Navigating the complexities of the United States tax system is a significant aspect of personal and business financial management. Perhaps the most critical moment in this annual cycle is the point of payment. Whether you are a high-net-worth investor, a small business owner, or a salaried professional, the question of “where do I send my IRS payment” involves more than just an address—it involves choosing the right financial tool, ensuring security, and optimizing your cash flow.

In an increasingly digital financial landscape, the Internal Revenue Service (IRS) has expanded its intake channels. This guide provides a deep dive into the various payment methods available, the logistical requirements for physical mail, and the strategic financial considerations you should keep in mind to ensure your obligations are met efficiently and securely.

Understanding Your Payment Options: Digital vs. Physical Channels

The modern taxpayer has a variety of tools at their disposal. The shift toward digital finance has made IRS payments faster and more verifiable, yet traditional methods remain a staple for those who prefer physical documentation or specific banking workflows.

The Efficiency of IRS Direct Pay

For individual taxpayers, IRS Direct Pay is often the most streamlined option. This tool allows you to pay your individual tax bill or estimated tax directly from your checking or savings account without any additional fees. From a financial management perspective, Direct Pay is advantageous because it provides an immediate confirmation number, which serves as a vital digital receipt for your records. It is used primarily for Form 1040 series, estimated taxes, and other individual income tax liabilities.

The Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is for individuals, EFTPS is the “gold standard” for businesses and individuals with complex tax requirements. This is a free service provided by the Department of the Treasury. It requires a formal enrollment process, including the issuance of a PIN, which adds an extra layer of financial security. For business owners managing payroll taxes or large corporate tax liabilities, EFTPS allows for scheduled payments up to 365 days in advance, making it a powerful tool for cash flow forecasting.

Credit and Debit Card Payments

If you are looking to leverage credit card rewards or need a short-term bridge to cover a tax liability, the IRS utilizes third-party payment processors to accept card payments. While the IRS does not charge a fee for this, the processors do. From a personal finance standpoint, this option should be weighed carefully against the interest rates of the card and the convenience fee (usually between 1.8% and 2%). If your credit card offers 2% cash back or more, or if you are working toward a significant “sign-up bonus,” this route can actually be a strategic financial move.

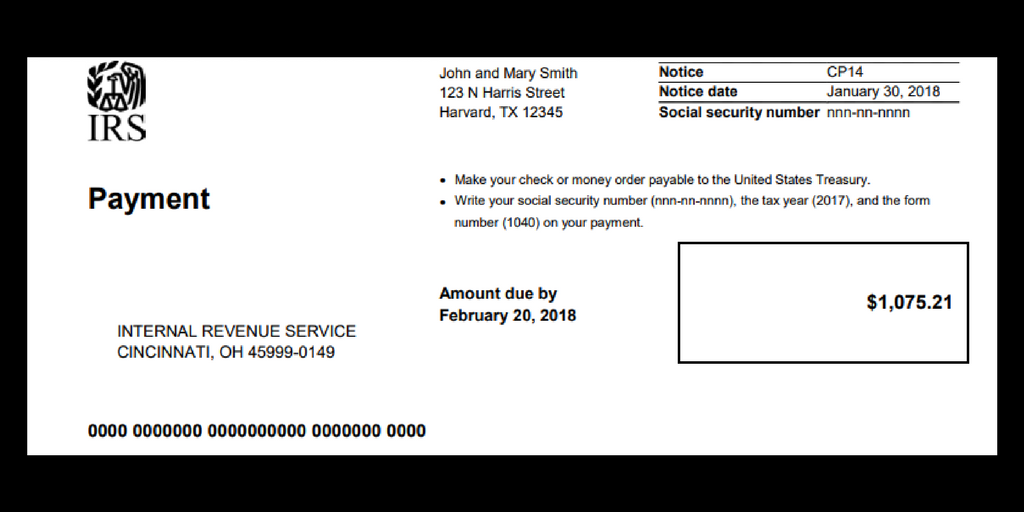

The Traditional Route: Sending a Check or Money Order by Mail

Despite the digital revolution, many taxpayers prefer the “paper trail” associated with mailing a physical check. However, sending money to the IRS via mail requires precision to ensure the payment is credited to the correct account and year.

Locating the Correct Mailing Address by State

The IRS does not have one single “headquarters” for payments. Instead, it uses several “lockbox” locations managed by various Department of the Treasury financial agents. The correct address depends entirely on two factors: the state where you live and whether or not you are enclosing a tax return with your payment.

For example, taxpayers in Florida or Louisiana might send their payments to a different processing center than those in California or Washington. It is essential to check the latest “Where to File” charts on the official IRS website or the instructions for Form 1040-V (Payment Voucher). Sending your payment to the wrong service center can lead to delays in processing, which might result in undeserved late-payment notices.

Essential Enclosures for Paper Payments

When mailing a payment, your check or money order must be accompanied by a Form 1040-V, the Payment Voucher. This small form is a critical piece of financial data communication; it tells the IRS’s automated systems exactly who you are and where the money should go. On the check itself, you should always include:

- Your name and address.

- Your Social Security Number (SSN) or Employer Identification Number (EIN).

- The tax year the payment applies to (e.g., “2023 Form 1040”).

- A daytime phone number.

Ensuring Proof of Mailing

In the world of personal finance, documentation is your best defense. If you choose to mail a payment, never send it via standard First-Class mail without tracking. Use United States Postal Service (USPS) Certified Mail with a Return Receipt Requested. This provides legal proof that your payment was sent on time, which is vital if the IRS claims a payment was late or never received.

Strategic Financial Planning for Tax Liability

Knowing where to send your payment is a matter of logistics; knowing how much and when to send it is a matter of financial strategy. Proper tax planning is the difference between a smooth financial year and a cash-flow crisis.

Managing Cash Flow for Quarterly Estimated Payments

For freelancers, contractors, and business owners, tax payments aren’t a once-a-year event. The U.S. tax system is a “pay-as-you-go” system. If you expect to owe more than $1,000, you are generally required to make quarterly estimated payments.

From a money management perspective, the best practice is to utilize a “sinking fund”—a high-yield savings account where you set aside 25-30% of every check received. By treating your tax liability as a non-negotiable monthly expense rather than an annual surprise, you ensure that the funds are available when the quarterly deadlines (April, June, September, and January) arrive.

The Benefits of Early Filing and Payment

There is a common misconception that filing early means you must pay early. You can file your return in February and schedule your electronic payment for the April deadline. This allows you to retain your capital in an interest-bearing account for as long as possible while still fulfilling your administrative obligations.

Avoiding Late Fees and Interest Penalties

The financial cost of missing a tax payment is steep. The failure-to-pay penalty is 0.5% of the unpaid taxes for each month or part of a month the tax remains unpaid. Furthermore, the IRS charges underpayment interest that fluctuates quarterly. In a high-interest-rate environment, these penalties can quickly compound, turning a manageable tax bill into a significant financial burden.

Specialized Payment Scenarios for Business Owners and Investors

Tax remittance becomes more complex when you move beyond individual income. Different types of income require different forms and different “destinations” for your funds.

Payroll Taxes and FUTA

Business owners with employees have the added responsibility of acting as a fiduciary for the government. You must withhold Social Security, Medicare, and federal income tax from your employees’ checks and remit them to the IRS. These payments must be made electronically via EFTPS. Mailing a check for payroll taxes is generally not an option for most businesses and can lead to significant penalties.

Capital Gains and Investment Income Payments

If you have a significant windfall from the sale of stock, real estate, or cryptocurrency, you may need to make a one-time estimated tax payment to avoid the “underpayment of estimated tax” penalty at the end of the year. Investors should coordinate these payments with their overall portfolio strategy, ensuring they don’t liquidate assets at an inopportune time just to cover the tax bill.

Security and Verification: Protecting Your Financial Data

In an era of rampant identity theft and financial fraud, ensuring your IRS payment reaches the intended recipient is paramount.

Recognizing Official IRS Communications

The IRS will never initiate contact with taxpayers by email, text messages, or social media channels to request personal or financial information. If you receive an email with a link to “pay your taxes,” it is a phishing scam. Always navigate directly to IRS.gov to initiate any digital payment.

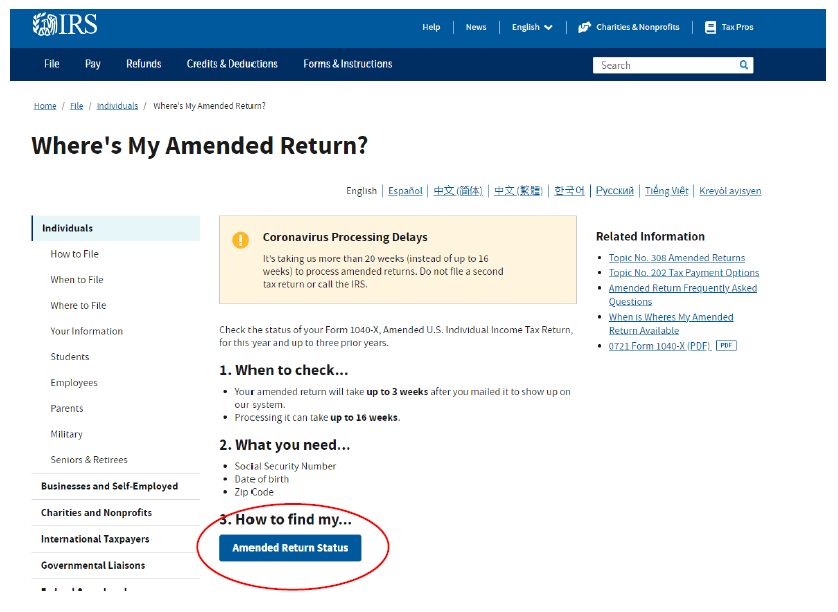

Verifying Your Payment Status Online

One of the best modern financial tools provided by the IRS is the “Online Account” feature. By creating an account through the IRS website (using ID.me for verification), you can view your balance, your payment history, and even digital copies of select notices. Checking this account 14 days after you make a payment is a best practice to ensure your funds were successfully applied to your account.

Dealing with “Lost” Payments

If you have sent a check and it hasn’t cleared your bank within three weeks, or if your digital payment doesn’t show in your IRS Online Account, proactive communication is key. Keep your bank statements and your certified mail receipts. If a dispute arises, having a clear “paper trail” or “digital trail” is the only way to have penalties waived through a process called “Abatement for Reasonable Cause.”

By understanding the logistical “where” and the strategic “how” of IRS payments, you can transform a stressful annual requirement into a routine component of your professional financial management. Whether through a digital portal or a physical lockbox, the goal remains the same: accuracy, timeliness, and the preservation of your financial reputation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.