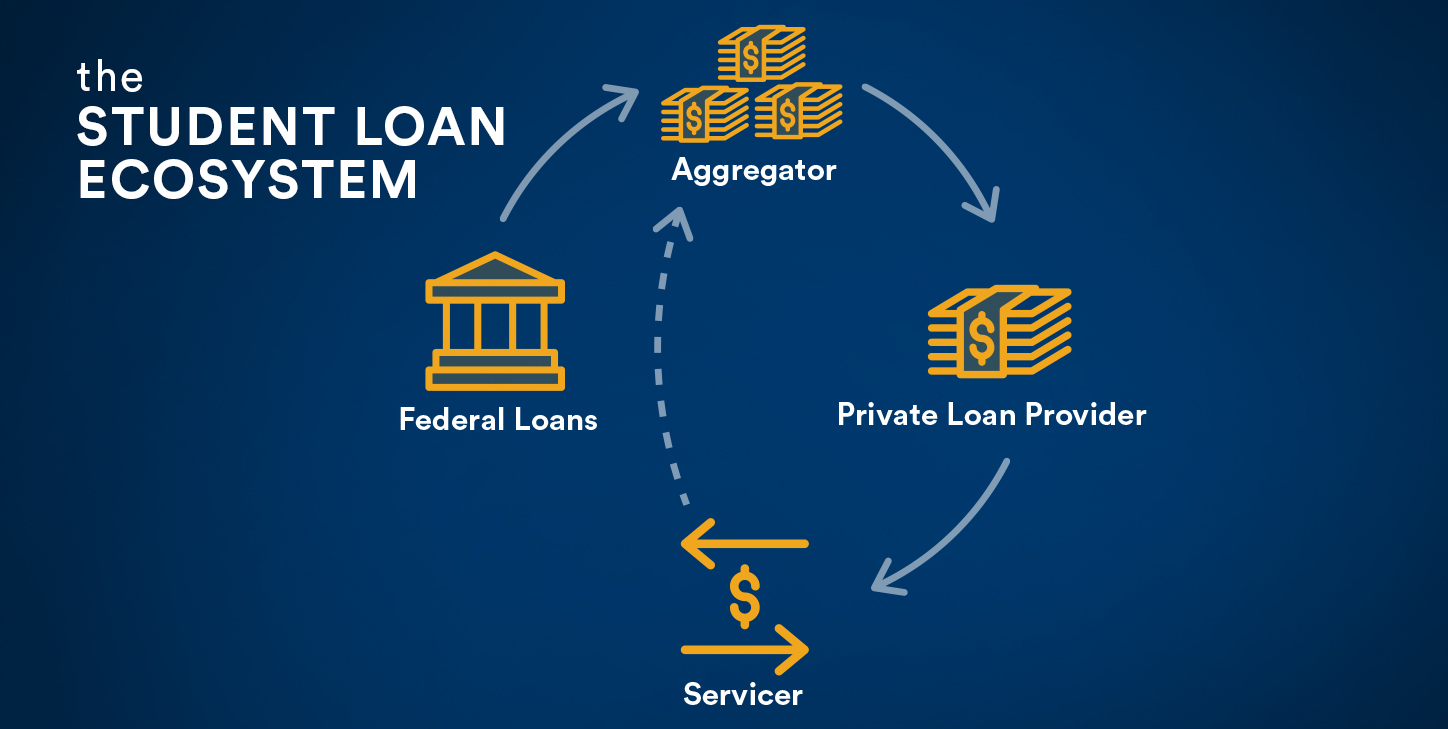

Federal student loans, provided by the U.S. Department of Education, are generally the most advantageous option and should be your primary focus. They offer a suite of borrower protections and benefits typically unavailable with private loans, including fixed interest rates, flexible repayment plans (like Income-Driven Repayment), and potential for deferment, forbearance, or even loan forgiveness under specific programs. Eligibility for most federal loans hinges on completing the Free Application for Federal Student Aid (FAFSA), which assesses your financial need.

Key types of federal loans include:

- Direct Subsidized Loans: For undergraduate students with demonstrated financial need. The government covers interest while you’re in school at least half-time, during your grace period, and during deferment.

- Direct Unsubsidized Loans: Available to undergraduate and graduate students, irrespective of financial need. Interest accrues from the moment the loan is disbursed.

- Direct PLUS Loans: For graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). These require a credit check but offer favorable federal benefits.

Private Student Loans: Bridging the Funding Gap

Private student loans are non-federal loans offered by banks, credit unions, and other private financial institutions. They are designed to supplement federal aid when the cost of attendance exceeds the maximum federal loan limits or other financial assistance received. Unlike federal loans, private loans are primarily credit-based. Your (and often a co-signer’s) credit score and financial history are paramount in determining eligibility, interest rates, and terms.

While they lack the extensive borrower protections of federal loans, private loans can be a necessary component of a comprehensive funding strategy, particularly for students with excellent credit or those pursuing more expensive academic programs. They offer a diverse range of options, making careful comparison essential.

State & Institutional Programs: Localized Support

Beyond national federal and private options, many states offer their own student loan programs, often with specific residency requirements and potentially favorable terms for residents. Similarly, individual colleges and universities may provide institutional loans, sometimes tied to specific academic departments or for students with particular circumstances. These programs, though less universally publicized, can be valuable for filling smaller funding gaps and are worth investigating directly through your state’s higher education agency or your chosen institution’s financial aid office.

Maximizing Federal Aid: Your Primary Resource

For the vast majority of students, the journey to financial aid begins and heavily relies on federal programs. The streamlined process, coupled with unparalleled borrower benefits, makes federal aid your most crucial resource.

The FAFSA: Gateway to Federal Funds

The Free Application for Federal Student Aid (FAFSA) is the single most important document in accessing federal student aid. It serves as the application for federal grants, scholarships, work-study programs, and, critically, federal student loans. To be eligible, you generally must be a U.S. citizen or eligible non-citizen, have a valid Social Security number, be enrolled in an eligible degree or certificate program, and maintain satisfactory academic progress.

Completing the FAFSA requires detailed financial information, including income from tax returns, bank statements, and investment records for yourself and, if dependent, your parents. It is imperative to complete the FAFSA as early as possible each year, as some aid is awarded on a first-come, first-served basis, and deadlines can vary by state and institution. The information you provide calculates your Expected Family Contribution (EFC), which schools use to determine your financial need and the amount of aid you qualify for.

Understanding Federal Loan Types and Benefits

The appeal of federal loans lies not just in their accessibility but in their borrower-centric design:

- Fixed Interest Rates: Federal loan rates are fixed for the life of the loan, providing predictable monthly payments regardless of market fluctuations.

- Income-Driven Repayment (IDR) Plans: These invaluable plans adjust your monthly payment based on your income and family size, offering a safety net if your post-graduation earnings are lower than expected.

- Deferment and Forbearance: In times of financial hardship (e.g., unemployment, economic hardship), you can temporarily postpone loan payments without penalty, protecting your credit score.

- Loan Forgiveness Programs: Programs like Public Service Loan Forgiveness (PSLF) can forgive remaining balances for those in qualifying public service jobs after a certain number of payments.

- No Credit Check (for most): Direct Subsidized and Unsubsidized Loans do not require a credit check, making them widely accessible to students without established credit histories.

These benefits underscore why exhausting federal loan options should always precede considering private alternatives.

Navigating Private Student Loans: A Strategic Approach

While federal loans should be your priority, they have borrowing limits that may not cover the full cost of your education. In such cases, private student loans become a necessary component of your funding strategy.

When and Where to Seek Private Funding

Private loans are best considered only after you have maximized all federal aid, scholarships, and grants. They are typically used to bridge the remaining financial gap for tuition, fees, housing, books, and other living expenses. Students with excellent credit or a creditworthy co-signer often find the most favorable terms from private lenders.

The private loan market is diverse, encompassing various lenders:

- Traditional Banks: Major financial institutions like Sallie Mae, Wells Fargo, and Citizens Bank offer private student loan products. They often have robust online platforms and customer service.

- Credit Unions: Local or national credit unions can be competitive, sometimes offering members slightly better rates or more personalized service.

- Online Lenders: Digital-first lenders such as College Ave, Ascent, and Earnest specialize in student loans, often featuring streamlined application processes and potentially unique repayment options.

- State-Affiliated Lenders: As mentioned, some states have their own lending agencies that may offer more favorable terms to state residents compared to national private lenders.

When researching, compare multiple lenders’ offerings, focusing on interest rates, fees, repayment terms, and customer reviews.

Critical Factors: Rates, Co-signers, and Terms

Private student loans are less standardized than federal loans, making careful scrutiny essential.

- Interest Rates: Private loans can have fixed or variable interest rates. Variable rates might start lower but can fluctuate with market conditions, potentially increasing your payments. Fixed rates offer payment predictability but may start higher. Always compare the Annual Percentage Rate (APR), which includes fees, for the true cost.

- Co-signers: Most students require a creditworthy co-signer (typically a parent or guardian) to qualify for a private loan, especially to secure lower interest rates. A co-signer’s good credit significantly improves approval chances. Understand that a co-signer is equally responsible for the debt.

- Repayment Terms: Private lenders offer varying repayment structures. Some allow you to defer payments until after graduation, while others may require interest-only payments or even full payments while you’re still in school. Evaluate how these options impact your total loan cost and future budget. Look for lenders that offer some flexibility in case of financial hardship, though these are generally less comprehensive than federal protections.

Smart Funding Strategies: Beyond Borrowing

While loans are a critical resource, they represent debt that must be repaid. A strategic financial approach prioritizes minimizing your borrowing by first exhausting all “free money” options and adopting responsible borrowing habits.

Scholarships & Grants: Free Money First

Scholarships and grants are “gift aid” – money that does not need to be repaid. They are typically awarded based on merit (academic achievement, talents, community service) or financial need.

- Institutional Scholarships: Your chosen college or university is often a significant source. Check their financial aid website and specific departmental offerings.

- Private Scholarships: Numerous organizations, foundations, and corporations offer scholarships based on diverse criteria. Utilize online search engines like Fastweb, Scholarship.com, and the College Board’s scholarship search.

- Federal and State Grants: Programs like the Pell Grant (federal) and various state-specific grants are need-based and can substantially reduce your reliance on loans. Your FAFSA application automatically considers you for these.

Dedicate considerable time to researching and applying for scholarships and grants. Every dollar you secure in gift aid is a dollar you won’t have to borrow and repay with interest.

Employer Aid & Responsible Borrowing

Some employers offer tuition assistance, reimbursement programs, or scholarships for employees pursuing higher education, particularly if it aligns with their professional development. If you are employed, inquire with your human resources department about such benefits. This can significantly reduce your out-of-pocket expenses.

When loans become necessary, adopt intelligent borrowing practices:

- Borrow Only What You Need: Accurately calculate your expenses and borrow the absolute minimum required. Avoid borrowing extra for non-essential spending.

- Understand Your Loans: Thoroughly read all loan documents. Be fully aware of your interest rate, repayment schedule, and the consequences of missed payments.

- Track Your Debt: Maintain a comprehensive record of all your student loans – lender, loan type, interest rate, and outstanding balance. This will be invaluable during repayment.

- Consider In-School Payments: Even making small interest payments on unsubsidized or private loans while you’re in school can reduce the total interest accrued over the life of the loan.

The Application-to-Repayment Journey

Securing a student loan involves more than just identifying a lender; it requires a systematic approach from application through to repayment.

Preparing for Application and Comparison

Before applying for any loan, gather all necessary documentation, including your Social Security number, driver’s license, federal tax returns (yours and parents’ if dependent), bank statements, and school information. Having these ready will streamline the application process for both federal and private loans.

For private loans, it is highly advisable to apply to 2-3 different lenders to compare offers side-by-side. Look beyond just the advertised interest rate; scrutinize the Annual Percentage Rate (APR), which reflects the true cost including any fees. Compare repayment terms, potential fees (origination, late payment), and any borrower benefits like interest rate reductions for automatic payments or co-signer release options. Don’t hesitate to ask lenders clarifying questions.

From Disbursement to Repayment Planning

Once approved, loan funds are typically disbursed directly to your school to cover tuition and fees, with any remaining balance sent to you for living expenses. Use these funds judiciously and only for educational and essential living costs.

Crucially, begin planning for repayment well before you graduate. Understand your grace period – the time after you leave school before payments begin. For federal loans, explore the various Income-Driven Repayment plans offered by your loan servicer. For private loans, contact your lender to understand your available options. Proactive repayment planning can prevent future stress and help you manage your debt effectively.

Conclusion

Funding your higher education is a significant investment that often requires student loans. By prioritizing federal loans, diligently pursuing scholarships and grants, and strategically approaching private lending, you can secure the necessary funds. Always approach borrowing with an informed perspective, understand the terms of your loans, and plan for repayment from the outset. Your education is a valuable asset; fund it wisely to pave the way for a successful future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.