Navigating the financial world to find a loan can feel like an overwhelming task. Whether you are looking to consolidate debt, fund a major home renovation, expand a small business, or cover an unexpected emergency, the question “where can I get a loan?” is often followed by a realization that there are more options today than ever before. The evolution of the financial sector has moved far beyond the local town bank, introducing digital-first platforms, member-owned cooperatives, and specialized private lenders.

Understanding where to look requires an assessment of your financial health, the purpose of the funds, and the speed at which you need the capital. This guide explores the diverse landscape of modern lending to help you identify the best source for your specific needs.

1. Traditional Banking Institutions: The Pillar of Stability

For many, the first instinct when seeking a loan is to visit a traditional commercial bank. These institutions remain the backbone of the global financial system, offering a sense of security and a wide range of products.

Commercial Banks

National and international banks, such as Chase, Bank of America, or Wells Fargo, offer a variety of loan products including personal loans, mortgages, auto loans, and business lines of credit. The primary advantage of a commercial bank is the potential for “relationship banking.” If you already hold a checking or savings account with a bank, they may offer you preferential interest rates or a more streamlined application process. However, commercial banks typically have the most stringent credit requirements. They favor borrowers with high credit scores and stable, verifiable income.

Credit Unions

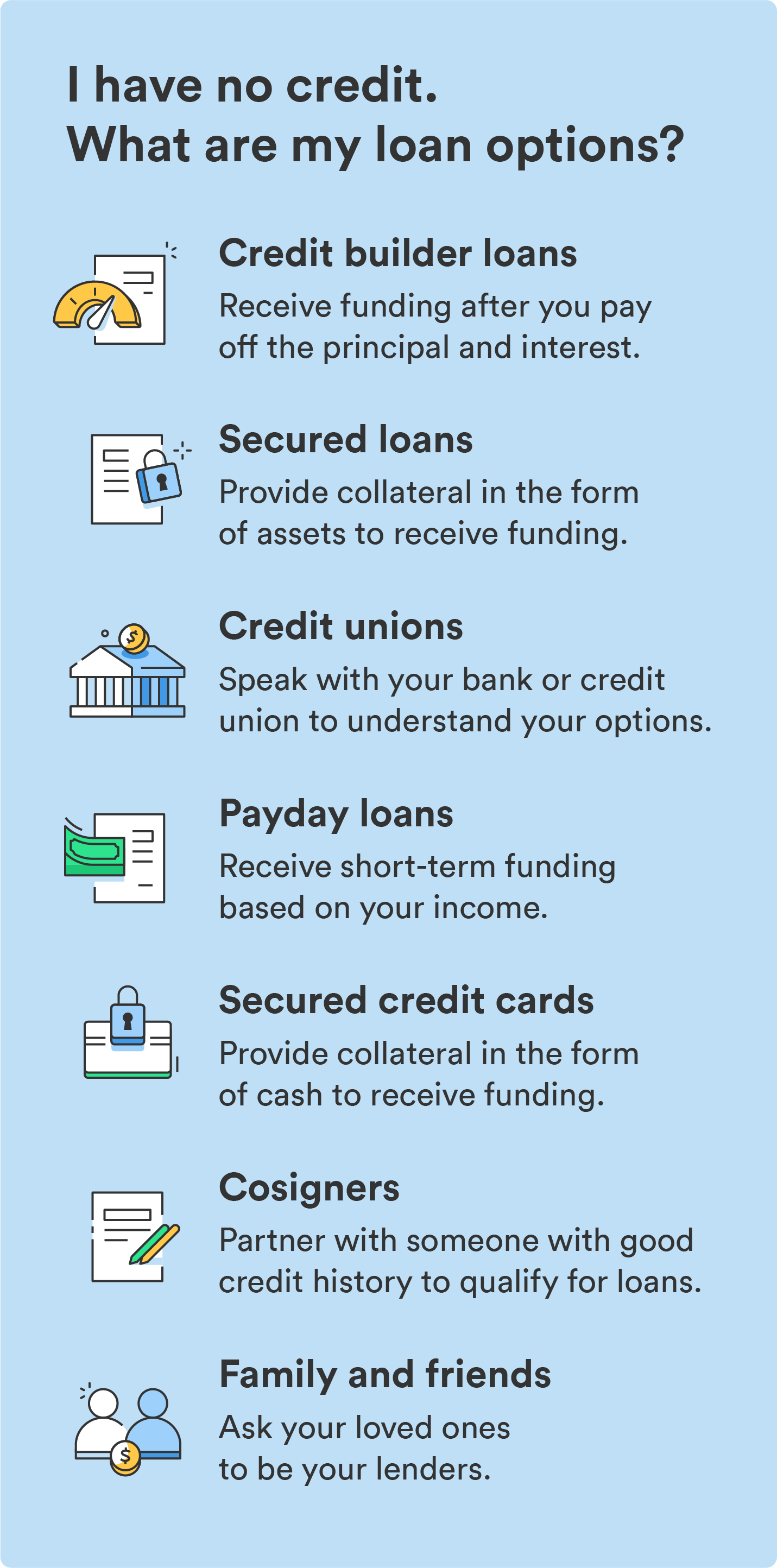

Credit unions are member-owned, non-profit financial cooperatives. Because they are not beholden to shareholders, they often return their “profits” to members in the form of lower interest rates on loans and higher yields on savings. For a borrower, a credit union is often the most cost-effective place to get a loan. The downside is that you must meet specific membership criteria—such as living in a certain geographic area or working in a specific industry—to apply. Furthermore, their digital interfaces may sometimes lag behind the cutting-edge tech of major banks or fintech firms.

Community Banks

Community banks focus on local lending and personal relationships. They are often more flexible than large national banks because their decision-making process happens locally rather than through a centralized corporate algorithm. If your financial situation is unique—perhaps you are self-employed or have a non-traditional income stream—a community bank might be more willing to look at the “whole picture” rather than just a credit score.

2. The Fintech Revolution: Online and Digital Lenders

In the last decade, financial technology (Fintech) companies have disrupted the lending industry by prioritizing speed, accessibility, and user experience. If you need funds quickly and prefer an entirely digital process, this is often the best route.

Personal Loan Platforms

Online lenders like SoFi, Marcus, or Rocket Loans have streamlined the borrowing process. These platforms use advanced algorithms to assess risk, often looking at data points beyond traditional FICO scores, such as education and employment history. The primary draw of online lenders is speed; it is not uncommon for a borrower to apply, receive approval, and have funds deposited into their account within 24 to 48 hours.

Peer-to-Peer (P2P) Lending

Peer-to-peer lending platforms, such as LendingClub or Prosper, act as intermediaries that connect individual borrowers directly with individual or institutional investors. Instead of borrowing from a bank, you are borrowing from a pool of people looking to earn interest on their capital. P2P loans can be a great alternative for those who may not fit the rigid box of traditional banking, though interest rates can vary significantly based on the “grade” assigned to your loan by the platform.

Neobanks and Mobile-First Lenders

A new generation of “neobanks”—banks that exist almost exclusively as mobile apps—now offer integrated lending products. Companies like Chime or Varo often provide small-dollar “spot” loans or credit-builder products. While these are usually not suitable for large-scale financing like a mortgage, they are excellent for managing short-term cash flow gaps without the predatory terms often associated with payday lenders.

3. Specialized Loans for Specific Financial Goals

Sometimes, the “where” depends entirely on the “what.” Certain financial needs are best served by specialized lenders who understand the nuances of specific industries or life stages.

Small Business Administration (SBA) and Business Lenders

If you are seeking a loan to start or grow a business, traditional personal loans are rarely the best fit. The U.S. Small Business Administration (SBA) doesn’t lend money directly but guarantees loans made by partner banks. This guarantee reduces risk for the lender, allowing them to offer better terms to small business owners. Additionally, online business lenders like OnDeck or BlueVine offer working capital loans and lines of credit specifically tailored to the cash flow cycles of small enterprises.

Education and Student Loan Providers

For funding higher education, the first stop should always be federal student loans due to their fixed interest rates and income-driven repayment plans. However, if federal limits are reached, private student loan providers like Sallie Mae or specialized refi-companies like Earnest provide targeted lending. These institutions focus on the future earning potential of the student, which is a different risk profile than a standard consumer loan.

Mortgage Lenders and Brokers

Buying a home is the largest financial commitment most people will ever make. While banks offer mortgages, specialized mortgage companies (like Quicken Loans) and mortgage brokers often provide a wider array of products. A mortgage broker, in particular, acts as a “personal shopper,” comparing rates from dozens of different lenders to find the one that fits your specific down payment ability and credit profile.

4. Alternative and Asset-Backed Lending

For those who may have significant assets but limited liquid cash—or those with poor credit who have collateral—alternative lending paths exist.

Home Equity Lines of Credit (HELOC) and Home Equity Loans

If you own a home with significant equity, your house can serve as the source of your loan. A HELOC allows you to borrow against the value of your property. Because these loans are secured by real estate, the interest rates are typically much lower than unsecured personal loans or credit cards. However, the risk is high: if you fail to repay, you could lose your home.

401(k) and Life Insurance Loans

In some cases, you can “be your own bank.” Many employer-sponsored 401(k) plans allow participants to borrow against their balance. The interest you pay on the loan goes back into your own account, which sounds ideal. However, if you leave your job, the loan often becomes due immediately, and failure to pay results in heavy taxes and penalties. Similarly, “permanent” or “whole” life insurance policies often allow you to borrow against the cash value of the policy with no credit check required.

Secured Personal Loans

If you have a low credit score but have savings, you can get a “CD-secured” or “savings-secured” loan from a bank. The bank holds your deposit as collateral, reducing their risk and allowing you to access a loan to build credit history.

5. Critical Factors to Evaluate Before Choosing a Lender

Finding where to get a loan is only half the battle; the other half is ensuring the loan doesn’t jeopardize your long-term financial health. Before signing a promissory note, you must evaluate the following three pillars.

Credit Score and Eligibility Requirements

Your credit score is the primary determinant of where you can get a loan and how much it will cost. Before applying, check your score. If it is below 600, you may be limited to secured loans or high-interest online lenders. If it is above 740, the world of low-interest traditional banking and premium fintech products is open to you. Always check the “eligibility” section of a lender’s website to see if they have minimum income requirements or geographic restrictions.

The True Cost: APR vs. Interest Rate

Many borrowers make the mistake of looking only at the interest rate. The Annual Percentage Rate (APR) is a more accurate measure because it includes the interest rate plus any origination fees, processing fees, or mandatory insurance. A loan with a 7% interest rate and a 3% origination fee might actually be more expensive than a loan with an 8% interest rate and no fees. Always ask for a breakdown of the total cost of borrowing over the life of the loan.

Repayment Terms and Flexibility

A loan is a long-term relationship. Look at the repayment terms: are they fixed or variable? A variable rate might start lower but could skyrocket if market conditions change. Additionally, check for “prepayment penalties.” Some lenders charge you a fee if you pay the loan off early, effectively punishing you for being financially responsible. In the modern market, the best lenders (especially in the Fintech and Credit Union sectors) typically offer no-fee prepayment options.

In conclusion, the answer to “where can I get a loan” is highly personal. If you value low rates and have great credit, a credit union or traditional bank is likely your best bet. If you value speed and ease of use, an online fintech lender is the way to go. For those with specific needs, like starting a business or buying a home, specialized lenders offer the most tailored expertise. By understanding the landscape and carefully vetting the terms, you can secure the capital you need while maintaining a trajectory toward financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.