In an era of market volatility and fluctuating economic indicators, the Certificate of Deposit (CD) remains a cornerstone of a conservative investment strategy. As a low-risk, fixed-income instrument, the CD offers a guaranteed return on investment, making it an attractive option for those looking to preserve capital while earning interest. However, the modern financial landscape has evolved far beyond the local bank branch. Today, investors must navigate a sea of online banks, credit unions, and brokerage firms to find the best yields and terms.

Knowing where to buy a Certificate of Deposit is not merely about finding the highest interest rate; it is about understanding the institutional stability, liquidity options, and strategic advantages offered by different providers. This guide explores the primary venues for purchasing CDs and how to align your choice with your personal financial goals.

1. Traditional vs. Online Institutions: Finding the Best Yields

The first decision any investor faces when looking for a CD is whether to stay with a traditional brick-and-mortar bank or venture into the world of online-only financial institutions. The “where” significantly impacts the “how much” regarding your return.

Traditional Brick-and-Mortar Banks

Traditional banks, such as Chase, Bank of America, or Wells Fargo, offer the advantage of physical accessibility and integrated services. If you already have a checking and savings account with a large national bank, opening a CD there is often a seamless process. However, convenience frequently comes at a cost. Because these institutions maintain high overhead costs—including physical branches and large staff—their interest rates on CDs are often significantly lower than the national average. They are best suited for investors who prioritize personal relationships and the security of a “Too Big to Fail” institution over maximizing every basis point of yield.

Online-Only Banks and Neo-Banks

Online banks like Ally, Marcus by Goldman Sachs, and Capital One have revolutionized the CD market. Without the burden of physical infrastructure, these institutions can pass their savings on to the consumer in the form of much higher Annual Percentage Yields (APYs). Online banks are often the first place savvy investors look for high-yield CDs. They typically offer user-friendly digital interfaces, robust mobile apps, and 24/7 customer service. For those comfortable managing their finances digitally, online banks currently provide some of the most competitive CD rates in the industry.

Credit Unions: The Member-Owned Alternative

Credit unions are non-profit organizations owned by their members. Because they do not have to answer to shareholders, they frequently offer CD rates (often called “Share Certificates”) that rival or even exceed those of online banks. To buy a CD at a credit union, you must meet membership requirements, which can range from living in a specific geographic area to working for a certain employer or belonging to an association. Credit unions are excellent choices for investors looking for competitive rates coupled with a community-focused banking experience.

2. Specialized Platforms and Brokered CDs

Beyond standard bank-issued products, investors can look toward the investment markets to find Certificates of Deposit. These options provide different levels of flexibility and often cater to those with larger sums of capital or complex portfolio needs.

Financial Marketplaces and Aggregators

Before committing to a specific bank, many investors use financial marketplaces like Raisin or SaveBetter. These platforms act as intermediaries, allowing you to open and manage multiple CDs from various banks through a single portal. This is a highly efficient way to “shop” for the best rates nationwide without the hassle of opening ten different bank accounts. It allows for diversification of your cash across multiple institutions while keeping your administrative overhead low.

Brokered CDs through Investment Firms

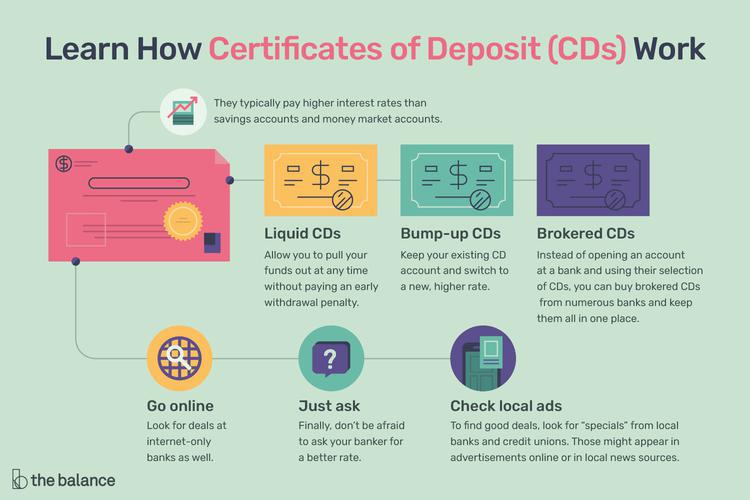

Brokerage firms like Charles Schwab, Fidelity, and Vanguard offer what are known as “Brokered CDs.” Unlike a traditional CD that you buy directly from a bank, a brokered CD is purchased through a brokerage account. There are several distinct advantages here. First, the brokerage firm negotiates with various banks to offer a wide selection of rates and terms in one place. Second, brokered CDs can sometimes be sold on the secondary market before they mature. If interest rates have fallen since you bought the CD, your CD might even sell for a premium. This provides a level of liquidity that traditional bank CDs—which usually carry stiff early withdrawal penalties—cannot match.

Jumbo CDs for High-Net-Worth Investors

For those looking to deposit $100,000 or more, “Jumbo CDs” are the standard. While many banks offer the same rates for a $10,000 deposit as they do for $100,000, some institutions offer tiered pricing. Buying a Jumbo CD can sometimes unlock “relationship rates” or specialized terms. When looking for Jumbo CDs, it is often beneficial to speak directly with a private banker or a wealth management representative, as these rates are sometimes not advertised on public-facing websites.

3. Critical Factors to Evaluate Before Purchasing

Once you have identified a potential institution, the “where” must be balanced with the “what.” Every CD comes with a set of terms and conditions that can significantly impact your net return.

Interest Rates (APY) and Compounding Frequency

The headline rate is the Annual Percentage Yield (APY). However, it is essential to look at how often interest is compounded—daily, monthly, or quarterly. Daily compounding will result in a slightly higher effective return than annual compounding. When comparing where to buy, ensure you are looking at the APY rather than just the nominal interest rate, as the APY accounts for the effects of compounding within the year.

Minimum Deposit Requirements and Term Lengths

Different institutions have different “buy-in” levels. Some online banks allow you to open a CD with $0 or $500, while traditional banks might require $1,000 to $2,500. Furthermore, the term length—ranging from one month to ten years—must align with your liquidity needs. Generally, the longer you agree to leave your money in the bank, the higher the interest rate you will receive. However, in a “flat” or “inverted” yield curve environment, short-term CDs may occasionally offer higher rates than long-term ones.

Early Withdrawal Penalties (EWP)

This is perhaps the most overlooked aspect of buying a CD. If you need your money before the term expires, the bank will charge a penalty. At some institutions, this penalty might be three months of interest; at others, it could be a year’s worth of interest or even a portion of your principal. Before buying, always read the fine print regarding the EWP. If you think there is a chance you might need the funds, you should look for “No-Penalty CDs,” which allow for early withdrawal after a short initial holding period (usually 7 days) without any loss of interest.

4. Strategic Approaches to Buying CDs

Successful CD investing is rarely about buying a single certificate. Instead, it involves a strategic approach to timing and liquidity. Where you buy your CDs can depend on which strategy you intend to employ.

The CD Ladder Strategy

A CD ladder involves dividing your total investment into equal parts and investing them in CDs with different maturity dates (e.g., a 1-year, 2-year, 3-year, 4-year, and 5-year CD). As each CD matures, you reinvest it into a new 5-year CD. This strategy provides regular liquidity while allowing you to capture the higher rates associated with long-term certificates. When building a ladder, it is often easiest to use a single brokerage firm or an online bank that offers a wide variety of term lengths to keep your management centralized.

Step-Up and Bump-Up CDs

If you are worried that interest rates will rise after you have locked in your CD, you might look for “Step-Up” or “Bump-Up” CDs. A Bump-Up CD gives you the option to request a rate increase if the bank’s offered rates on new CDs rise during your term. A Step-Up CD has a pre-determined schedule where the rate increases automatically at set intervals. These products are usually found at larger regional banks and online banks that want to offer more flexible products to entice cautious investors.

5. Ensuring Your Investment is Protected

Security is the primary reason investors choose CDs. However, the protection of your principal depends entirely on where you choose to buy and how you structure your accounts.

FDIC vs. NCUA Insurance

When buying a CD from a bank, ensure the institution is a member of the Federal Deposit Insurance Corporation (FDIC). If you are buying from a credit union, ensure it is insured by the National Credit Union Administration (NCUA). Both provide up to $250,000 of protection per depositor, per insured bank, for each account ownership category. This insurance is the “gold standard” of safety in the financial world, ensuring that even if the bank fails, your principal and accrued interest (up to the limit) are safe.

Managing Limits Across Multiple Institutions

For investors with more than $250,000, the “where” becomes a matter of diversification for the sake of insurance. To ensure all your funds are protected, you should spread your CD purchases across multiple different banks. This is where brokered CDs or marketplace platforms (like Raisin) become invaluable. They allow you to hold millions of dollars in total CD investments while ensuring that no more than $250,000 is held at any single underlying bank, thus maintaining full FDIC coverage across your entire portfolio.

The Importance of “Automatic Renewal” Clauses

Finally, be wary of the “grace period.” Most institutions will automatically renew your CD into a new term of the same length once it matures, often at a much lower “standard” rate rather than a promotional rate. When choosing where to buy, look for banks that provide clear notifications via email or app alerts as your maturity date approaches. This allows you to move your money to a higher-yielding option or a different asset class without being locked into another cycle at an unfavorable rate.

In conclusion, the best place to buy a Certificate of Deposit depends on your specific balance of yield, convenience, and liquidity. While online banks offer the highest rates for most consumers, brokered CDs provide superior flexibility for active investors, and credit unions offer a member-centric alternative. By evaluating APYs alongside withdrawal penalties and insurance limits, you can effectively use CDs to build a secure and profitable foundation for your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.