In an economy where financial needs can arise unexpectedly or opportunities demand capital, understanding where and how to secure a loan is a fundamental aspect of personal and business finance. Whether you’re looking to consolidate high-interest debt, finance a significant purchase, start a new venture, or cover an emergency, navigating the world of lending can seem daunting. This guide aims to demystify the process, exploring various loan options, identifying reliable sources, outlining the application steps, and highlighting crucial considerations to ensure you make informed decisions. Obtaining a loan isn’t just about getting money; it’s about finding the right financial product that aligns with your specific circumstances and long-term financial health.

Understanding the Landscape of Loan Options

The first step in finding the right loan is to understand the diverse array of products available. Loans are not one-size-fits-all; they are tailored to different needs, risk profiles, and repayment capacities. Knowing the distinctions between common loan types is crucial for making an educated choice.

Personal Loans: Versatility for Various Needs

Personal loans are perhaps the most flexible type of borrowing. Typically unsecured, meaning they don’t require collateral, these loans can be used for almost any purpose: debt consolidation, home improvements, medical expenses, vacation financing, or even covering unexpected emergencies. Lenders assess your creditworthiness, income, and debt-to-income ratio to determine your eligibility and interest rate. The repayment terms usually range from one to seven years, with fixed monthly payments. Their versatility makes them a popular choice for individuals seeking a lump sum of cash without specific collateral.

Secured vs. Unsecured Loans: What’s the Difference?

The distinction between secured and unsecured loans is fundamental.

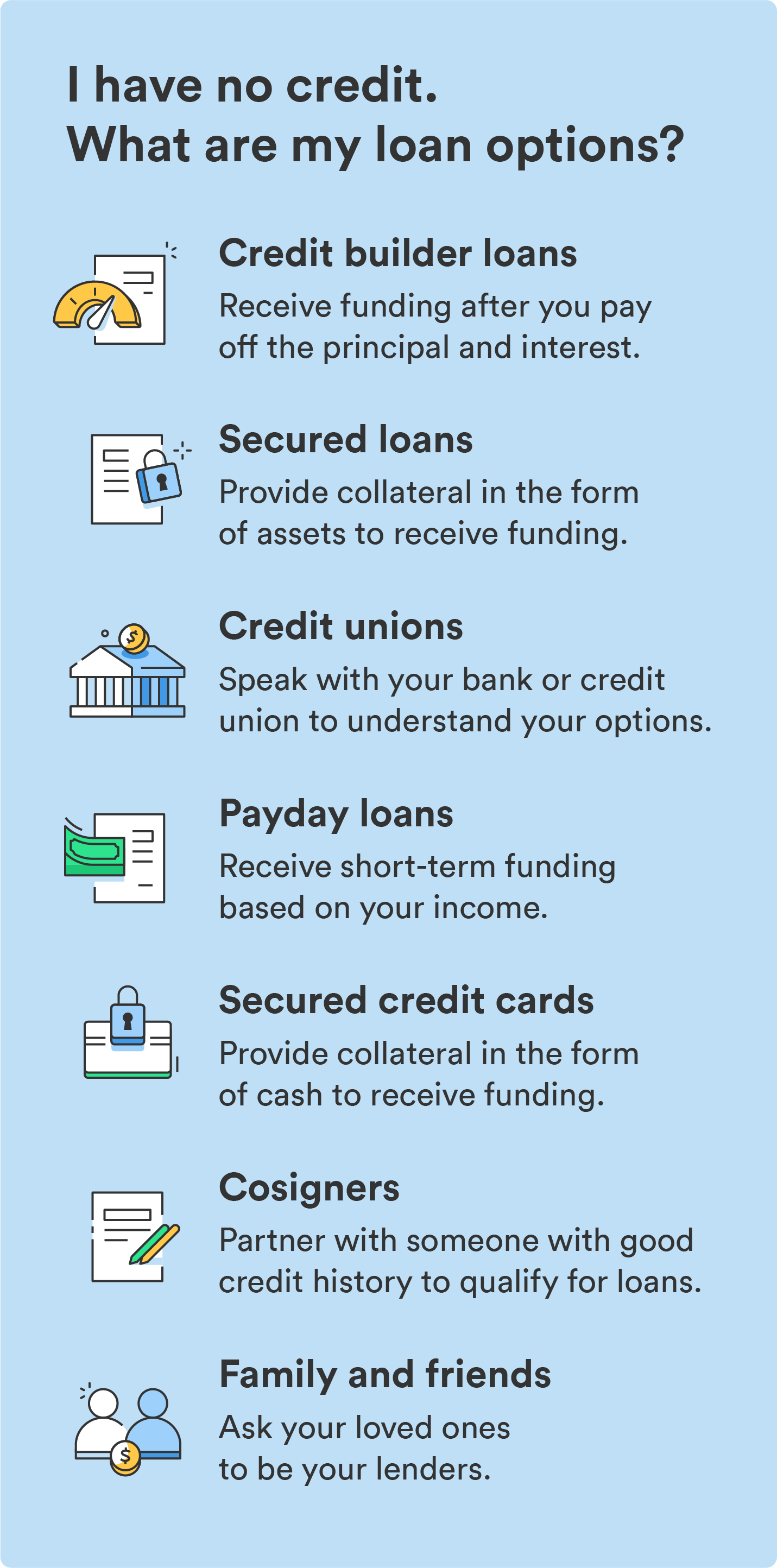

- Unsecured Loans: As mentioned with personal loans, these loans are not backed by any asset. Lenders rely solely on your credit history and income to assess your ability to repay. This higher risk for the lender often translates into higher interest rates, especially for applicants with lower credit scores. Examples include personal loans, most credit cards, and student loans.

- Secured Loans: These loans require collateral, an asset that the lender can seize if you fail to repay the loan. Common collateral includes real estate (for mortgages), vehicles (for auto loans), or savings accounts. Because the lender’s risk is lower, secured loans typically come with lower interest rates and more favorable terms. Home equity loans and car title loans are other examples. While they offer better terms, the risk of losing your asset if you default is a significant consideration.

Specific Purpose Loans: Mortgages, Auto, Student, and Business

Beyond the general categories, many loans are designed for very specific purposes, each with its own structure and requirements.

- Mortgages: These are secured loans used to purchase real estate, with the property itself serving as collateral. They are typically long-term (15-30 years) and come with various interest rate options (fixed or adjustable).

- Auto Loans: Used to finance the purchase of a vehicle, these are secured loans where the car serves as collateral. Terms are generally shorter than mortgages (3-7 years).

- Student Loans: Designed to cover educational expenses, these can be federal or private. Federal student loans often offer more flexible repayment options and don’t typically require a credit check for undergraduate students, while private student loans are credit-based.

- Business Loans: These are crucial for entrepreneurs and small business owners. They come in many forms, including term loans, lines of credit, SBA loans, equipment financing, and invoice financing, each catering to different business needs and stages of growth. They can be secured or unsecured, depending on the lender and the business’s financials.

Key Sources for Obtaining a Loan

Once you understand the type of loan you need, the next step is to identify where to get it. The lending landscape has expanded significantly beyond traditional banks, offering consumers and businesses more options than ever before.

Traditional Banks and Credit Unions

These remain cornerstone institutions for lending.

- Banks: Large national and regional banks offer a full spectrum of loan products, from personal loans and mortgages to business lines of credit. They often have established processes, physical branches, and a wide range of customer service options. However, they can have stricter eligibility criteria, especially regarding credit scores and income.

- Credit Unions: Member-owned financial cooperatives, credit unions often offer more personalized service and may have slightly lower interest rates or more flexible terms compared to traditional banks, particularly for members with less-than-perfect credit. Their focus is on serving their members, making them an attractive option for many.

Online Lenders and Fintech Platforms

The rise of financial technology (fintech) has revolutionized the lending industry, offering speed, convenience, and often more competitive rates.

- Online Personal Loan Lenders: Companies like SoFi, LendingClub, Prosper, and LightStream specialize in personal loans, often boasting quick application processes, fast funding, and competitive rates for borrowers with good credit. They leverage technology to streamline underwriting, making the experience more efficient.

- Online Small Business Lenders: Platforms such as Kabbage, OnDeck, and Fundbox provide a range of business financing options, often with quicker approvals than traditional banks. They cater particularly to small businesses that might struggle to meet traditional bank requirements, though interest rates can sometimes be higher.

Peer-to-Peer (P2P) Lending

P2P lending platforms connect individual borrowers directly with individual investors. These platforms, such as LendingClub and Prosper, facilitate loans that are funded by a collective of investors rather than a single institution. This model can sometimes offer competitive rates for borrowers and an alternative investment opportunity for lenders. P2P loans are typically unsecured personal loans, and eligibility depends on your credit profile and the platform’s specific criteria.

Alternative Lenders (Payday, Title Loans – with caveats)

While these options exist, they come with significant warnings.

- Payday Loans: These are short-term, high-interest loans, typically for small amounts, intended to be repaid on your next payday. They are notorious for extremely high Annual Percentage Rates (APRs) and can trap borrowers in a cycle of debt. They should generally be considered a last resort for financial emergencies only when no other options are available, and you are absolutely certain you can repay on time.

- Car Title Loans: These are secured loans where your car title acts as collateral. While they offer quick access to cash, the interest rates are very high, and you risk losing your vehicle if you default. Like payday loans, they carry substantial risk and should be approached with extreme caution.

The Loan Application Process: What to Expect

Regardless of the lender or loan type, the application process generally follows a structured path. Understanding each stage can help you prepare and increase your chances of approval.

Pre-Qualification and Research

Before formally applying, many lenders offer a pre-qualification option. This involves a soft credit pull (which doesn’t impact your credit score) to give you an estimate of the loan amount, interest rate, and terms you might qualify for. Use this step to compare offers from multiple lenders without commitment. Research different lenders, read reviews, and understand their specific eligibility criteria.

Gathering Necessary Documentation

Once you decide on a lender, you’ll need to submit a formal application, which requires detailed documentation. This typically includes:

- Proof of Identity: Driver’s license, passport, Social Security card.

- Proof of Income: Pay stubs, tax returns, bank statements, W-2s, 1099s.

- Proof of Residence: Utility bills, lease agreement, mortgage statements.

- Financial Statements: Bank statements, investment statements (especially for business loans).

- Credit History: Lenders will pull your credit report, so ensure it’s accurate beforehand.

Understanding Credit Scores and Reports

Your credit score is a numerical representation of your creditworthiness and plays a pivotal role in loan approval and interest rates. Lenders use scores (like FICO or VantageScore) to assess the risk of lending to you. A higher score (generally 670 and above) indicates a lower risk, leading to better loan terms. It’s wise to check your credit report from all three major bureaus (Experian, Equifax, TransUnion) annually for accuracy and to understand your financial standing. Dispute any errors promptly.

Reviewing Loan Offers and Terms

Once approved, you’ll receive a loan offer detailing the principal amount, interest rate, APR (Annual Percentage Rate, which includes fees), repayment schedule, and any associated fees. Read this document meticulously. Understand the total cost of the loan, including all charges. Don’t hesitate to ask questions if anything is unclear. Compare the APR, not just the interest rate, between offers to get a true picture of the loan’s cost.

Important Considerations Before Taking Out a Loan

Borrowing money is a significant financial decision. Before signing on the dotted line, it’s critical to weigh several factors to ensure it’s the right move for your financial well-being.

Assessing Your Repayment Capability

The most crucial question is whether you can comfortably afford the monthly payments without straining your budget. Create a realistic budget that includes the new loan payment and ensure you have sufficient disposable income to cover it, even if unexpected expenses arise. Failing to repay a loan can lead to severe consequences, including damage to your credit score, collection calls, and even legal action.

Interest Rates, Fees, and APR

Always compare the APR (Annual Percentage Rate) across different loan offers. The APR is a more comprehensive measure of the cost of borrowing as it includes both the interest rate and most fees associated with the loan. Look out for origination fees, application fees, late payment fees, and prepayment penalties. A seemingly low interest rate might be offset by high fees, making the overall loan more expensive.

The Impact on Your Credit Score

Taking out a new loan can initially cause a slight dip in your credit score due due to the hard inquiry on your credit report and the new credit account. However, consistently making on-time payments will significantly boost your credit score over time, demonstrating responsible financial behavior. Conversely, late or missed payments will severely damage your credit, making it harder and more expensive to borrow in the future.

Avoiding Predatory Lenders and Scams

Be vigilant against predatory lenders who target vulnerable borrowers with extremely high-interest rates, hidden fees, and deceptive terms. Be wary of lenders who guarantee approval regardless of credit history, pressure you to act immediately, or demand upfront fees before processing a loan. Legitimate lenders will always assess your ability to repay and will be transparent about all terms and conditions. If an offer seems too good to be true, it probably is.

Managing Your Loan Responsibly

Securing a loan is only half the battle; managing it responsibly is key to leveraging it as a financial tool rather than a burden.

Strategies for On-Time Payments

Punctuality is paramount. Set up automatic payments from your bank account to avoid missing due dates. If automatic payments aren’t an option, mark payment due dates on your calendar and set reminders. Consider making bi-weekly payments if your lender allows, as this can sometimes reduce the total interest paid and shorten the loan term. If you anticipate difficulty making a payment, contact your lender immediately to discuss options.

Refinancing and Debt Consolidation Options

If you have multiple high-interest debts, or if interest rates have dropped since you took out your original loan, debt consolidation or refinancing might be viable options.

- Debt Consolidation Loan: This involves taking out a new loan (often a personal loan) to pay off several existing debts. The goal is to simplify payments into one monthly bill, ideally at a lower interest rate, reducing your overall cost and making debt management easier.

- Refinancing: This means replacing an existing loan with a new one, often to secure a lower interest rate, change the loan term (shorter to save interest, longer to reduce monthly payments), or switch from an adjustable to a fixed rate. This is common for mortgages and student loans.

The Path to Financial Freedom

Ultimately, a loan should serve as a stepping stone, not a permanent fixture. Use it strategically to achieve your financial goals, whether it’s buying a home, funding an education, or growing a business. Develop a clear repayment plan and stick to it. As you pay down your loan, you not only improve your creditworthiness but also free up your financial resources, paving the way for greater financial flexibility and independence.

In conclusion, where you can get a loan depends on what type of loan you need, your financial profile, and your preference for traditional versus modern lending platforms. By understanding your options, carefully navigating the application process, and considering the long-term implications, you can secure the right financing to achieve your objectives without compromising your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.