Navigating the annual tax season can feel like a daunting task for many, but understanding where and how to file your tax return is the first crucial step towards fulfilling your financial obligations and potentially securing valuable refunds or credits. The method you choose can significantly impact your time, financial outlay, and even the accuracy of your submission. This guide delves into the various avenues available, helping you make an informed decision that aligns with your personal finance situation.

Understanding Your Filing Obligations

Before you even consider the “where,” it’s vital to grasp the “why” and “when” of tax filing. Not everyone is required to file a federal income tax return, but many benefit from doing so even if they aren’t strictly obligated.

Who Needs to File?

Generally, whether you need to file depends on your gross income, filing status, age, and whether you are a dependent. For instance, if your gross income exceeds a certain threshold (which changes annually and varies by filing status), you are required to file. However, even if your income falls below this threshold, you might still want to file to claim a refund for withheld taxes, or to claim refundable tax credits like the Earned Income Tax Credit (EITC) or the Child Tax Credit, which could put money back into your pocket. Certain types of income, such as self-employment earnings above a minimal amount, also trigger a filing requirement regardless of your total gross income. It’s always prudent to consult the IRS guidelines or a tax professional if you’re unsure about your specific obligation.

Key Deadlines to Remember

The standard federal tax filing deadline for most individual taxpayers is April 15th of each year. If April 15th falls on a weekend or holiday, the deadline is typically shifted to the next business day. There are specific deadlines for certain groups, such as those living in federally declared disaster areas or U.S. citizens living abroad. If you anticipate needing more time, you can usually file an extension, which typically grants you an additional six months to file, usually until October 15th. It’s crucial to remember that an extension to file is not an extension to pay. If you expect to owe taxes, you should still estimate and pay them by the original April deadline to avoid penalties and interest. Missing deadlines can result in costly penalties, so proactive calendar management is essential for sound financial planning.

The Primary Avenues for Tax Filing

Once you’ve confirmed your filing obligation and marked your calendar, the next step is to choose your filing method. The landscape of tax filing options has evolved considerably, offering a range of choices from fully self-service digital platforms to personalized professional assistance.

IRS Direct File (When Available)

The IRS has been piloting a Direct File program, offering a free online tax filing service directly through the agency itself. This initiative aims to simplify the filing process for taxpayers with simpler tax situations, potentially cutting out third-party costs. While its availability and scope may vary, if your tax situation aligns with the program’s eligibility criteria, using IRS Direct File could be a straightforward and cost-effective option. It leverages a direct interface with the tax authority, streamlining submission and reducing potential errors associated with interpreting third-party software. Keep an eye on IRS announcements for eligibility and availability in your filing year.

Tax Software Solutions

For many, tax preparation software represents a powerful blend of autonomy and guidance. Companies like TurboTax, H&R Block, TaxAct, and FreeTaxUSA offer user-friendly interfaces that guide you step-by-step through the process, asking questions to ensure you capture all relevant income, deductions, and credits. Many of these platforms offer free versions for simple tax returns and paid versions for more complex scenarios, often including state tax filing and audit support. The key benefit here is convenience: you can file from anywhere with an internet connection, at any time. Moreover, these programs perform complex calculations automatically, reducing the risk of mathematical errors, and often provide immediate estimates of your refund or tax due. Choosing the right software often depends on the complexity of your return and your budget.

Professional Tax Preparers

For individuals with complex financial situations—such as business owners, those with significant investment portfolios, foreign income, or intricate deductions—hiring a professional tax preparer can be an invaluable investment. Certified Public Accountants (CPAs), Enrolled Agents (EAs), and other qualified tax professionals can offer expert advice, ensure compliance with the latest tax laws, and identify every legitimate deduction or credit you might be eligible for. They can represent you in case of an audit and provide year-round tax planning advice that contributes to your overall financial well-being. While this option comes with a fee, the peace of mind, potential tax savings, and expert guidance often justify the cost, especially when dealing with high-stakes financial scenarios.

Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE)

For those with modest incomes, disabilities, or who speak limited English, and for taxpayers aged 60 and over, the IRS-sponsored VITA and TCE programs offer free tax preparation and e-filing services. These programs are staffed by IRS-certified volunteers who provide accurate assistance. VITA and TCE sites are typically located in community centers, libraries, schools, shopping malls, and other convenient locations. These services are a fantastic resource for ensuring that eligible individuals can file their taxes correctly and on time without incurring professional fees, helping them keep more of their hard-earned money. Eligibility for these services is income-based, with specific thresholds provided by the IRS annually.

Choosing the Right Filing Method for You

The “best” filing method isn’t universal; it depends entirely on your personal circumstances, financial complexity, comfort level with technology, and budget. Thoughtful consideration of these factors will lead you to the most suitable choice.

DIY with Software: When it Makes Sense

If your tax situation is relatively straightforward—you have W-2 income, a few standard deductions, and perhaps some common credits like the Child Tax Credit—doing it yourself with tax software is often the most cost-effective and efficient method. Modern tax software is designed to be intuitive, guiding you through questions that illuminate potential deductions and credits. This approach empowers you to understand your tax situation better and maintain direct control over your financial data. It’s particularly appealing for those who are comfortable with technology and prefer to handle their financial affairs independently, saving on preparation fees.

Professional Help: When to Splurge

Investing in a professional tax preparer becomes a wise financial decision when your tax situation becomes intricate. This includes scenarios such as owning multiple properties, running a small business, experiencing significant life changes (marriage, divorce, birth of a child, retirement), or having income from diverse sources like foreign investments or cryptocurrency. A professional can identify complex deductions specific to your situation, ensure compliance with intricate tax laws, and provide strategic advice that could lead to substantial long-term savings. For business owners, a tax professional can also assist with quarterly estimated taxes, payroll taxes, and navigating business deductions, ensuring your enterprise remains compliant and fiscally sound.

Free Options: Leveraging Community Resources

For those on a tight budget or with specific eligibility criteria, leveraging free tax filing resources is an excellent financial strategy. The IRS Direct File (when available) offers a direct, free route for simple returns. The VITA and TCE programs provide invaluable, free, expert assistance to qualifying taxpayers, ensuring accuracy and helping them claim all eligible credits. Many commercial tax software providers also offer free editions for very simple returns. Exploring these options can save hundreds of dollars in preparation fees, making a real difference to your personal finances. It’s important to verify eligibility requirements for these free services each year to ensure you qualify.

Gathering Your Essential Documents

Regardless of your chosen filing method, successful tax filing hinges on having all your necessary documentation readily accessible. Preparing these documents in advance will significantly streamline the filing process and minimize stress.

Income Statements (W-2s, 1099s)

These are the backbone of your tax return, detailing your earnings. For most employees, a Form W-2 (Wage and Tax Statement) will report your wages, tips, and other compensation, as well as the federal, state, and local taxes withheld. If you received income from sources other than a traditional employer, you’ll likely receive various 1099 forms:

- Form 1099-MISC: For miscellaneous income, such as rent or certain attorney fees.

- Form 1099-NEC: For nonemployee compensation (freelance or contract work).

- Form 1099-INT: For interest income from banks or other financial institutions.

- Form 1099-DIV: For dividends and distributions from stocks and mutual funds.

- Form 1099-R: For distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, etc.

- Form 1099-B: For proceeds from broker and barter exchange transactions.

Ensure you have all relevant W-2s and 1099s for the tax year; these forms typically arrive by late January or early February.

Deduction & Credit Documentation

To maximize your refund or minimize your tax liability, you’ll need documentation for any deductions or credits you plan to claim. This could include:

- Itemized Deductions: Receipts for medical expenses, charitable contributions, mortgage interest statements (Form 1098), state and local tax payments.

- Education Credits: Form 1098-T (Tuition Statement), receipts for educational expenses.

- Childcare Credits: Records of payments made to childcare providers, including their Taxpayer Identification Number (TIN).

- Retirement Contributions: Records of IRA contributions, HSA contributions.

- Business Expenses: For self-employed individuals, meticulous records of all business-related income and expenses are crucial.

Organizing these documents throughout the year can save immense time during tax season.

Prior Year’s Tax Return

Your previous year’s tax return is a valuable reference. It provides essential information like your adjusted gross income (AGI), which is often needed for verification when e-filing. It also helps you recall deductions or credits you claimed previously that might still be applicable, and serves as a roadmap for changes in your financial situation. Keep at least the last three years of tax returns and supporting documents on hand, as the IRS generally has three years to audit your return.

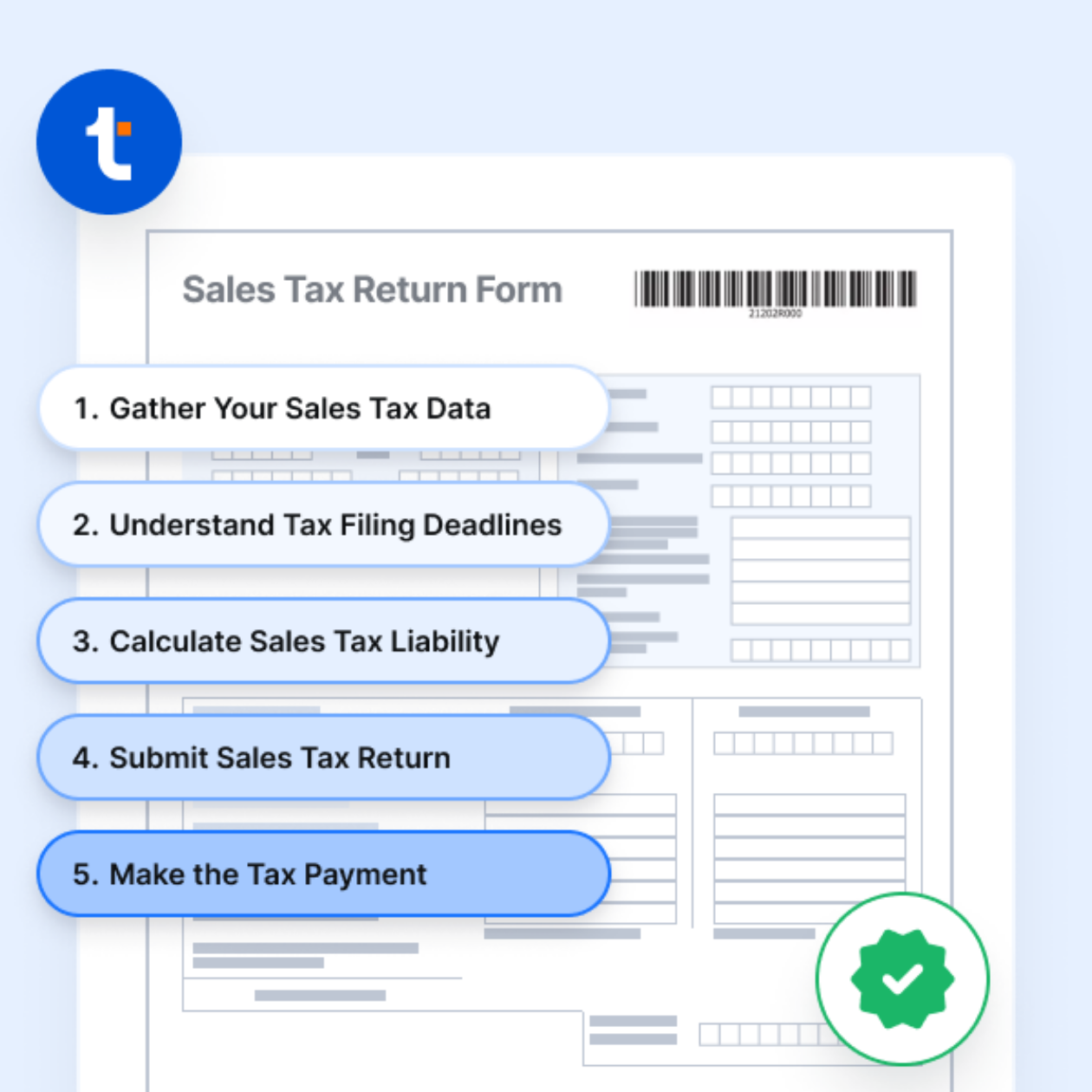

Final Steps: Reviewing and Submitting Your Return

The final stage of tax filing involves a meticulous review and proper submission, critical steps to ensure accuracy and compliance. Rushing this phase can lead to costly errors or delays.

Double-Checking for Accuracy

Before submitting your tax return, conduct a thorough review. Look for common errors such as misspelled names, incorrect Social Security Numbers (SSNs), wrong addresses, and mathematical mistakes. Verify that all income sources have been reported and all applicable deductions and credits have been claimed. If you’re using software, leverage its error-checking features. If you’re working with a professional, don’t hesitate to ask questions about anything you don’t understand. An accurate return prevents potential delays in processing your refund, avoids notices from the IRS, and reduces the risk of audits, safeguarding your financial peace of mind.

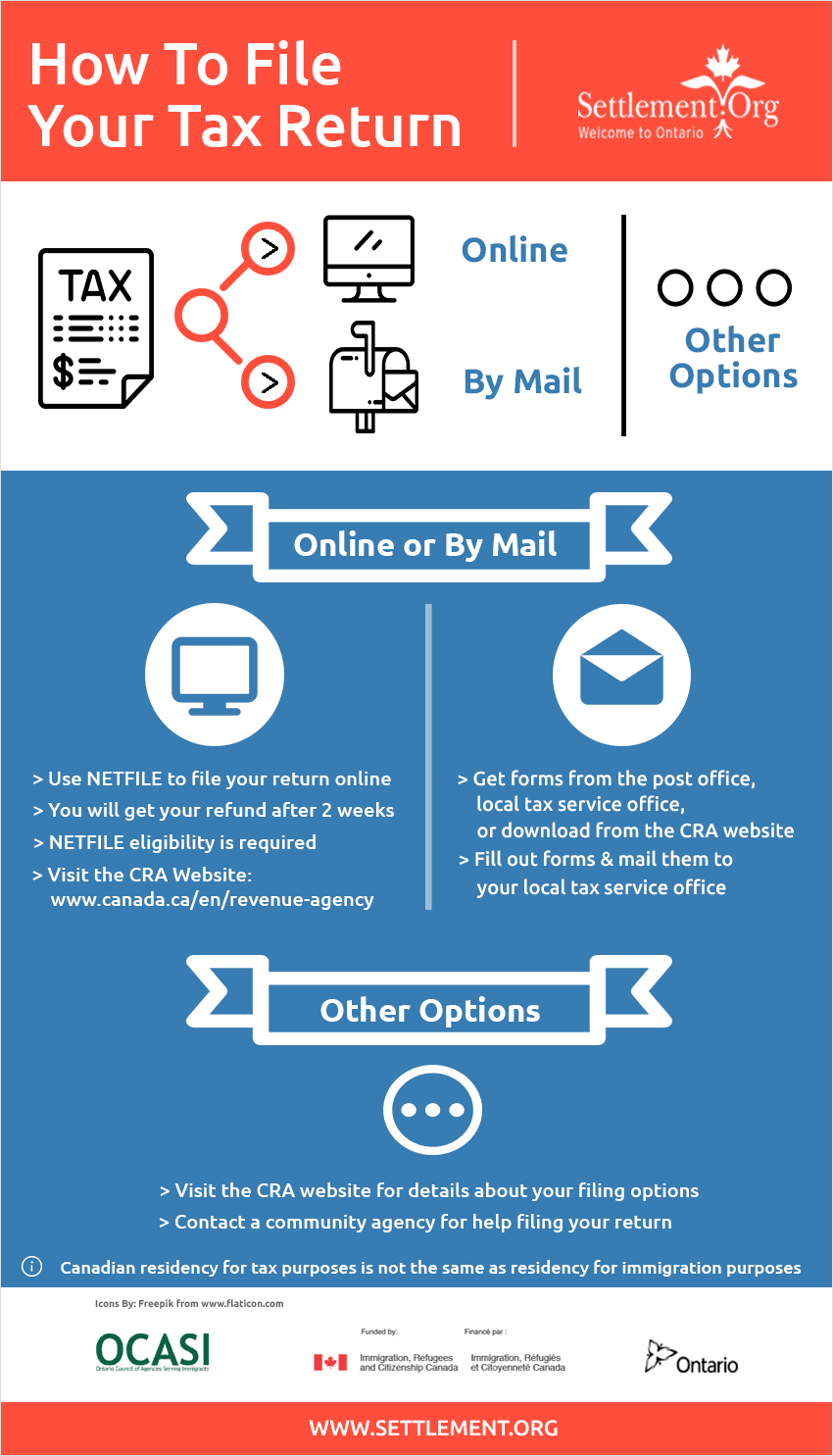

Electronic vs. Paper Filing

The vast majority of taxpayers now file their returns electronically (e-file), and for good reason. E-filing is faster, more accurate, and more secure than mailing a paper return. You typically receive confirmation that the IRS has received your return within 24-48 hours, and refunds for e-filed returns are processed much more quickly, especially when combined with direct deposit. While paper filing is still an option, it’s generally reserved for specific, uncommon situations or those who prefer not to use digital methods. If you choose to paper file, ensure you send it to the correct IRS address (which varies by state and form type) and obtain proof of mailing.

What Happens After You File?

Once your return is submitted and accepted, the waiting begins. If you’re expecting a refund, you can track its status using the IRS “Where’s My Refund?” tool, usually available 24 hours after e-filing or four weeks after mailing a paper return. If you owe taxes, ensure your payment is made by the deadline, either electronically (e.g., via IRS Direct Pay, Electronic Federal Tax Payment System – EFTPS) or by mail with Form 1040-V (Payment Voucher). Remember to keep a copy of your filed return and all supporting documentation for at least three years, as these records are crucial for future reference, amendments, or potential audits. Filing your tax return correctly and on time is a cornerstone of responsible personal finance, ensuring you meet your obligations and optimize your financial position.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.