Buying a car is a significant financial decision for most individuals, and for many, it necessitates securing a car loan. While the monthly payment often dominates the conversation, understanding your car loan interest rate is arguably the single most critical factor in determining the true cost of your vehicle. The interest rate dictates how much extra you’ll pay on top of the principal amount you borrowed, directly impacting your budget and long-term financial health. Ignoring or misunderstanding this crucial figure can lead to thousands of dollars in avoidable expenses over the life of the loan. This guide will walk you through the intricacies of car loan interest rates, explaining what they are, why they matter, how they’re determined, and practical steps you can take to figure out—and ideally improve—your own rate.

Understanding the Fundamentals of Car Loan Interest

Before you can figure out your interest rate, it’s essential to grasp what it represents and why its impact is so profound on your personal finances.

What is a Car Loan Interest Rate?

In simple terms, an interest rate is the cost of borrowing money, expressed as a percentage of the principal loan amount. When you take out a car loan, the lender (a bank, credit union, or dealership) is providing you with funds to purchase a vehicle. In return for this service, they charge you interest. This percentage is typically applied annually, meaning you pay a certain percentage of the outstanding loan balance each year.

It’s crucial to distinguish between the nominal interest rate and the Annual Percentage Rate (APR). The nominal interest rate is the basic rate at which interest is calculated. The APR, however, provides a more comprehensive picture of the total cost of borrowing. It includes not only the interest rate but also any additional fees associated with the loan, such as origination fees, administrative charges, or other upfront costs. For a true apples-to-apples comparison between different loan offers, the APR is the figure you should always pay closest attention to, as it reflects the true annual cost of your financing.

Why Does Your Interest Rate Matter So Much?

The interest rate is not merely an abstract number; it has a tangible and significant impact on your monthly car payment and the total amount you will pay over the entire loan term. Even a seemingly small difference in percentage points can translate into hundreds or even thousands of dollars over a typical 5-7 year car loan.

Consider two hypothetical loans for a $30,000 car over 60 months (5 years):

- Loan A: Interest rate of 5% APR

- Loan B: Interest rate of 8% APR

For Loan A, your estimated monthly payment would be around $566, and the total interest paid over 5 years would be approximately $3,966.

For Loan B, your estimated monthly payment would jump to about $608, and the total interest paid would be roughly $6,480.

That’s a difference of $42 per month and a staggering $2,514 in total interest for just a 3-percentage-point increase. This money could otherwise be used for savings, investments, or other essential expenses. A higher interest rate means more of your monthly payment goes towards servicing the interest rather than reducing the principal balance of the loan, slowing down your equity build-up in the vehicle. Understanding this impact empowers you to seek out the best possible rate.

Key Factors Influencing Your Car Loan Interest Rate

Lenders don’t just assign interest rates randomly; they assess a variety of factors to determine the level of risk associated with lending to you. The higher the perceived risk, the higher the interest rate they will charge to compensate themselves.

Your Credit Score and History

This is perhaps the single most influential factor. Your credit score (e.g., FICO score) is a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use it as a quick indicator of how likely you are to make your loan payments on time.

- Excellent Credit (780+): Typically qualifies for the lowest available interest rates, as you are seen as a very reliable borrower.

- Good Credit (670-779): Generally receives competitive rates, though perhaps not the absolute lowest.

- Fair Credit (580-669): May face slightly higher rates due to some past credit challenges or limited credit history.

- Poor Credit (Below 580): Often leads to significantly higher interest rates, as lenders view you as a high-risk borrower. Some may even require a co-signer or substantial down payment.

Your credit history, including payment consistency, amount of debt, and length of credit history, all feed into this score.

Loan Term and Amount

The loan term refers to the length of time you have to repay the loan (e.g., 36, 48, 60, 72, or even 84 months). Generally, shorter loan terms often come with slightly lower interest rates because the lender’s risk is spread over a shorter period. However, shorter terms mean higher monthly payments. Conversely, longer terms typically have higher interest rates but lower monthly payments, making the car seem more “affordable” on a monthly basis, though you’ll pay significantly more interest over the loan’s life.

The loan amount itself can also play a role, though less directly than credit score. Very small loan amounts might sometimes have slightly higher administrative costs reflected in the rate, while very large loans might be scrutinized more closely.

Down Payment

A down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow. A larger down payment has several benefits:

- Reduces Loan-to-Value (LTV) Ratio: A lower LTV means less risk for the lender, as you have more equity in the vehicle from the start. This can lead to a lower interest rate.

- Lower Principal: Less money borrowed means less interest accrues overall.

- Shows Financial Stability: A significant down payment signals to lenders that you are financially responsible and serious about your purchase.

Vehicle Type and Age

The type of vehicle you’re buying can subtly influence your rate. Lenders often consider the car’s resale value and depreciation.

- New Cars: Generally attract lower interest rates because they are less risky for lenders (they hold their value better initially, are less prone to immediate mechanical issues).

- Used Cars: Typically carry slightly higher interest rates due to higher depreciation risk, potential for mechanical problems, and the vehicle’s age. The older the car, the higher the perceived risk might be.

Market Conditions and Lender Policies

Broader economic factors play a part. When the Federal Reserve raises or lowers its benchmark interest rates, this often ripples through the entire lending industry, affecting car loan rates. Additionally, different lenders (banks, credit unions, dealership finance departments, online lenders) have varying risk appetites, overheads, and competitive strategies, leading to different rate offerings. Credit unions, for example, are often known for offering more competitive rates to their members.

Practical Steps to Figure Out Your Car Loan Interest Rate

Whether you’re pre-approved, already have a loan, or are still shopping, there are clear ways to identify your specific interest rate.

Reviewing Your Loan Documents

The most definitive place to find your interest rate is in your official loan documents. These are the papers you signed when you secured the loan. Look for:

- Loan Agreement or Promissory Note: This is the legally binding contract outlining all terms and conditions of your loan. The interest rate, often expressed as an Annual Percentage Rate (APR), will be clearly stated here.

- Truth in Lending Disclosure (TIL Disclosure): This document, mandated by federal law, provides key information about the cost of your credit, including the APR, finance charge, amount financed, and total payments. This is where you’ll find the most comprehensive cost breakdown.

Ensure you differentiate between the simple interest rate and the APR. The APR will give you the total cost inclusive of certain fees. If you’ve just received offers, carefully compare the APRs.

Contacting Your Lender

If you’re unable to locate your physical loan documents or need clarification, directly contacting your lender is your next best step.

- Customer Service: Call your bank, credit union, or the finance company that holds your loan. They can readily provide you with your current interest rate and other loan details.

- Online Portals/Apps: Many lenders offer online accounts or mobile apps where you can log in and view your loan details, including the interest rate, outstanding balance, and payment history.

Utilizing Online Calculators and Tools

While not for finding your specific, existing rate, online car loan calculators are invaluable for understanding the impact of different interest rates and working backward if you know your payment.

- Payment Calculators: Input a potential loan amount, loan term, and a hypothetical interest rate, and the calculator will estimate your monthly payment. This helps you understand what a given rate translates to financially.

- Reverse Calculators: If you know your loan amount, term, and monthly payment, some advanced calculators can work backward to approximate the interest rate you’re paying. This can be useful for verification or quick estimates.

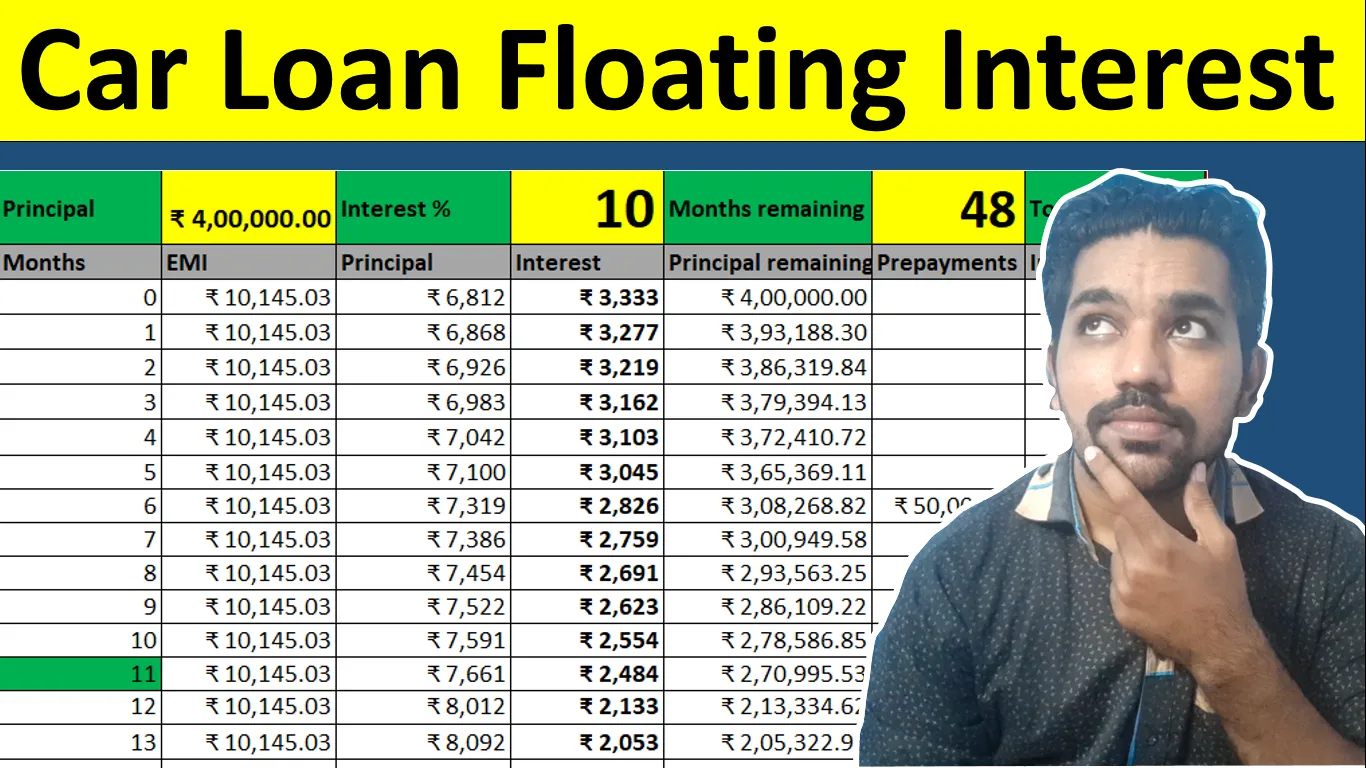

- Amortization Calculators: These tools show you how your payments are broken down between principal and interest over the life of the loan, highlighting the long-term cost implications of your interest rate.

Strategies to Secure a Favorable Car Loan Interest Rate

Knowing your current or potential interest rate is one thing; actively working to improve it is another. Proactive steps can save you a substantial amount of money.

Improving Your Credit Score

Since your credit score is paramount, taking steps to boost it before applying for a loan is highly recommended:

- Pay Bills on Time: Payment history is the biggest factor. Set up reminders or automatic payments.

- Reduce Existing Debt: Lowering your credit utilization ratio (how much credit you use vs. how much you have available) can improve your score.

- Avoid New Credit Applications: Don’t open new credit cards or loans just before applying for a car loan, as this can temporarily ding your score.

- Check Your Credit Report for Errors: Dispute any inaccuracies that could be negatively affecting your score.

Shopping Around for Lenders

Never take the first loan offer you receive, especially from a dealership. Competition among lenders is fierce, and rates can vary significantly.

- Get Pre-Approved: Apply for pre-approval from several different financial institutions (banks, credit unions, online lenders) before you visit the dealership. This provides you with concrete offers, gives you negotiating power, and separates the financing decision from the car-buying process.

- Credit Unions Often Offer Better Rates: As non-profit organizations, credit unions are often able to provide more favorable interest rates to their members compared to traditional banks.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and others specialize in online car loans and can offer very competitive rates, often with streamlined application processes.

Negotiating with Dealerships

While dealerships are convenient, their primary goal is profit. They might mark up interest rates offered by their partner lenders.

- Use Your Pre-Approvals as Leverage: If you have a pre-approval from an outside lender, show it to the dealership. They may try to beat or match it to keep your business.

- Focus on the Car Price and APR Separately: Don’t let them bundle everything into one “monthly payment” discussion. Negotiate the car’s price first, then discuss financing.

Making a Substantial Down Payment

As discussed, a larger down payment reduces the principal borrowed and lowers the lender’s risk, making you a more attractive borrower and potentially qualifying you for a lower interest rate. Aim for at least 10-20% if possible.

Considering a Shorter Loan Term (If Affordable)

While it results in higher monthly payments, opting for a shorter loan term (e.g., 48 or 60 months instead of 72 or 84) often comes with a lower interest rate and significantly reduces the total interest you pay over time. Only choose this option if the higher monthly payment comfortably fits within your budget.

The Long-Term Impact and Continuous Monitoring

Understanding your car loan interest rate isn’t a one-time event. It’s an ongoing aspect of managing your personal finances.

Refinancing Your Car Loan

If your financial situation improves after you’ve taken out a loan—for example, your credit score has significantly increased, or market interest rates have dropped—you might be able to refinance your car loan. This involves taking out a new loan with a lower interest rate to pay off your existing one. Refinancing can lead to lower monthly payments, reduced total interest paid, or a shorter loan term, effectively saving you money over the remaining life of the loan. It’s always worth periodically checking if you qualify for a better rate.

Monitoring Your Loan and Payments

Regularly reviewing your loan statements and understanding how your payments are allocated to principal and interest is a smart financial habit. This awareness helps you stay on track, identify any discrepancies, and empowers you to make informed decisions about potential early principal payments or refinancing opportunities.

By taking the time to understand, track, and strategically manage your car loan interest rate, you empower yourself to make smarter financial decisions, save money, and ultimately drive away with greater peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.